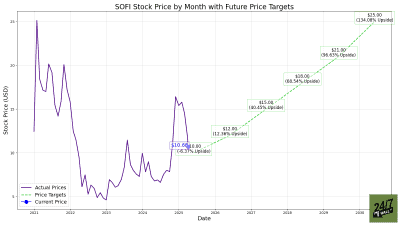

SoFi Technologies (NASDAQ:SOFI | SOFI Price Prediction) has quietly built the profile of an ideal fintech takeover target: 14.7 million members, a national bank charter, over $40 billion in member deposits funding over 90% of liabilities, and the Galileo technology platform servicing approximately 133 million global accounts. At a share price around $18 and a market cap below $23 billion, it is digestible for any mega-cap acquirer.

Here’s the catch: this is a deal to buy a regulated bank. SoFi Bank’s charter reshapes both the strategic fit and the approval path for every candidate.

4. PayPal: Strategic Logic, Weakest Case

PayPal (NASDAQ:PYPL) needs a growth story. Q1 2026 revenue of $8.353 billion grew just 7.21%, and CEO Enrique Lores has guided FY2026 non-GAAP EPS flat to slightly lower vs. FY 2025’s $5.31. A SoFi bolt-on would hand Venmo a bank charter and a lending engine. But with a market cap of $41.8 billion and just $13.5 billion in cash, the math forces heavy leverage or dilution. Becoming a bank holding company under the Fed would compound the challenge.

3. JPMorgan: Capacity Without Room

JPMorgan Chase (NYSE:JPM) has the checkbook. Q2 2026 revenue reached a better-than-expected $57.35 billion, and the board authorized a new $50 billion share repurchase program. SoFi would supercharge its digital-native reach. Yet JPMorgan already brushes against the 10% nationwide deposit cap. Adding SoFi’s deposits would trigger intense Fed and OCC scrutiny that likely blocks the deal outright.

2. Bank of America: Cleaner Fit, Same Cap Problem

Bank of America (NYSE:BAC) posted Q2 2026 EPS of $1.21 and services 60 million active digital banking users. Brian Moynihan’s Erica-plus-Zelle strategy would mesh cleanly with SoFi’s app-first millennial base and Galileo’s B2B rails. Still, Bank of America is also close to the deposit-cap ceiling, and absorbing another chartered bank invites the same regulatory hurdles as JPMorgan.

1. Mastercard: The Payoff Fit

Mastercard (NYSE:MA) is the cleanest strategic buyer. It is already SoFi’s partner: CEO Anthony Noto has described an important partnership with Mastercard to enable SoFiUSD settlement across their global payments network. Michael Miebach has signaled the direction, telling investors Mastercard is “expanding our stablecoin solutions through the planned acquisition of BVNK.” With $7.91 billion in cash, 60.8% operating margins, and $11.7 billion in buyback authorization, capacity is ample. The real hurdle is owning a chartered bank, though the Galileo platform and SoFiUSD infrastructure make the strategic prize unusually rich.

The Private Equity Question

Private equity would rank between PayPal and JPMorgan in terms of strategic fit. Sponsors have the cash, but Bank Holding Company Act rules cap non-controlling stakes and effectively bar a full buyout. Noto’s aggressive May and June share purchases at up to $18.0578 suggest that management is not shopping the company. Investors should watch SoFi’s FY2026 guidance of ~$4.655 billion revenue and ~$0.60 adjusted EPS as the real driver of the takeout math.

Contact [email protected] for any questions or corrections.