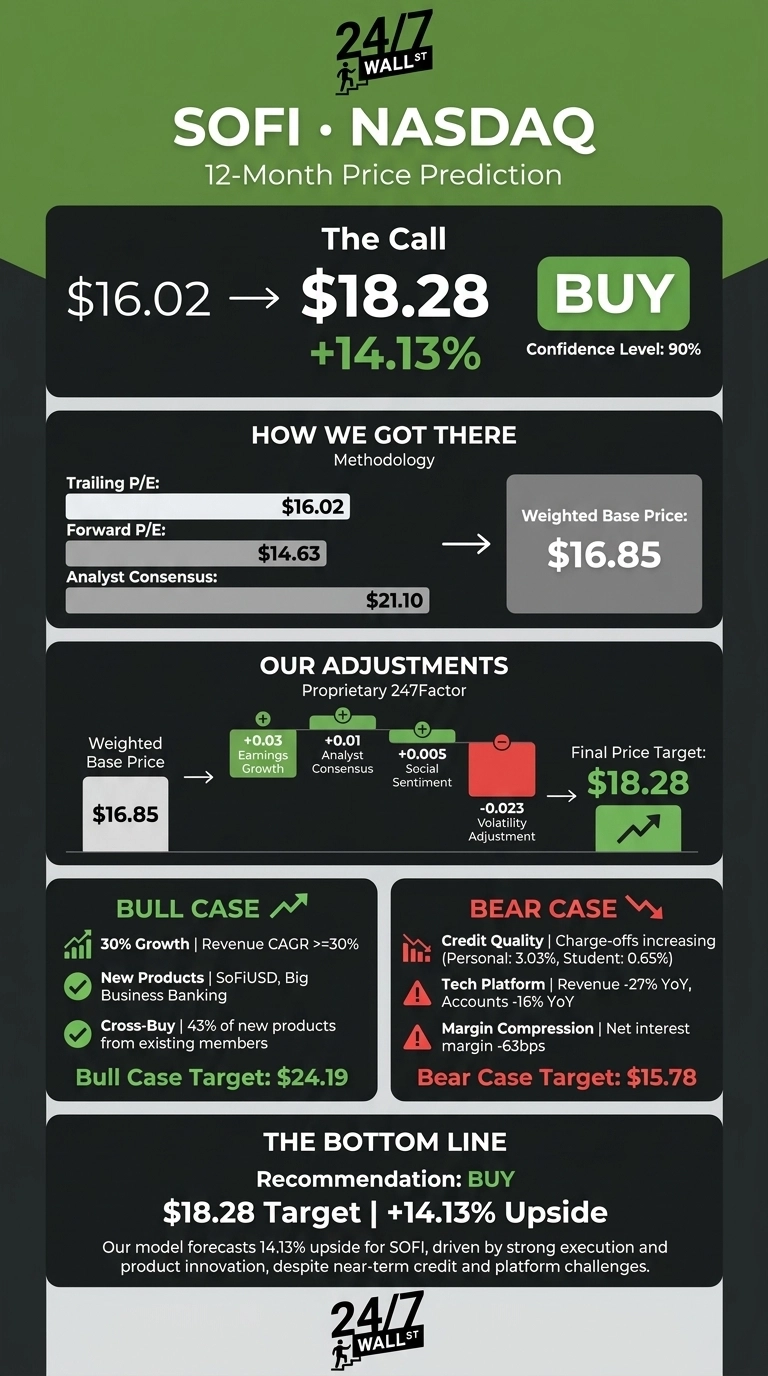

Our SoFi Technologies (NASDAQ:SOFI | SOFI Price Prediction) thesis is straightforward: the fintech is executing too well for the stock’s recent slide to last, even if the next 12 months bring more volatility than fireworks. The 24/7 Wall St. price target for SoFi is $18.28, implying 14.13% upside from $16.02. We rate shares a buy with high conviction (90% model confidence).

| Metric | Value |

|---|---|

| Current Price | $16.02 |

| 24/7 Wall St. Price Target | $18.28 |

| Upside | 14.13% |

| Recommendation | BUY |

| Confidence Level | 90% |

From $32 to $16: What Just Happened to SoFi

SoFi has been punished. Shares are down 38.81% year to date and 49.4% from the October 2025 high near $31.66, despite fundamentals that keep improving.

Q1 2026 revenue came in at $1.10 billion (up 41% YoY on an adjusted basis), GAAP net income more than doubled to $166.7 million, and loan originations hit a record $12.18 billion, up 68% YoY. Members grew 35% to 14.7 million.

Yet SOFI fell 15.44% on earnings day after merely meeting EPS at $0.12, with traders fixating on the Technology Platform segment’s 27% revenue decline tied to a single large client departure.

Why Bulls See SoFi Doubling by 2030

The bull case rests on durable compounding. CEO Anthony Noto told investors SoFi just delivered its “18th consecutive quarter of the Rule of 40 with a score of 72%” and called the company “in a class of one.” Management guides 2026 adjusted revenue to $4.655 billion (~30% growth) and a medium-term adjusted EPS CAGR of 38-42%.

Catalysts stack up. The SoFiUSD stablecoin (the first national bank stablecoin on a public permissionless blockchain), the Mastercard settlement partnership, Big Business Banking, and the relaunched SoFi Plus at 4.5% APY all expand the revenue surface. The Loan Platform Business added $3.6 billion in commitments in Q1. Our five-year bull case projects $41.56 by May 2031, a 159.43% return that hits the $32+ doubling threshold by 2029.

The Risks Worth Watching

The bear case starts with credit and margin pressure. Personal loan charge-offs ticked to 3.03% from 2.80%, student loan charge-offs to 0.65%, and average asset yields compressed 63 basis points YoY. The Technology Platform’s 27% revenue decline and 16% drop in enabled accounts raise legitimate questions about Galileo’s growth.

That said, bulls counter that the Technology Platform shock reflects one departing client, with like-for-like growth still running near 12% YoY and 13 new partners onboarded in Q1. Credit trends, while up, remain well inside SoFi’s 7-8% tolerance. A bear scenario tracks the model’s downside path to $15.78 over the next 12 months.

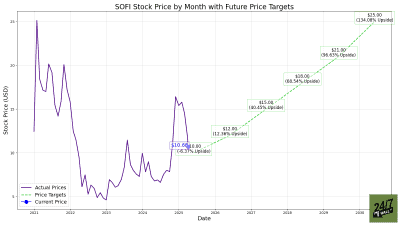

SoFi Price Prediction 2026-2030

The 24/7 Wall St. price target of $18.28 says shares are modestly mispriced today; the five-year math says they could be dramatically mispriced. A forward P/E near 26x on a business compounding revenue at 30% with expanding margins is not demanding.

The setup looks favorable for investors who can tolerate the 2.13 beta and want exposure to the fintech transition. The thesis weakens if credit trends worsen another quarter or Tech Platform revenue fails to stabilize by year end.

Looking further out, here is where our model projects SoFi could trade, assuming management hits its medium-term revenue and EPS targets.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $18 |

| 2027 | $22 |

| 2028 | $26 |

| 2029 | $30 |

| 2030 | $34 |

These projections assume SoFi continues compounding members at 30%+, defends net interest margin above 5%, and successfully monetizes SoFiUSD and Big Business Banking. Significant upside could come from stablecoin adoption; downside risk centers on a credit cycle turn or further Technology Platform attrition.

Contact [email protected] for any questions or corrections.