Few stocks divide investors quite like MicroStrategy (NASDAQ:MSTR | MSTR Price Prediction), the Bitcoin treasury vehicle now branded Strategy. The stock has declined alongside Bitcoin, but Wall Street analysts remain overwhelmingly constructive.

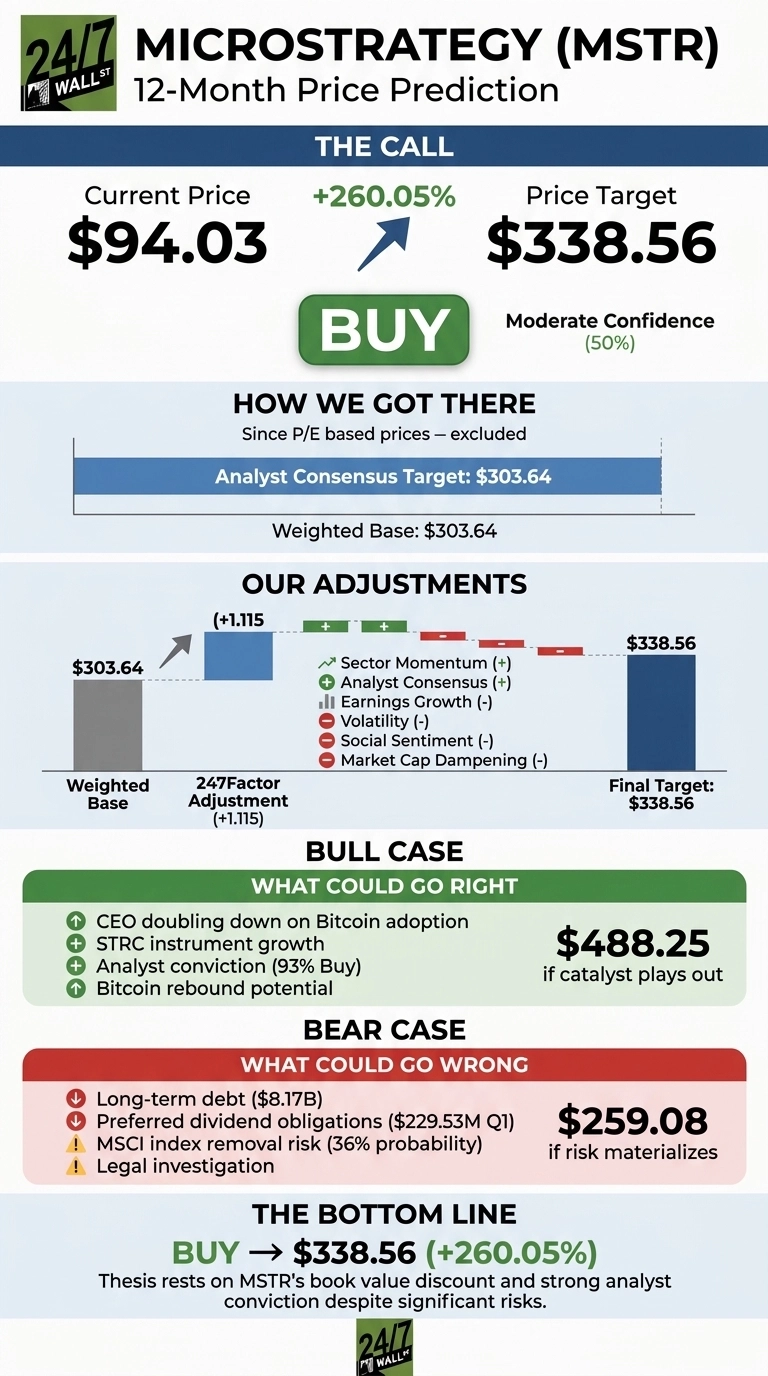

Our 24/7 Wall St. price target for MSTR is $338.56, implying 260.05% upside from the current price of $94.03. Our recommendation is buy, with a moderate 50% confidence level, reflecting the extreme Bitcoin sensitivity baked into the model.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $94.03 |

| 24/7 Wall St. Price Target | $338.56 |

| Upside | 260.05% |

| Recommendation | BUY |

| Confidence Level | 50% |

A Bitcoin Bear Market Has Punished MSTR

MSTR is down 79.37% over the past year, 38.12% year to date, and 23.43% over the past month, sitting just above its 52-week low of $81.81 and far below the $454.33 high. Bitcoin is off 46.63% over the same year at $63,658.88.

Q1 2026 showed EPS of -$38.25 versus a -$18.98 estimate on a $14.46 billion unrealized Bitcoin mark. Subscription revenue surged to $58.88 million, and MSTR now holds 818,334 BTC after raising $11.68 billion YTD.

The Case for $488 or Higher

Our bull case points to $488.25. CEO Phong Le is doubling down: “Adoption of Bitcoin continues to grow in 2026. Digital Credit, highlighted by STRC, has been a big success.” The STRC preferred instrument has scaled to an $8.5 billion market cap in nine months, and management authorized $2 billion in buybacks under the Digital Credit Capital Framework.

Benchmark Equity Research reiterated its Buy rating, and 13 of 14 covering analysts rate MSTR a Buy with a consensus target of $303.64. A Bitcoin rebound toward prior highs would compound the equity’s leveraged beta of 3.545.

What Could Go Wrong

Our bear case projects $259.08, but real damage lurks below. MSTR carries $8.17 billion in long-term debt and $229.53 million in quarterly preferred dividends against only $2.21 billion in cash. Polymarket assigns a 36% probability to MSCI index removal by year-end, and a Rosen Law Firm investigation adds legal overhang.

The software business is still expanding, with subscription revenue up sharply and 67.1% gross margins reflecting ASU 2023-08 fair-value accounting, an accounting-driven effect rather than an operational one.

How MSTR Stacks Up Against COIN and MARA

Coinbase (NASDAQ:COIN) is the most liquid crypto proxy on U.S. exchanges. The company posted $1.41 billion in Q1 revenue, down 30.54% YoY, at a market cap of $35.7 billion, versus MSTR’s $34.4 billion. Coinbase generates operating cash flow, making MSTR’s identical market cap look aggressive on fundamentals but conservative on Bitcoin-per-share exposure.

MARA Holdings (NASDAQ:MARA) is a purer Bitcoin miner comp with a $4.35 billion market cap and a Q1 net loss of $1.3 billion. MARA’s price-to-book of 1.25 compares with MSTR’s 0.91, meaning MSTR trades below book value on a Bitcoin-heavy balance sheet. That discount makes our $338.56 target reasonable.

Where the Setup Stands

The 24/7 Wall St. price target of $338.56 and buy rating rest on one core view: MSTR trades at a discount to book value on a portfolio of over 800,000 BTC, and analyst conviction remains near-unanimous with 13 Buy ratings.

The setup strengthens if Bitcoin stabilizes above $60,000 and STRC funding continues absorbing capital demand. Risk escalates if BTC breaks below $55,000 or the preferred stack shows stress. Confidence remains moderate at 50%.

MicroStrategy Price Prediction 2026-2030

Extending the 24/7 Wall St. price target model forward, here is where MSTR could trade assuming Bitcoin resumes its long-term uptrend and Strategy continues accretive accumulation.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $168 |

| 2027 | $338 |

| 2028 | $725 |

| 2029 | $1,650 |

| 2030 | $3,100 |

These projections assume Bitcoin trends higher over the decade and MSTR avoids forced deleveraging. Significant downside could result from a prolonged BTC drawdown, MSCI removal, or a preferred-dividend refinancing squeeze.

Contact [email protected] for any questions or corrections.