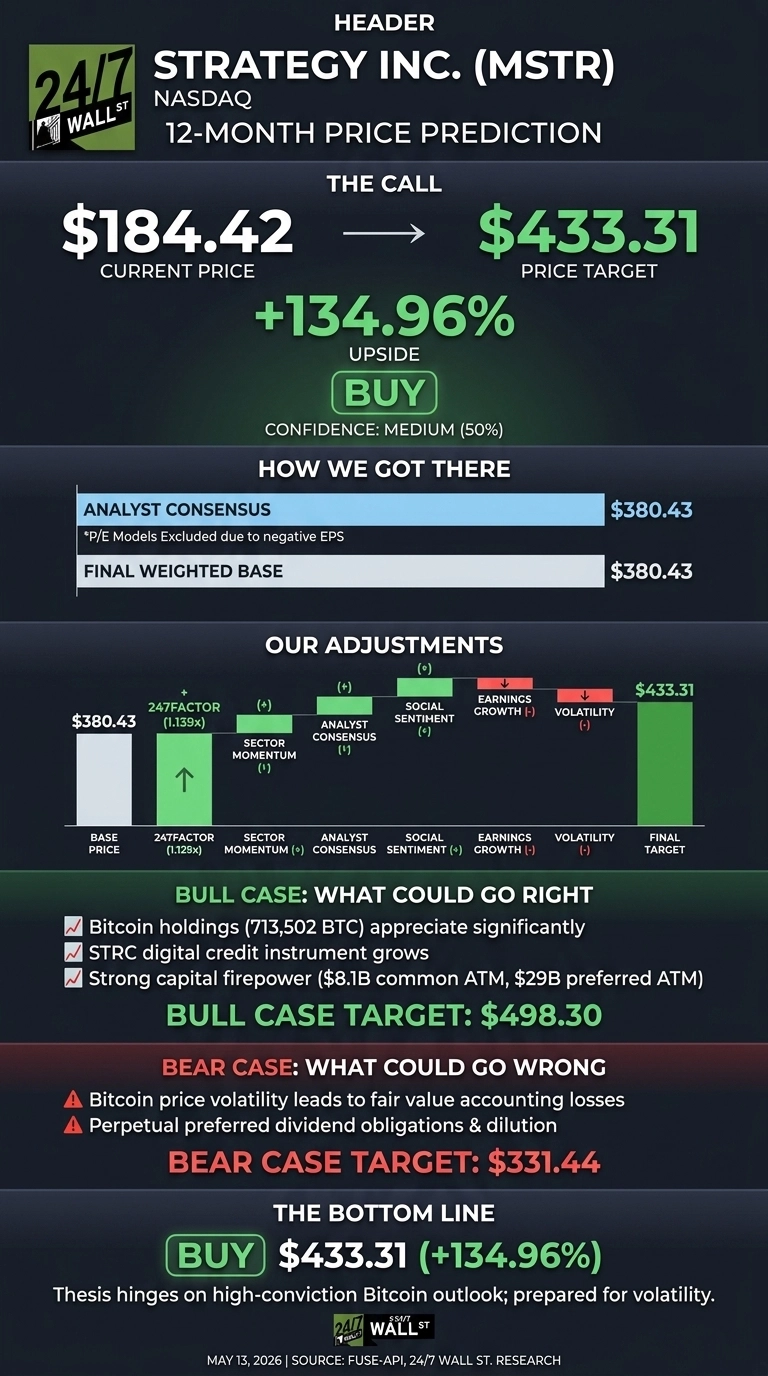

I’ll cut straight to the verdict. Strategy (NASDAQ:MSTR | MSTR Price Prediction), the Bitcoin treasury vehicle formerly known as MicroStrategy, has been gutted over the past year, but our model sees a meaningful rebound from here.

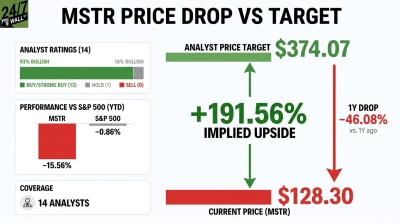

Current shares trade at $184.42, and the 24/7 Wall St. price target for Strategy is $433.31, implying 134.96% upside over the next 12 months. Our recommendation is buy with moderate confidence of 50%, reflecting the binary nature of MSTR’s Bitcoin-linked thesis.

.

.24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $184.42 |

| 24/7 Wall St. Price Target | $433.31 |

| Upside | 134.96% |

| Recommendation | BUY |

| Confidence Level | 50% |

A Brutal Year, A Sharp Spring Bounce

Strategy has been one of the most violent rides in large caps. Shares are down 54.45% over the past year from $404.90, but the trend has flipped. MSTR is up 43.36% in the past month and 21.37% year to date, even after a 5.88% single-day drop on May 12. The 52-week range stretches from $104.17 to $457.22.

Q4 2025, reported February 5, was the bruise. Revenue of $122.99M beat by 0.98% and grew 10.74% year over year, but EPS of -$42.93 missed estimates badly thanks to a $17.44B unrealized loss on Bitcoin under ASU 2023-08 fair value accounting. Subscription services revenue grew 62.1%, a quiet bright spot.

Why Bulls See a Breakout Ahead

The bull case is straightforward: Bitcoin goes up, MSTR goes up faster. Strategy holds 713,502 BTC as of February 1, 2026, including 41,002 BTC acquired in January alone. CEO Phong Le pointed to STRC, the flagship Digital Credit instrument, growing to “$3.4 billion in size, supported by increasing liquidity and declining volatility.” Capital firepower remains huge: $8.1B on the common ATM and $29B across preferred ATM programs.

Wall Street remains lopsidedly constructive with 14 Buy or Strong Buy ratings against just 1 Hold, and an analyst consensus target of $380.43. Our bull case scenario tops out at $498.30 over 12 months.

What Could Go Wrong

The bear case is equally simple: if Bitcoin tanks, the fair value accounting hammer falls again. Q4 2025’s $17.44B unrealized loss showed how unforgiving ASU 2023-08 can be. Management’s reaffirmed FY2025 guidance of $80 diluted EPS assumed Bitcoin reaching $150,000 by year-end, which did not happen. Perpetual preferred dividend obligations, the STRC rate of 11.25%, and constant ATM dilution are real costs.

It should be noted that bulls counter the optics: the Q4 loss is non-cash, software revenue accelerated to +10.74% growth, and shareholders equity sits at $44.12B. Our bear case still lands at $331.44, well above today’s price.

The Setup From Here, With Eyes Open

The 24/7 Wall St. price target of $433.31, the buy rating, and 50% confidence reflect a coiled spring. The tipping factor for me is the analyst skew combined with the recent month’s 43.36% bounce off the lows. The thesis hinges on conviction that Bitcoin holds above $80,000. Investors who cannot stomach beta of 3.6 swings will find the volatility difficult to absorb.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $433.31 |

| 2030 | $1,951 |

These projections assume Strategy continues compounding Bitcoin per share and that BTC trends higher through the cycle. Significant downside could result from a prolonged crypto winter or forced deleveraging of the preferred stack.

Contact [email protected] for any questions or corrections.