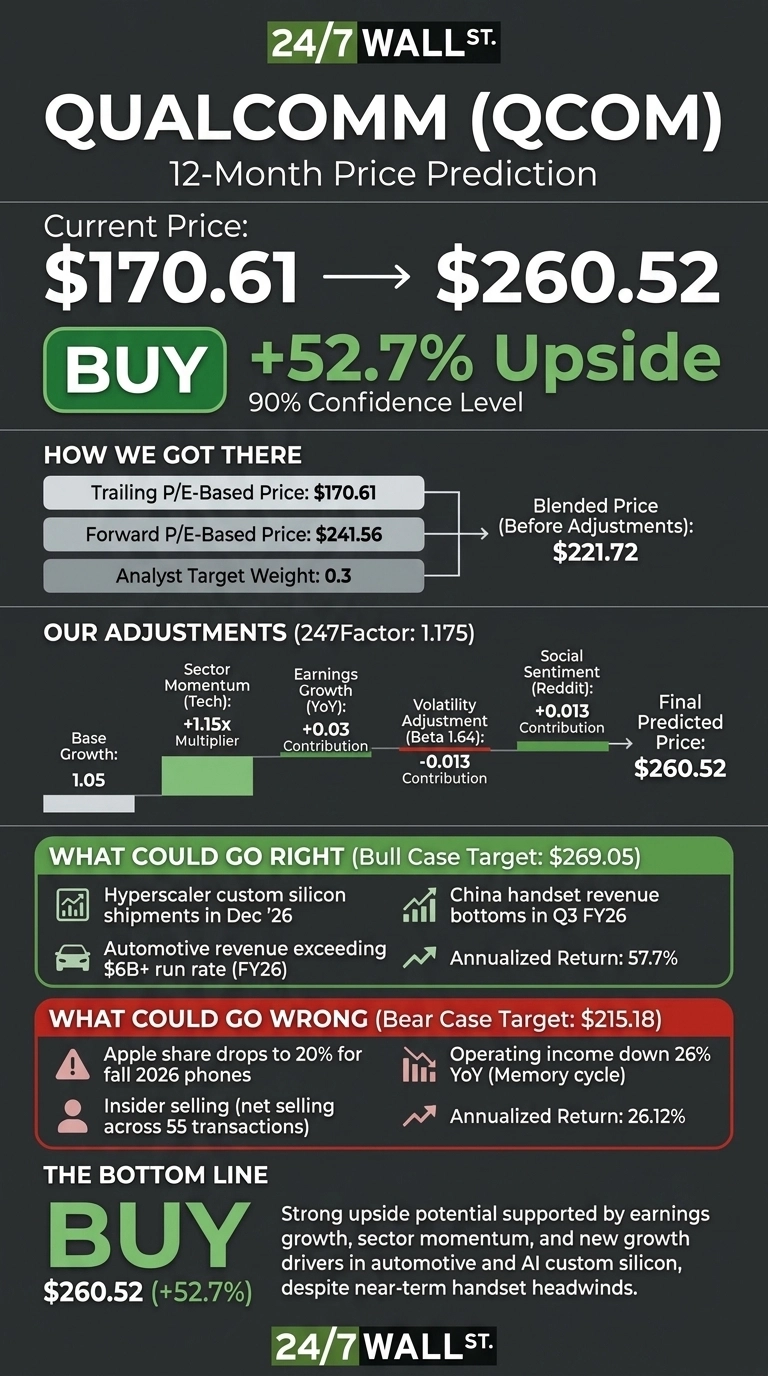

Qualcomm (NASDAQ:QCOM | QCOM Price Prediction) trades at $170.61 as of the July 16 close, down 20.3% over the past month after a sharp June rally faded. Our 24/7 Wall St. price target for Qualcomm is $260.52, implying 52.7% upside over the next 12 months. The recommendation is buy at a 90% confidence level.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $170.61 |

| 24/7 Wall St. Price Target | $260.52 |

| Upside | 52.7% |

| Recommendation | BUY |

| Confidence Level | 90% |

How QCOM Got Here: A Volatile Round Trip

Qualcomm has round-tripped dramatically. Shares hit a 52-week low near $121.54 in March, then rallied to $258.96 high after the June 24 Investor Day, where management doubled its 2029 non-handset revenue target to $40 billion and set a $15 billion AI data center sales goal. That rally has faded, leaving the stock roughly flat year to date at +0.77%.

Fundamentals remain healthy. Q2 FY26 revenue was $10.60 billion and non-GAAP EPS came in at $2.65, meeting expectations on the top line and beating by 3.67% on the bottom.

Automotive hit a record $1.326 billion, up 38% YoY, while handsets fell 13% on memory supply constraints and Chinese OEM channel drawdowns. Polymarket traders assign an 87% probability that Qualcomm beats its next earnings report on July 29.

The Case for $270+

The bull thesis rests on Qualcomm becoming a credible third player in hyperscaler custom silicon. CEO Cristiano Amon confirmed a custom silicon engagement with a leading hyperscaler is on track for initial shipments in the December quarter.

Automotive is guided to 50% YoY growth in Q3, exiting FY26 at $6 billion+ run rate. Analyst consensus target sits at $222.73, but our bull-case scenario points to $269.05 if the data center ramp lands cleanly and China handsets bottom on schedule.

What Could Go Wrong

The bear case starts with customer concentration. Qualcomm expects only 20% share of Apple phones launching fall 2026, with no relationship beyond that. Handset revenue fell 13% YoY, and Q3 FY26 guidance calls for a step-down to $9.2B-$10B in revenue and $2.10-$2.30 EPS.

Recent insider activity has skewed toward net selling across 55 transactions. Operating income fell 26% YoY largely on the memory cycle, and Amon has said the June quarter should mark the bottom for Chinese handset revenue. Our bear-case downside target is $215.18, still meaningfully above today’s price.

How Qualcomm Compares to NVIDIA and Broadcom

NVIDIA (NASDAQ:NVDA) trades at a P/E of roughly 42, with Q1 FY27 data center revenue of $75.25 billion, up 92% YoY. Qualcomm’s P/E near 32 and forward multiple in the low teens looks cheap in that context, though NVIDIA’s 55.6% net margin is in a different league.

Broadcom (NASDAQ:AVGO) is the closer analog, already selling custom AI accelerators to hyperscalers with Q2 FY26 AI semiconductor revenue of $10.80 billion, up 143% YoY, and Q3 guidance calling for $16 billion in AI semis alone.

Broadcom’s $1.78 trillion market cap reflects the multiple investors assign to that model. Qualcomm capturing even a fraction of the same rerating would justify our $260 target.

Weighing the Setup Into July 29 Earnings

My 24/7 Wall St. price target of $260.52 stands, with a buy recommendation at 90% confidence. At an implied P/E near 14x on $15.27 forward EPS, Qualcomm is priced for stagnation while management just doubled the 2029 non-handset revenue target.

The key catalysts to watch are whether July 29 earnings confirm the Chinese handset bottom and reiterate hyperscaler custom silicon timing. A further push-out of data center shipments into 2027 would undermine the thesis.

Qualcomm Price Prediction 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $215 |

| 2027 | $260 |

| 2028 | $329 |

| 2029 | $415 |

| 2030 | $523 |

These projections assume Qualcomm executes on its data center ramp and Automotive continues content-per-vehicle expansion. Meaningful upside or downside could come from Apple modem timing, China trade friction, or hyperscaler win rates.

Contact [email protected] for any questions or corrections.