The Financial Independence Retire Early (F.I.R.E.) strategy, embraced by Millennials and some Gen-Xers, can produce outcomes that exceed even optimistic projections. Founded on principles of thrift and aggressive growth-oriented investing, FIRE targets a nest egg of roughly 25 times annual expenses — a figure that supports a 4% annual withdrawal rate while the saver is still in their 50s, or occasionally their 40s.

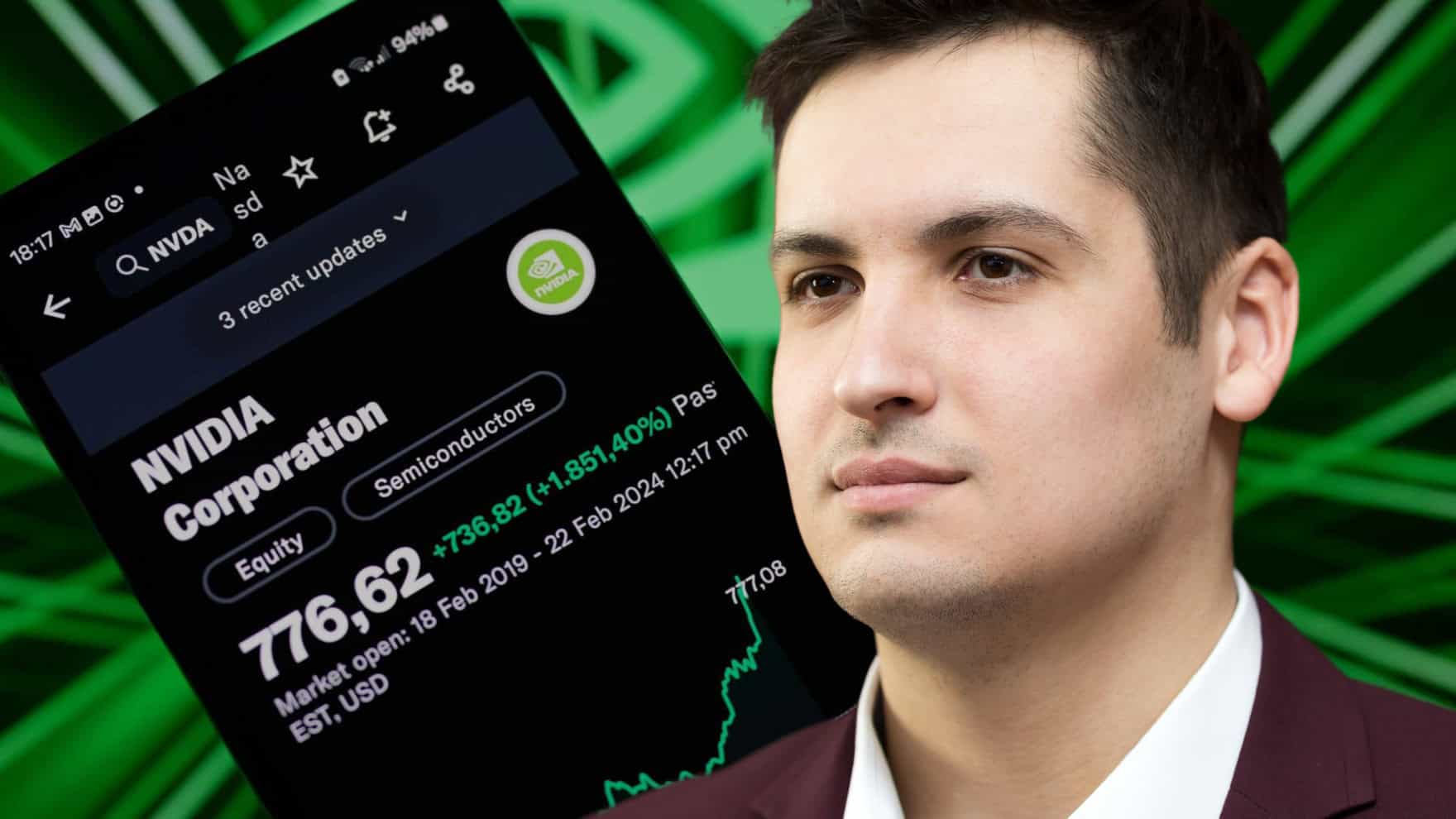

Anomalous market conditions can accelerate that timeline dramatically. As of mid-July 2026, disruptive technologies like artificial intelligence continue to act as rocket fuel for NVIDIA (NASDAQ:NVDA | NVDA Price Prediction). The stock closed near $212 on July 15, 2026, after the company reported actual Q1 FY2027 revenue of $81.6 billion, beating the prior Wall Street consensus of $78.8 billion and representing 85% growth year over year. NVIDIA also guided Q2 FY2027 revenue to approximately $91 billion, and its full fiscal year 2026 produced record revenue of $215.9 billion, up 65% from the prior year.

LEAPS Into the FIRE

LEAPS (Long Term Equity Appreciation Securities) calls are long term call options with expirations up to 3 years into the future.

One 34-year-old who had been actively self-managing his retirement account bought synthetic long LEAPS (Long Term Equity Appreciation Securities) calls on NVDA inside his Roth IRA, and that account has grown into multiple seven figures. Because options eventually expire rather than compounding indefinitely, he plans to cash them out and redeploy into index funds. His F.I.R.E. target may still be 5 to 7 years away, and the tax cost of early withdrawal is his most pressing concern.

Beyond a mortgage at 2.97%, the family already maxes out IRAs, 401(k)s, HSAs, and a 529, with household income exceeding $200,000. Their goal is more time for travel and family, potentially using geographic arbitrage by relocating to high-performing school districts in Marietta, GA or Orlando, FL to reduce cost-of-living expenses.

He posted three scenarios on Reddit and asked the community for feedback:

- Early withdrawal with a 10% penalty and a 37% tax on the remainder, moving the after-tax funds to a brokerage account to supplement income while gradually reducing work hours.

- Leaving the Roth IRA untouched to grow toward a more comfortable retirement, though doing so would require staying in his current role for another 25 years.

- Deploying systematic incremental withdrawals sized to keep taxable income within a lower bracket, a process that would nonetheless stretch beyond a decade.

Other Considerations To Bear in Mind

Converting IRA and 401-K accounts to Roth accounts can save thousands in taxes at withdrawal if the conversion is done earlier before significant growth after the fact occurs.

With the Roth IRA approaching $5 million and a target of $10 million, the core task shifts from accumulation to preservation and strategic income planning. For anyone in a comparable position, the 2026 Roth IRA contribution limit stands at $7,500 per year for those under 50, rising to $8,600 for those 50 and older under new catch-up rules introduced by SECURE 2.0. Additional strategies worth exploring include:

- Utilizing 72(t) Substantially Equal Periodic Payment (SEPP) guidelines to create sustainable, penalty-free early distributions. The applicable interest rate for 2026 SEPP calculations stands at 4.5%, representing 120% of the current federal mid-term rate, which directly affects how much income an amortization or annuity method plan can generate.

- Implementing an options-overlay strategy, such as selling covered calls or cash-secured puts, to generate yield on the existing portfolio without full liquidation.

- Reviewing 2026 ACA health insurance options, which represent the primary hurdle for early retirees who are leaving high-salary corporate roles and their employer-sponsored coverage.

- Segregating annual travel and discretionary expenses from current earned income, so that tax liabilities do not compound against the core retirement nest egg.

- Evaluating Roth conversion laddering within the 2026 tax landscape to bridge the gap between early retirement and age 59 and a half, when penalty-free Roth earnings withdrawals become available.

This article is intended solely as informational content. Anyone facing tax or retirement decisions of this complexity should consult a qualified financial or tax professional before taking action.

Editor’s note: This update revises NVIDIA’s stock price to approximately $212 (July 15, 2026 close), corrects the Q1 FY2027 revenue figure from the pre-earnings Wall Street estimate of $78.8 billion to the actual reported result of $81.6 billion, adds Q2 FY2027 guidance of $91 billion and full-year FY2026 revenue of $215.9 billion, and specifies the 2026 SEPP applicable interest rate of 4.5%.

Contact [email protected] for any questions or corrections.