A Reddit user recently posed an intriguing question: at what point does contributing to a 401(k) become unnecessary because compound growth alone will handle the heavy lifting?

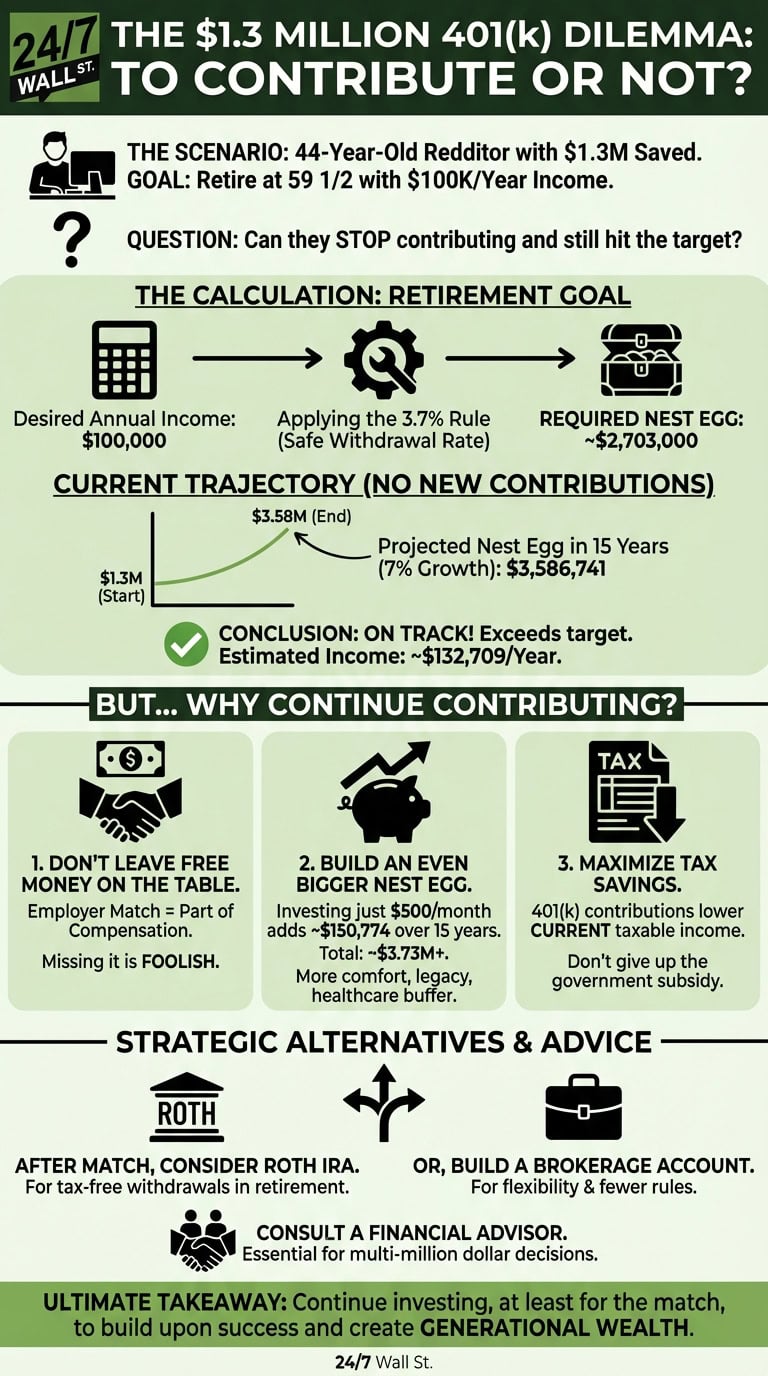

The 44-year-old poster has already accumulated $1.3 million and plans to retire at 59 1/2. He noted that even maxing out his contributions would represent just 1% of his account’s expected annual growth. His goal is straightforward: generate at least $100,000 per year in retirement income. Can he coast from here, or should he keep funding the account?

The answer hinges on how much you actually need and what you might be leaving on the table by stopping early.

Calculating the retirement target

Before deciding whether to halt contributions, you need to know your finish line. How much wealth do you need to safely produce $100,000 per year in retirement?

Financial planners traditionally relied on the 4% rule, which caps first-year withdrawals at 4% of the portfolio balance. That guideline has shifted. Morningstar’s latest 2025 research now recommends a 3.9% starting withdrawal rate for retirees seeking steady, inflation-adjusted spending over a 30-year horizon. This reflects a modest improvement from the 3.7% rate published in 2024, driven by updated capital-market assumptions.

Using the 3.9% benchmark, you would need roughly $2.56 million to generate $100,000 annually. If this Reddit user’s $1.3 million grows at a 7% average annual return for the next 15 years without any additional contributions, he will end up with approximately $3.59 million. That handily exceeds his target and would support around $140,000 in annual retirement income at a 3.9% withdrawal rate.

On paper, stopping contributions now still gets him to his goal. But that narrow calculation misses important considerations.

Why you might want to keep contributing anyway

First, if your employer offers matching contributions, walking away from them means forfeiting part of your compensation. Unless you genuinely cannot afford the deferrals while maintaining your lifestyle, leaving employer match dollars unclaimed is a costly mistake. That money is yours for the taking.

Second, continued contributions build a bigger cushion. If you contribute just $500 per month over the next 15 years at a 7% return, you would reach roughly $3.89 million instead of $3.59 million (before factoring in any employer match). That extra $300,000 provides flexibility for unexpected healthcare costs, market downturns early in retirement, or the ability to leave a larger inheritance.

Third, 401(k) contributions deliver immediate tax savings. Every dollar you defer reduces your current taxable income. Stop contributing and your tax bill climbs. Redirecting that money to the IRS instead of your retirement account rarely makes financial sense, especially for someone already in a strong savings position.

Alternative strategies beyond the 401(k)

Continuing to save does not necessarily mean pouring everything into your 401(k). Once you have captured your full employer match, other accounts may offer better advantages depending on your situation.

A Roth IRA, if you qualify based on income, allows tax-free withdrawals in retirement. For 2026, single filers with modified adjusted gross income below $153,000 and joint filers below $242,000 can contribute the full $7,500 annual limit ($8,600 if age 50 or older). Building a Roth alongside your traditional 401(k) creates valuable tax diversification, giving you more control over your retirement tax burden.

You might also consider building up a taxable brokerage account. Unlike retirement accounts, brokerage holdings carry no withdrawal restrictions or required minimum distributions. You gain full liquidity and a broader range of investment choices. If your 401(k) already covers your retirement income needs, steering additional savings into a brokerage account can provide accessible funds for pre-retirement goals or bridge income if you retire before age 59 1/2.

A financial advisor can help you weigh these options, particularly once your portfolio reaches seven figures. The stakes are higher, and small decisions around tax strategy, asset location, and withdrawal sequencing can translate into tens of thousands of dollars over a retirement that may span 30 years or more.

The case for staying invested

While the original poster’s math holds up, stopping contributions entirely means giving up tangible benefits. At minimum, keep contributing enough to claim your employer match. Beyond that, evaluate whether funneling money into a Roth IRA, taxable account, or additional 401(k) deferrals aligns with your broader financial picture.

Retirement planning is not just about hitting a number. It is about building resilience, optimizing taxes, and creating options. Continued saving, even when you are already on track, strengthens all three. If you are fortunate enough to be in this position, use it to go beyond “enough” and build a foundation for true financial independence and generational wealth.

Editor’s note: This article has been updated to reflect Morningstar’s 2025 safe withdrawal rate guidance of 3.9%, current 2026 contribution limits for 401(k) and Roth IRA accounts, and expanded discussion of alternative retirement savings strategies.