Baby Boomers are nearing retirement, if they aren’t there yet. For many members of this generation, those golden years may look far less golden than expected. Too many Boomers are making decisions right now that could create serious financial problems down the road, and the data paints a sobering picture.

Here are three ways Boomers are setting themselves up for a painful retirement.

1. Their work plans aren’t realistic

One of the most damaging miscalculations Boomers make is assuming they can simply work longer to close any savings gap. According to the Transamerica Center for Retirement Studies, 56% of Boomers plan to work until at least age 70 or never retire at all. That sounds like a reasonable cushion, but the actual numbers tell a different story.

Data from the Center for Retirement Research at Boston College puts the average retirement age at 65 for men and 63 for women. People stop working far earlier than they intend, often because health problems, disability, or caregiving obligations force the issue. Nationwide, roughly 31% retire earlier than planned due to health issues alone, according to EBRI and SSA research. A Boomer banking on a decade of additional earnings to fund retirement could find that runway suddenly cut short, leaving a nest egg that simply was not ready to support two or more decades of withdrawals.

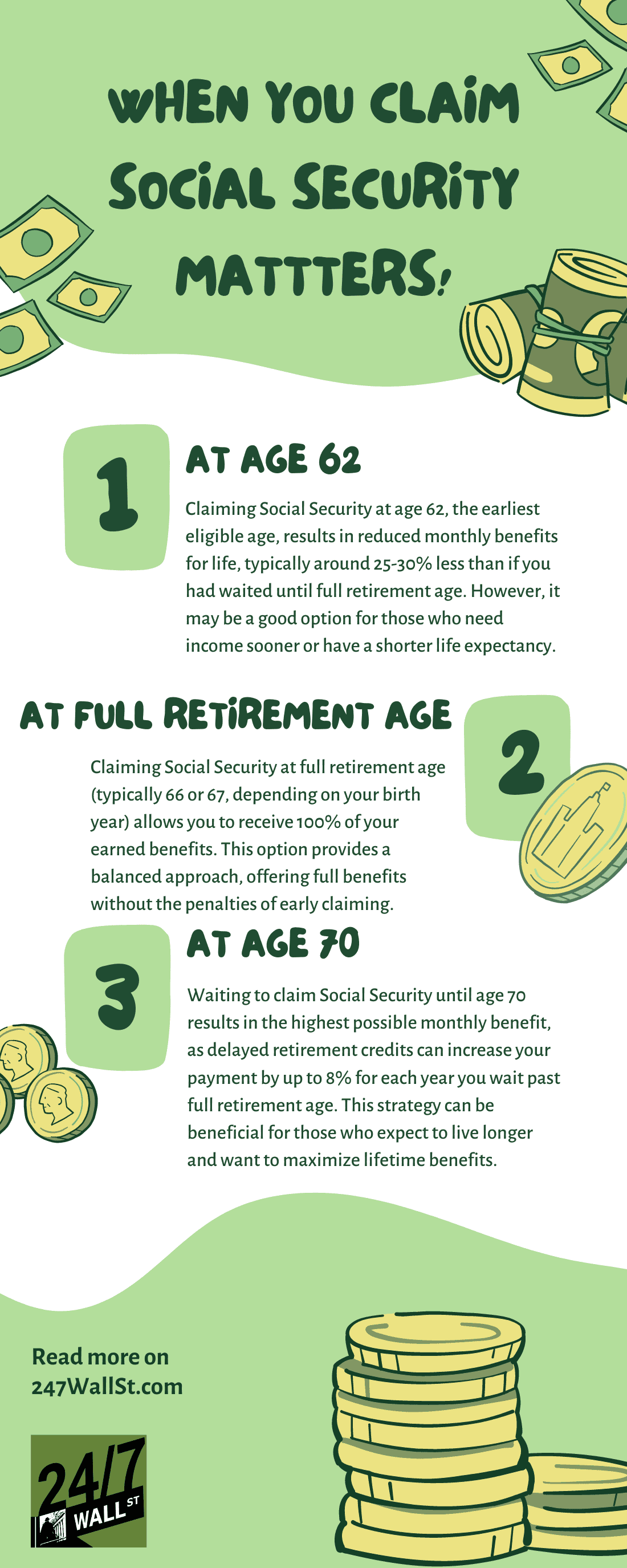

2. They’re planning to over-rely on Social Security

Social Security was never designed to be a full income replacement, and Boomers who treat it as one are in for a rude awakening. The Transamerica report found that 43% of Boomers expect Social Security to be their primary source of retirement income. The Social Security Administration itself says the program is designed to replace roughly 40% of pre-retirement income for the average worker, and that number falls even shorter for higher earners.

The math got harder in 2026. The 2.8% Cost of Living Adjustment (COLA) added around $56 per month to the average Social Security check, but that raise was largely absorbed by a nearly 9.7% jump in Medicare Part B premiums, which rose to $202.90 per month. According to the Center for Retirement Research at Boston College, that Part B increase will eat up more than a quarter of the COLA for most beneficiaries. Research from Boston College also notes that Part B premiums as a share of the average Social Security benefit will hit an all-time high of 9.4% in 2026, marking the third consecutive year that Medicare premium growth has outpaced the COLA.

There is a partial offset available. The One Big Beautiful Bill Act, signed into law on July 4, 2025, created a new senior bonus deduction worth up to $6,000 per person ($12,000 for married couples when both spouses qualify) for taxpayers age 65 and older. The IRS confirms this deduction applies to tax years 2025 through 2028 and phases out for single filers with modified adjusted gross income above $75,000 and joint filers above $150,000. By lowering taxable income, it can help some Boomers reduce the amount of their Social Security benefits subject to federal tax. Even so, without a pension or substantial savings, Social Security alone cannot sustain a comfortable standard of living.

3. They aren’t saving enough

The savings picture is the most troubling piece of the puzzle. According to Federal Reserve Survey of Consumer Finances data compiled by NerdWallet, the median household retirement savings for Americans aged 55 to 64 is approximately $185,000, while households headed by someone at or near retirement age hold a median of around $200,000. Fidelity’s Q4 2025 analysis of 24.8 million 401(k) participants found that Boomers carried an average 401(k) balance of $270,800, but averages are skewed sharply by wealthier savers. The median tells a harder truth.

Using the traditional 4% withdrawal guideline, a $185,000 nest egg would generate roughly $7,400 per year in retirement income, or about $617 per month. Many financial planners now advocate a more conservative 3.7% rate for new retirees to reduce the risk of draining accounts too quickly in a volatile market environment. At that rate, the same $185,000 produces just under $6,850 annually. Vanguard’s 2025 retirement outlook found that the median Boomer faces an estimated annual shortfall of around $9,000 relative to their projected spending needs, with only about 40% of Boomers on track to maintain their current standard of living in retirement.

The risks do not stop at the account balance. Northwestern Mutual research found that roughly 40% of Boomers say it is at least somewhat likely they will outlive their savings. Boomers who are behind have limited but real options: delaying retirement even by a year or two improves outcomes significantly, catch-up contributions to a 401(k) allow savers aged 60 to 63 to contribute up to $35,750 in 2026, and diversifying into assets with lower correlation to equity markets can reduce the damage a downturn does in the critical early years of retirement. The window to act is narrow, but it is still open.

Editor’s note: This article was updated to reflect the Federal Reserve and NerdWallet median savings figures for Boomers near retirement age, the confirmed 2.8% Social Security COLA and $202.90 Medicare Part B premium for 2026, the new $6,000 senior bonus deduction enacted under the One Big Beautiful Bill Act (valid 2025 through 2028), and Vanguard’s 2025 finding that the median Boomer faces a roughly $9,000 annual shortfall in retirement.

Contact [email protected] for any questions or corrections.