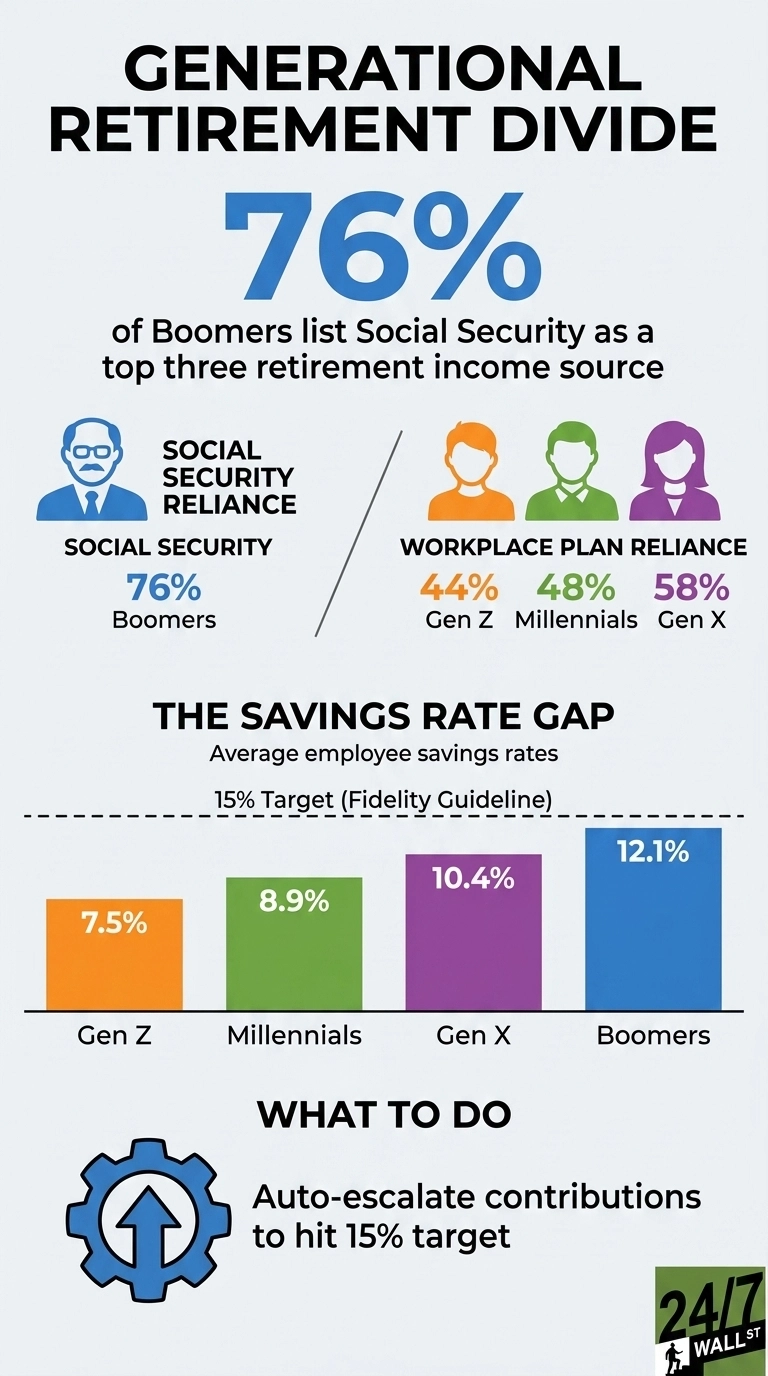

Fidelity’s 2026 retirement study draws a clear line between generations based on where they expect their retirement income to come from. The data begins with the finding that 76% of Boomers list Social Security as a top-three source of retirement income, while younger workers point elsewhere. In addition, 58% of Gen X, 48% of Millennials, and 44% of Gen Z cite workplace retirement plans as a primary source. The split matters because each path carries a distinct vulnerability profile, with asymmetric risks on each side.

Two different retirement engines

Boomers came of working age before auto-enrollment, target-date funds, and Roth 401(k)s became standard plan features. Their retirement security was always going to lean on a guaranteed government benefit. Aggregate Social Security receipts grew from $1.5 trillion in Q1 2024 to $1.6 trillion in Q1 2026, reflecting both demographic shifts and benefit growth. For Boomers already drawing checks, that flow is the floor of their monthly income.

Younger workers’ bet on workplace plans is structurally different, and their income depends on contribution discipline, employer match generosity, market returns over decades, and avoiding early withdrawals. Fidelity’s data shows the average Boomer 401(k) balance at $269,100, Gen X at $215,600, Millennials at $82,600, and Gen Z at $18,000. Early balances are small by design, since compounding does most of the heavy lifting in the final two decades of accumulation.

Why the dependency profiles diverge in risk

Boomers’ exposure is mostly to political and inflationary risks. Social Security’s trust fund faces well-documented solvency concerns, and any fix will likely combine revenue increases and benefit adjustments. Core PCE, the Fed’s preferred inflation gauge, rose from 126.121 in June 2025 to 129.63 in April 2026, meaning the annual cost-of-living adjustment has to keep pace just to maintain purchasing power. Retirees with limited savings outside the program absorb any shortfall directly.

Younger generations face market and behavioral risk. While Fidelity’s data shows the overall average 401(k) savings rate holding steady at a healthy 14.2%, individual generation paths vary. Fidelity’s own guidance suggests a combined employee and employer savings rate of 15%, and currently, Gen X is the standout group, consistently pushing past the 15% target and the only one above it.

The macro backdrop is tightening at the wrong time for younger savers, with the personal savings rate falling from 6.2% in Q1 2024 to 3.7% in Q1 2026, and consumer sentiment hit 49.8 in April 2026, below the 60 recessionary threshold. Tighter household cash flow translates directly into smaller contributions and more early withdrawals.

The planning gap inside the data

Fidelity also finds that those with a retirement plan are more than 2x as likely to feel confident about retirement, and among retirees, 81% with a plan say they have enough money to last their lifetime, compared with 45% without one. That gap extends beyond psychology, and plans force decisions about Social Security claiming age, withdrawal sequencing, and account consolidation that meaningfully shift outcomes.

Account fragmentation may be the underrated risk for workplace-plan-reliant generations: 23% of Americans with retirement accounts hold multiple unconsolidated balances from past or current jobs, and only 32% have rolled over old balances into their current workplace plan. Forgotten accounts often sit in default investments, outdated allocations, or higher-fee tiers, quietly dragging down long-run returns.

What the divide actually means

Affordability sits behind both stories. Among Americans uncertain about when they will retire, 42% overall, and 47% of Gen X, cite the inability to afford retirement as the reason. The Boomer concentration on Social Security reflects a generation arriving at the finish line with a fixed benefit doing the heavy work. The younger generation’s focus on workplace plans reflects a cohort whose outcomes are still being shaped by contribution rates, market paths, and whether old accounts are tracked.

Three implications follow from the data, starting with the reality that for near-retirees, the relevant scenario is one in which COLA trails Core PCE over a multi-year stretch. For Gen X and Millennials, combined deferral rates remain below the 15% target Fidelity recommends, with auto-escalation a common mechanism to close the gap. For workers with old 401(k) balances, the 23% who leave accounts uncoordinated typically bear the costs of fees and allocation drift.

Contact [email protected] for any questions or corrections.