In fiscal year 2026, the Congressional Budget Office estimates that the federal budget deficit will total $1.9 trillion, which is 5.8% of the GDP. By 2036, the deficit is expected to grow to $3.1 trillion and total 6.7% of GDP. These numbers are much larger than the 3.8% average deficit over the past 50 years.

With the country borrowing so much, on top of an already-large debt balance, rising interest costs have become a real problem, especially as interest rates have surged in the post-pandemic era. While rates are nowhere near the 20% peak they hit in the early 1980s, the Federal Reserve has kept its benchmark rate above recent norms since 2022 to curb the inflation resulting from supply chain disruptions and COVID-19 stimulus. The Federal Reserve is widely expected to raise interest rates again in 2026 despite hopes that inflation would finally cool to the point where easing was possible.

Rising rates only compound the problem of ballooning debt, as in fiscal year 2025, nearly 20% of the federal government’s revenue went to paying interest on the national debt. By 2036, those payments will increase to the point where a quarter of all tax revenue collected goes to interest. None of this is good news for taxpayers, but it is especially bad news for Social Security retirees who are facing a potential Doomsday Scenario by 2032.

Social Security is driving deficits, as borrowing grows more expensive

While the government has a lot of expenditures, two of the country’s most important and most popular programs are huge drivers of the deficit. Social Security and Medicare.

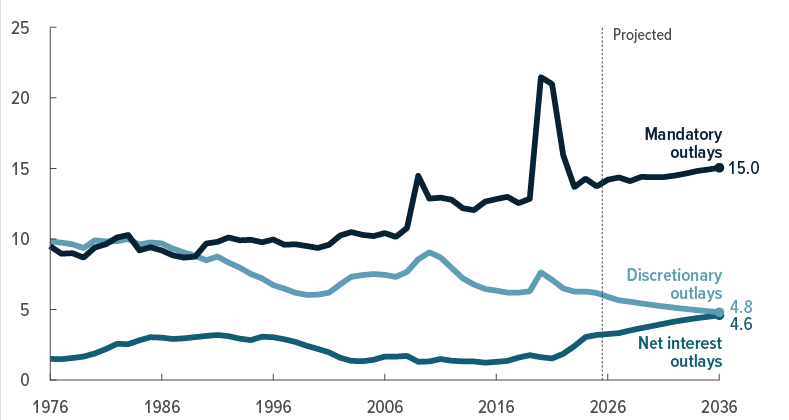

Both Social Security and Medicare are considered mandatory spending because outlays are controlled by existing laws, rather than by budget appropriations. Discretionary spending includes spending that must be approved and signed into law each fiscal year, including transportation, housing, environmental protection, and national defense. As the chart below shows, the costs of the country’s entitlement programs, which are considered mandatory outlays, are taking up an increasingly large share of GDP and leaving few options for bringing the deficit under control absent substantial revenue increases or major benefits reductions.

With mandatory outlays estimated to reach 15% of GDP by 2036, while discretionary outlays plummet to 4.8%, the costs of Social Security, Medicare, and other entitlement programs will become increasingly difficult to sustain, especially as rising interest rates put more pressure on the budget.

Social Security faces a day of reckoning in 2032

Social Security and Medicare collectively account for close to 40% of federal spending, with Social Security representing around 22% of the federal budget and Medicare around 13% to 14% of outlays. As Baby Boomers age, spending on these programs will only increase, and mandatory outlays as a percentage of the federal budget will rise. Unfortunately, as the cost of benefits climbs, Social Security is facing serious financial trouble.

The Social Security Board of Trustees released its report on June 9, and the news wasn’t good.

Social Security operates two trust funds: the Old-Age and Survivors Insurance (OASI) Trust Fund and the Disability Insurance (DI) Trust Fund. According to the most recent Trustees’ Report, with expenditures exceeding collected revenue, the OASI Trust Fund is projected to be depleted in 2032. And this is the Doomsday scenario for Social Security.

Social Security will only be able to pay benefits out of the revenue coming in, and there would be enough money to pay just 78% of scheduled benefits, leading to an automatic 22% cut. Social Security is not allowed to draw from the general fund under current law, which would mean that there’s no money to pay the extra benefits unless Congress acts.

Unfortunately, with interest costs already taking up so much revenue, and with deficits already running so high, Congress has little room to appropriate extra funds to cover the shortfall. If lawmakers don’t act soon, this could create a true crisis point for seniors in as little as six years.

Contact [email protected] for any questions or corrections.