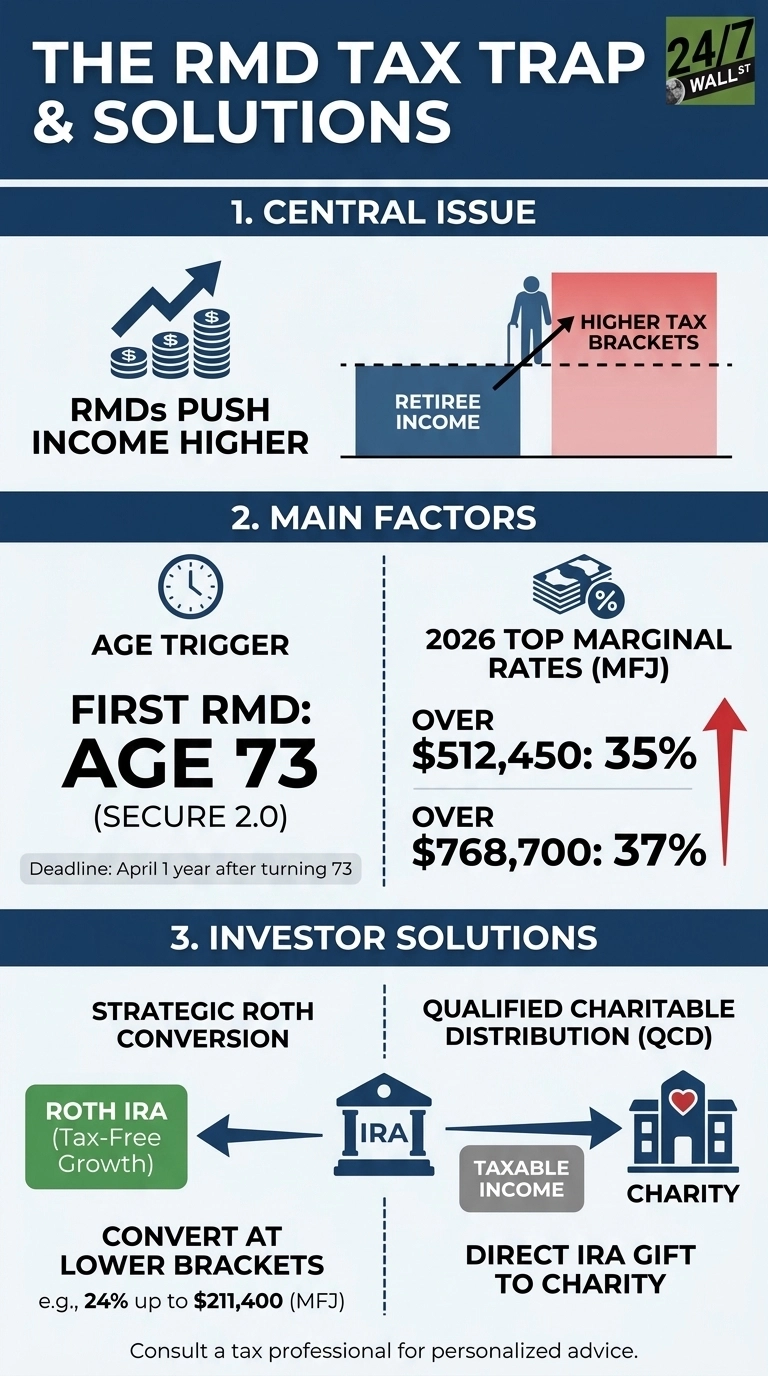

Many retirees face Required Minimum Distributions that arrive with large tax bills attached. Under SECURE 2.0, the first RMD is due by April 1 of the year after turning 73. The age rises to 75 in 2033.

The IRS uses the Uniform Lifetime Table to size an RMD. At age 73, the divisor is 26.5, applied to the prior year-end IRA balance. Consider a retiree with $1.8 million in retirement assets. He has a traditional IRA, a pension covering fixed expenses, and Social Security topping the income stack. His IRA closed the prior year near $2.1 million after a strong market run, which produces a first RMD of roughly $80,000.

Stack that $80,000 on top of existing income. A pension in the mid five figures plus a Social Security benefit (boosted by the 2.8% COLA for 2026) already lifts him well above the standard deduction of $32,200 for married filing jointly. The RMD lands on the last dollars earned, filling the middle brackets and pushing the top slice into the 35% band. For a high-income household, the top layer of that $80,000 gets taxed at the maximum federal rate, plus IRMAA surcharges on Medicare Part B and D.

Decades of tax deferral compress into non-optional income at exactly the moment he has the least flexibility to manage it. Every year he does nothing, the problem worsens.

The Roth Conversion Window He Already Missed (Partly)

The most effective lever is bracket-filled Roth conversions in the years between retirement and the first RMD. Between 63 and 72, most retirees sit in the 22% or 24% band. Converting enough IRA money each year to fill the 24% bracket, which runs up to $211,400 for MFJ in 2026, moves those dollars into a Roth where they grow tax-free and never trigger an RMD. Five or six years of conversions can shrink the IRA base by hundreds of thousands, dropping future RMDs enough to keep the household in the 24% bracket permanently.

At age 73, that window is narrower but not closed. He can still convert above the RMD each year. The RMD itself cannot be converted, but any additional withdrawal or conversion done at 24% or 32% is cheaper than letting the account compound into future 35% and 37% distributions. If future withdrawals will be taxed higher than today’s conversion rate, the Roth wins. That delta is 24% now versus 35% or 37% later.

Qualified Charitable Distributions

If he already gives to charity or is considering it, the Qualified Charitable Distribution can lower his tax burden. A QCD sends IRA money directly to a qualifying charity, counts toward the RMD, and never appears in adjusted gross income. The 2025 limit is roughly $108,000 per person and indexed going forward. Redirecting $30,000 or $40,000 of the RMD through QCDs shaves the same amount off taxable income, and those dollars would otherwise have been taxed at 35%.

Compare that to writing a check from taxable savings. The standard deduction of $32,200 means most retirees no longer itemize, so a cash donation buys zero tax benefit. A QCD delivers the full deduction economics without itemizing.

What to Do First

- Model the next 10 years of RMDs, not just this one. The divisor drops every year, and the balance grows. A projection at reasonable return assumptions shows the trajectory. If year-10 RMDs push deeper into the 37% bracket, aggressive conversions now are almost certainly worth it.

- Set a QCD target before December. The QCD must go directly from IRA custodian to the charity to qualify. Personal checks written to the charity from a distribution already received do not count.

- Avoid taking the RMD as a January lump sum with no tax withholding plan. Under-withholding on an $80,000 distribution can trigger safe-harbor penalties. Either withhold at the marginal rate at the source or make estimated payments.

A fee-only advisor is likely worth the cost here because the sequencing of conversions, QCDs, and IRMAA thresholds is a multi-year optimization, not a single-year fix.

Contact [email protected] for any questions or corrections.