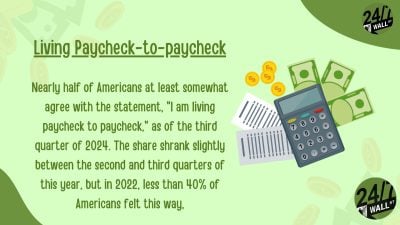

The 63% of adults who told the Federal Reserve they could cover an unexpected $400 expense with cash or its equivalent, according to the 2026 report on 2025 household well-being, represent the widest definition of financial resilience the government tracks. It is a low bar by design. The question asks whether a household has $400 available today, in checking, savings, or on a card that can be paid off at the next statement. It stops there. One month of retirement spending sits at a different order of magnitude.

Recent Bureau of Labor Statistics data cited in retirement studies put typical retiree household spending near $5,000 per month, with housing, healthcare, and food accounting for most of it. Covering that from savings requires roughly 12 times the $400 threshold. The group able to do it comfortably is a much smaller share of the population than the 63% headline suggests.

What One Month of Retirement Actually Costs

Retirement expenses cluster in categories that do not shrink much with age. Personal consumption data from the Bureau of Economic Analysis shows housing at $3,950.3 billion in annualized spending in May 2026 and healthcare at $3,716 billion, the two largest service categories in the national accounts. Combined with food, essential categories account for roughly 42% of total personal consumption. Retirees face the same categories with fewer income streams to meet them.

Against that, Vanguard’s How America Saves 2026 preview reports a median 401(k) balance of $44,115 across the plans it administers, alongside an average of roughly $167,970. The mean is lifted by a smaller number of large balances; the median describes the middle of the distribution. A $44,000 balance drawn at the 4% guideline produces roughly $147 a month before taxes, well short of a typical retiree’s grocery bill.

Why the Cushion Is Thinner Than It Looks

The household savings picture behind the $400 headline has been narrowing. The personal saving rate fell to 3.9% in the first quarter of 2026, down from 6.2% two years earlier, even as per capita disposable income rose to $68,391. Income grew while the share flowing into savings shrank.

Once inflation is applied, wages show the same squeeze. Average hourly earnings reached $37.64 in June 2026, up from $36.36 a year earlier. In inflation-adjusted terms, real average hourly earnings were $11.23 in May 2026, below the $11.32 reading from May 2025. Nominal pay is rising, while hourly purchasing power has slipped.

Median usual weekly earnings for full-time workers were $1,235 in the first quarter of 2026. Average annual consumer expenditures ran $78,535 in 2024, the most recent full year from the Consumer Expenditure Survey. The distance between typical earnings and typical annual outlays explains why the $400 test is easier to pass than the one-month-of-retirement test.

The Stress Signals Are Mixed

Household stress indicators sit in a middle zone. The credit card delinquency rate was 2.92% in the first quarter of 2026, inside the Federal Reserve’s normalizing range and well below the peaks seen in historical financial crises. Unemployment was 4.2% in June 2026, a slight uptick from 4.1% a year earlier.

The University of Michigan Consumer Sentiment Index registered 44.8 in May 2026, below the 60-point recessionary threshold and down from the July 2025 reading of 61.7, signaling weaker household confidence. Core PCE, the Fed’s preferred inflation gauge, rose 0.1% in May 2026 (or 3.4% year-over-year), keeping upward pressure on the essential categories retirees cannot avoid.

Where the Two Numbers Diverge

The $400 benchmark measures short-term liquidity. The one-month-of-retirement benchmark measures whether a household has built a savings buffer sufficient to replace income for a sustained period. The first can be answered by a paycheck-timed transfer. The second requires years of accumulation at a rate that the current 3.9% national savings rate does not produce for most households. Both questions describe the same balance sheet over different time horizons and arrive at different answers.

Contact [email protected] for any questions or corrections.