It’s been a tough road for telecom investors of late. Very high dividends just have not enticed investors back into telecom giants Verizon Communications Inc. (NYSE: VZ) and AT&T Inc. (NYSE: T). The defensive nature of telecom and high yields just are not tempting investors out of the growth stock areas in the market.

After some fresh analyst target hikes, some investors might think that after each company manages its transformation, finally there may be an opportunity. There is still some commonality between these two giants, but the differences in expectations have to be considered here.

It’s no secret that the wireless price and service four-way war has been at the expense of AT&T and Verizon, but AT&T is still rolling in DirecTV and it still wants to acquire Time Warner. Verizon has now rolled up AOL and Yahoo and wants to grow in mobile content and mobile advertising.

Verizon generated a slight negative total return of −0.8% in 2017, rather than what was originally expected to be a total return of 2.8%. After shares closed 2017 at $52.93, the consensus price target was $51.83 at the start of 2018. That and the whopping 4.46% dividend yield would imply an expected return of about 2.4% in 2018.

[nativounit]

AT&T was down just one cent at $36.72 after Barclays raised its target to $41 from $39. This implies upside of 11.7% in 2018, and the 5.45% dividend yield suggests an expected total return of better than 17% if Barclays is proven right. Also, KeyBanc Capital Markets maintained its Sector Weight rating on AT&T but raised its target to $38 from $35. Deutsche Bank raised its AT&T price target to $41 from $37 on January 10.

While Barclays raised its target price on Verizon to $56 from $50, the big surprise here is that the shares dropped another 27 cents to $51.39 in midday trading. On January 2, KeyBanc Capital Markets maintained its Sector Weight rating but raised its price target to $53 from $50. On January 10, Verizon’s target was raised to $56 from $48 at Deutsche Bank.

Barclays noted earlier in January that AT&T is planning a mobile 5G launch in 2018, targeting a dozen markets late in 2018 as the company thinks it can bring the 5G service to market faster than what was previously expected. in that same call, Barclays noted that commercial smartphones that support massive MIMO (large-scale antenna systems) are expected to hit the market during the first half of 2018.

Thomson Reuters has AT&T valued at 12.3 times expected 2018 earnings. Its consensus target price on AT&T has not changed enough from the current $39.42 consensus target price, but that is down from a $41.00 consensus target just 90 days ago. The consensus analyst targeted tax rate for AT&T in 2017 was 34.6%.

[recirclink id=436966]

Thomson Reuters has Verizon valued at 12.9 times expected 2018 earnings. Its consensus price target of $52.82 is up more than $1.00 from 30 days ago and from $49.68 just 90 days ago. The consensus tax rate for Verizon in 2017 was 33.95%.

AT&T shares were already down over 5% on Wednesday, and its stock has had a negative return of more than 10% over the trailing 12 months.

While Verizon was down over 2% so far in 2018, it’s important to keep in mind that Verizon would have been far worse in 2017 had it not risen 18% in the second half of the year.

We wanted to finish with a contrary view so both sides are represented here. According to Morgan Stanley, cable may still hold up just fine for AT&T and Verizon. AT&T’s upgrade plans and Verizon’s 5G penetration targets will not derail cable’s growth in the broadband market. Morgan Stanley’s view is that the cable sector may benefit from tax reform as much as any sector in the market.

[wallst_email_signup]

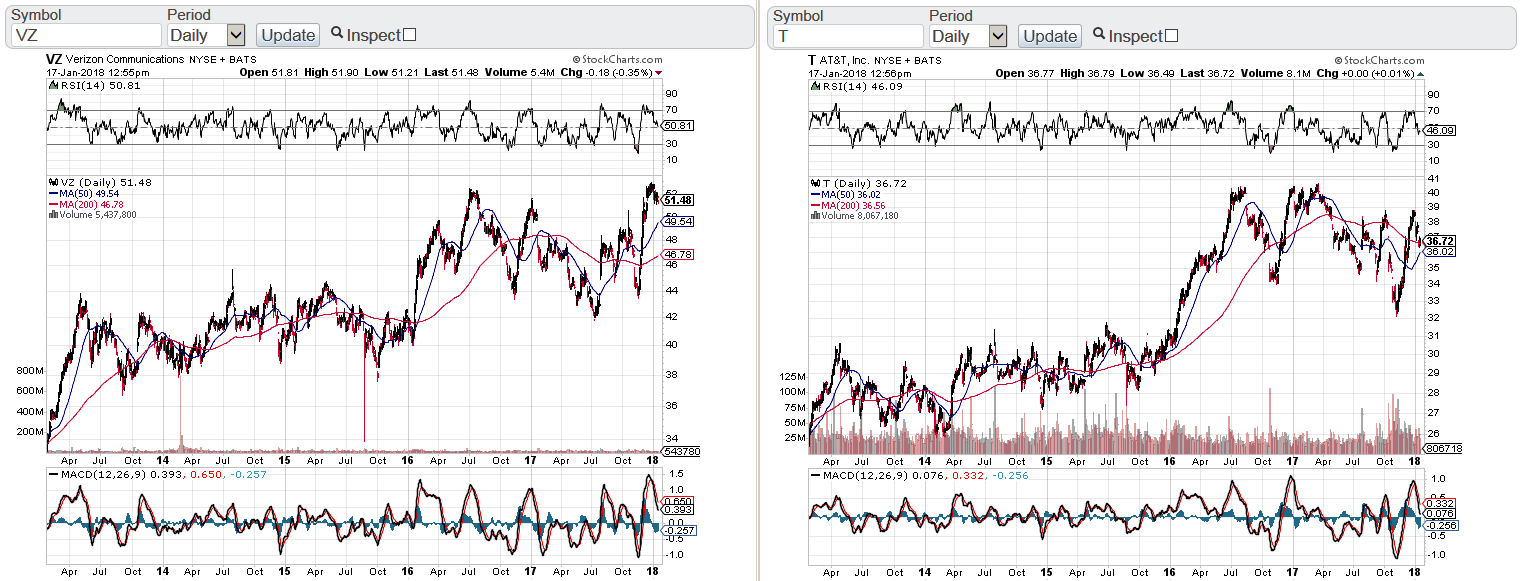

Also included are five-year stock charts from StockCharts.com:

Contact [email protected] for any questions or corrections.