If the federal government defaults on its debt, the recession could put millions of Americans out of work. However, the first wave of trouble will be what people pay for home mortgages, particularly for those with floating rates. People with fixed rates will be lucky. (The national debt under every president for the past 100 years.)

[in-text-ad]

The federal government has hit its borrowing limit of $31.7 trillion. Federal officials are juggling several sets of expenditures to extend the day this will affect the ability of the government to pay its bills at all. The expected end date of these efforts will be in early June.

[nativounit]

The debt issued by the U.S. government is considered the safest in the world. The United States has never defaulted, and every time the debt ceiling has been reached, Congress has raised it. At this point, the Republicans who control the House of Representatives want sharp cuts in federal spending to raise the limit. The Biden administration says it will not accept this solution.

The more risk loans take on, the higher the interest rate. The higher interest payments are meant to offset the chance of a loan being paid. Most interest rates in the United States are tied to the rate the government pays to raise money.

[wallst_email_signup]

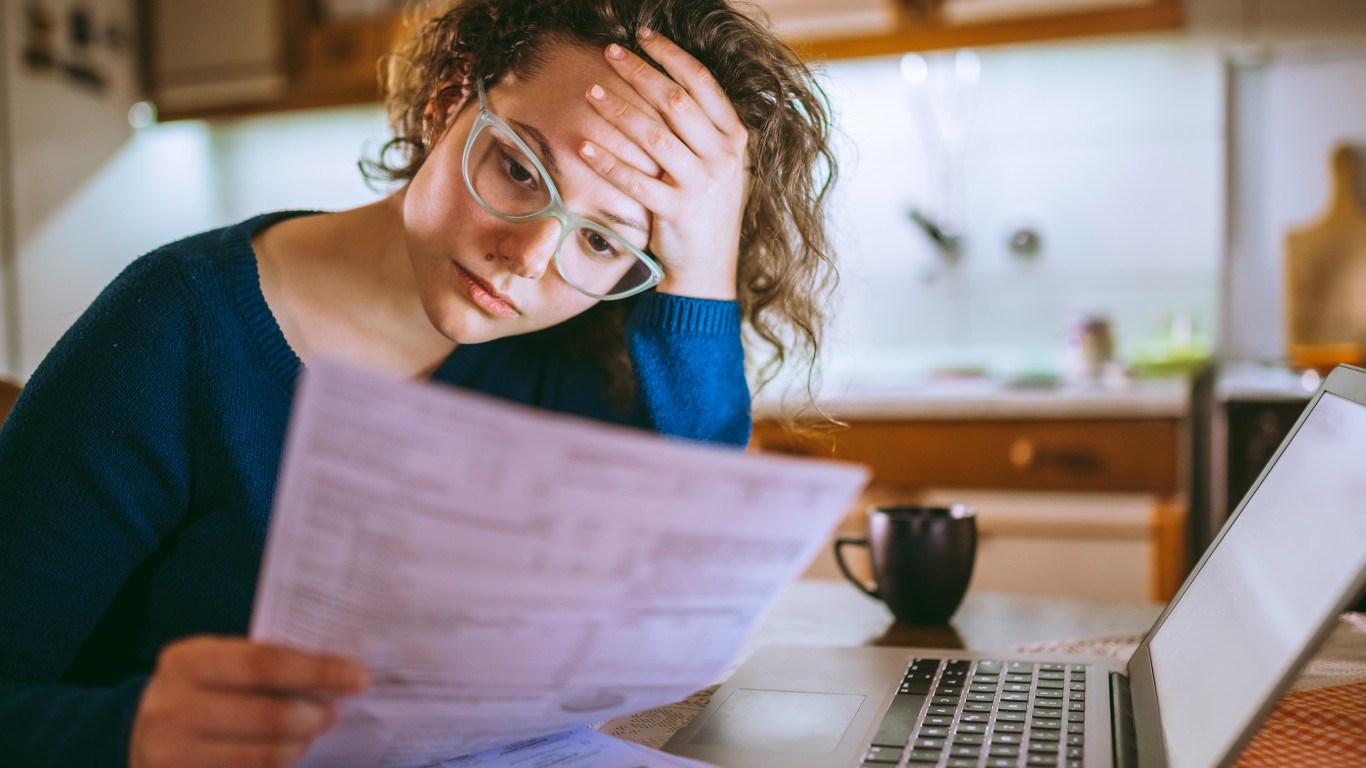

Many Americans locked in interest rates at or about 3% when the Federal Reserve kept rates at historic lows. Those rates have risen recently but have not skyrocketed. Even with the moderate rise in interest rates, some Americans have variable mortgage rates reaching 7%.

[recirclink id=1199332]

A default would raise the sum the federal government pays in interest rates to 6% or 7% within days. Federal government debt suddenly will become risky. That means variable rate mortgages could spike to 10% almost overnight. People would be faced with cutting costs simply to make home payments. In turn, the housing market could buckle under foreclosures driven by the higher mortgage payments.

Contact [email protected] for any questions or corrections.