The announced cuts to capital spending (capex) in the oil and gas exploration and production (E&P) business average over 50%, with cuts of up to 80% at some firms. One natural gas producer has said it will cease all drilling in 2016, reducing its capex to $125 million from $1.8 billion in 2015.

We have taken a look at several independent primarily oil E&P companies that have announced large capex cuts for 2016. According to a report from Nomura, the five largest year-over-year percentage cuts to capital spending are:

- Devon Energy Corp. (NYSE: DVN), down 81%, from $5.31 billion to $1 billion

- Whiting Petroleum Corp. (NYSE: WLL), down 80%, from $2.46 billion to $500 million

- Murphy Oil Corp. (NYSE: MUR), down 77%, from $2.55 billion to $580 million

- Energen Corp. (NYSE: EGN), down 76%, from $1.15 billion to $275 million

- Oasis Petroleum Inc. (NYSE: OAS), down 76%, from $820 million to $200 million

And that natural gas producer? That’s Southwestern Energy Co. (NYSE: SWN), reported to be slashing capex from $1.8 billion to just $125 million, a drop of about 93%.

[recirclink id=318468]

Not including Exxon, Chevron and Occidental, Nomura’s coverage universe of 34 companies accounts for 35% of the Lower 48’s onshore oil production, and the research analysts see production declines of 11% to 13% between the end of 2015 and the end of 2016. That amounts to about 800,000 to 900,000 barrels of oil per day. That onshore decline is expected to be partially offset by an offshore production increase of about 250,000 barrels a day by the end of this year.

The analysts noted:

… North American onshore, unconventional production is not always the high cost producer (although it has a big bell curve), but it is clearly the most flexible and the worst financed. That can be a toxic combination.

Nomura also warns against a “self-defeating rally” encouraged by currently rising prices. The analysts say that global demand and Saudi Arabian policy are likely to be the primary drivers of oil market fundamentals in the intermediate term. And here’s the catch:

Declines in [North American] onshore are supportive [of higher prices], but the more impactful declines will ultimately emerge from longer-cycle deferred/cancelled projects, which are anticipated in mid to late 2017. This is a period where the world will need incremental, shorter cycle capacity (both Saudi and US onshore), in our view.

In other words, no real recovery in U.S. onshore oil prices until the middle of next year.

Only by hoarding cash, hedging and continuing to do business on the basis of operating cash flow do these companies stand a chance of surviving until Nomura’s estimated turnaround. And some of these E&Ps already have taken some strong measures.

Devon sold 69 million new shares in mid-February at $18.75 per share. The company also cut its dividend from an annual payout of $1.00 to $0.24 and said it would reduce its workforce by about 20% in the first quarter of 2016. Although shareholders didn’t like the sound of all that at the time, shares closed at $24.79 on Monday, not even a month after the announcement.

Whiting said it will suspend all hydraulic fracturing (fracking) and spend about $440 million of its 2016 capex to shut down its drilling and completion operations beginning in the second quarter. The company expects to close the year with 73 drilled, uncompleted wells in the Bakken shale play and 95 drilled, uncompleted wells in the Niobrara shale play.

Energen, like Devon, sold more than 18 million new shares to raise about $381 million in February. The company last week also hedged an additional 5.2 million barrels of 2016 production at an average price of $41.47 per barrel. Energen has now hedged about half (6.3 million barrels) its expected production midpoint estimate for 2016 at an average price of $45.33 per barrel. That’s nearly $9 a barrel higher than the current price.

Oasis figures it can get by in 2016 if oil sticks around $35 a barrel. The company projected cash flow from adjusted EBITDA less cash interest will cover its $200 million in drilling and completion capex. Oasis has hedged about 71% of its production hedged at $51 per barrel.

[recirclink id=320026]

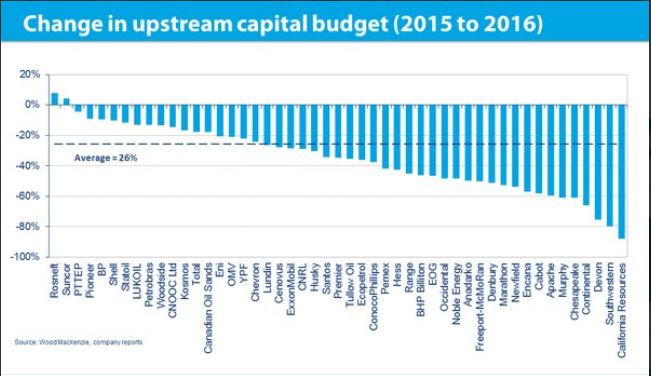

The following chart was included in a tweet from research firm Wood Mackenzie. It shows the decline in projected 2016 upstream capex compared to 2015 totals. The numbers are slightly different from Nomura’s, but the graphical presentation dramatizes what’s happening.

Benchmark West Texas Intermediate (WTI) crude oil for April delivery traded down about 2.7% in the late morning on Tuesday at $36.16. Crude for May delivery traded down about 2.3% at $37.93. The year-to-date high for WTI is just over $40 a barrel, set early in January.

Contact [email protected] for any questions or corrections.