Below I will present a simple quantitative method that exploits momentum in relative returns across a wide set of asset classes. The strategy is examined since 1972 in an allocation framework utilizing a combination of diverse and publicly traded asset class indices including US Stocks (S&P 500), Foreign Stocks (MSCI EAFE), Commodities (GSCI), REITs (NAREIT), Cash (90-Day Commercial Paper), and United States Government Bonds (10-Year Treasury Bonds).

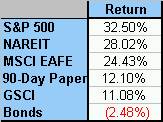

The most simple measure of momentum I can think of (and the one cited in the GS primer) is trailing 12-month absolute returns. To make matters even simpler, and improve the tax consequences, the system will only update once every year at year end. You begin with a simple ranking of absolute performance – the example to the right is year end 1980:

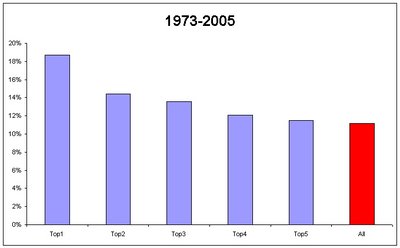

The optimum risk-adjusted portfolio is the Top 3 asset portfolio, returning over 250 bps more than the equal weighted with slightly higher volatility, and only 2 down years since 1973 – and a worst year of only -(3.64)%.

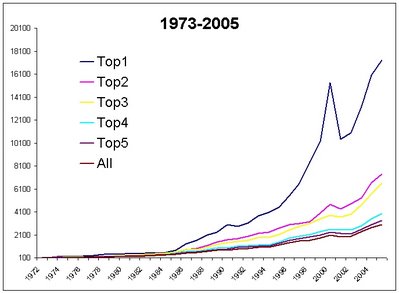

$100 invested in the 6 asset class portfolio would be worth $3003.03 year end 2005, while $100 invested in the Top1 strategy would be worth $17,333.15.

Example ETFs reflecting the asset classes discussed in article are:

Example ETFs reflecting the asset classes discussed in article are:

{kind=link}