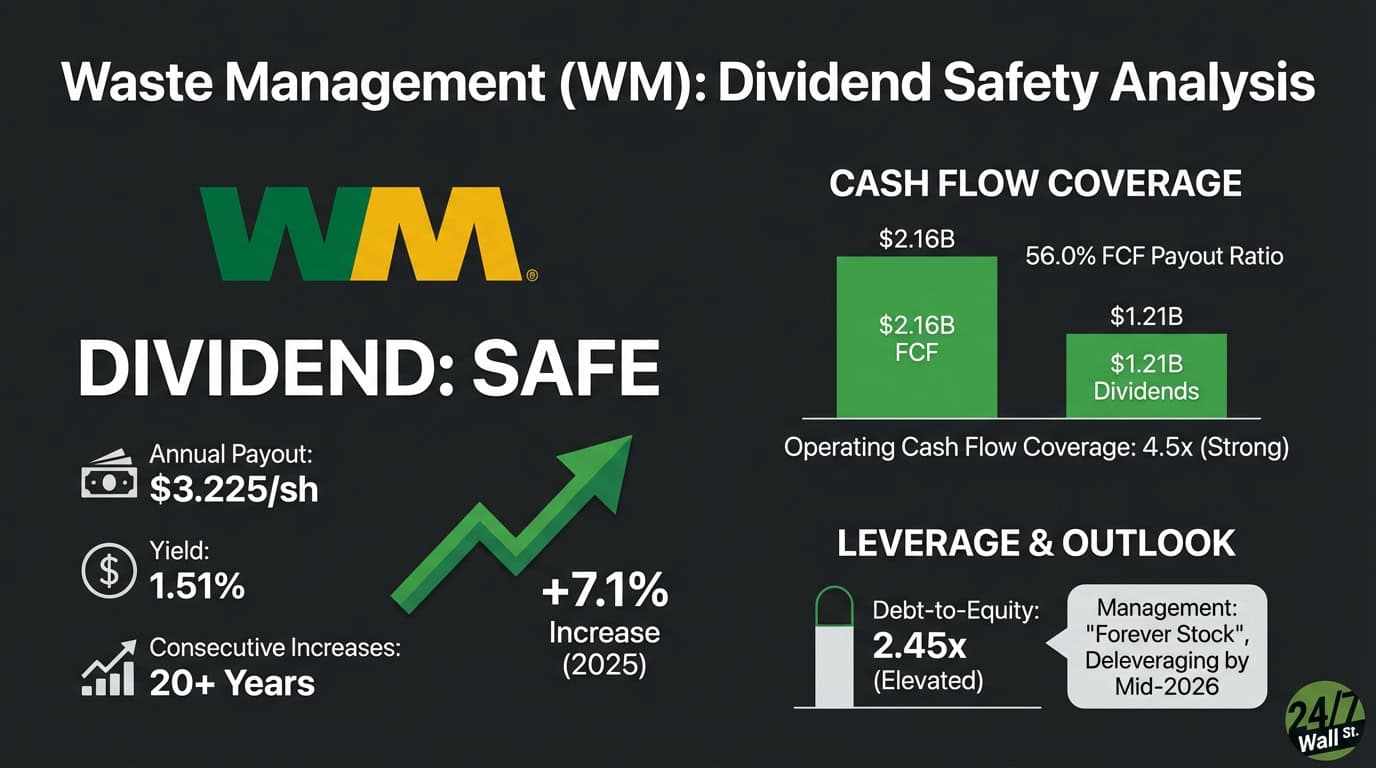

Waste Management (NYSE: WM | WM Price Prediction) pays an annual dividend of $3.225 per share, yielding 1.51%. The company raised its payout by 7.1% and has maintained over 20 consecutive years of dividend increases. After a sharp 20.7% earnings decline in Q3 2025, income investors are asking: can this dividend withstand pressure?

| Metric | Value |

|---|---|

| Annual Dividend | $3.225 per share |

| Dividend Yield | 1.51% |

| Consecutive Years of Increases | 20+ years |

| Most Recent Increase | +7.1% (2025) |

| Dividend Aristocrat Status | No |

Cash Flow Covers the Dividend With Room to Spare

Waste Management paid $1.21 billion in dividends against $2.16 billion in free cash flow during 2024, producing a 56.0% FCF payout ratio. That leaves nearly $950 million in retained cash after dividends.

| Metric | 2024 Value | Assessment |

|---|---|---|

| Earnings Payout Ratio | 41.6% | Healthy |

| FCF Payout Ratio | 56.0% | Healthy |

| Operating Cash Flow Coverage | 4.5x | Strong |

The trailing earnings payout ratio sits at 50.9% ($3.225 divided by $6.34 EPS). Over eight years, the FCF payout ratio averaged 49.4%, ranging from 39.8% in 2021 to 62.3% in 2023. Operating cash flow surged 69% from $3.18 billion in 2017 to $5.39 billion in 2024.

Leverage Is Elevated but Manageable

Waste Management carries $23.36 billion in total debt against $9.52 billion in equity, producing a debt-to-equity ratio of 2.45x. That’s elevated, driven by the 2024 Stericycle acquisition.

| Metric | Value | Assessment |

|---|---|---|

| Debt-to-Equity | 2.45x | Elevated |

| Net Debt-to-EBITDA | 3.19x | Manageable |

| Interest Coverage | 4.4x | Adequate |

| Cash on Hand | $175M | Thin |

Net debt-to-EBITDA stands at 3.19x, within reasonable bounds for a capital-intensive business. Interest coverage of 4.4x provides adequate cushion. CFO Devina Rankin stated in the Q2 2025 earnings call: “Our leverage ratio […] was 3.5x. We remain focused on quickly getting back to targeted leverage levels […] and we currently project we will achieve our target in the first half of 2026.”

Two Decades of Increases, Accelerating Growth

Waste Management has raised its dividend for over 20 consecutive years, including through the 2020 pandemic.

| Year | Annual Dividend | YoY Change |

|---|---|---|

| 2025 | $3.225 | +7.1% |

| 2024 | $3.01 | +6.4% |

| 2023 | $2.83 | +5.2% |

| 2022 | $2.69 | +3.9% |

| 2021 | $2.59 | +3.6% |

The five-year dividend CAGR runs 5.3% annually. Recent growth has accelerated, with 2025 marking the largest increase in years at 7.1%.

Management Calls WM a “Forever Stock”

CEO Jim Fish framed the company’s shareholder value proposition during the Q2 2025 earnings call: “Coming out of last month’s Investor Day, we’re energized by WM’s strategy […] generating consistent long-term value for years to come. It’s our sustained strong results across all market cycles that we believe makes us a forever stock, the type of stock you buy and hold indefinitely.”

The company returned $1.47 billion to shareholders in 2024 through $1.21 billion in dividends and $262 million in buybacks, down from $1.30 billion in buybacks during 2023. The shift toward dividends over repurchases reinforces income investor confidence.

This Dividend Is Safe Despite Earnings Volatility

Dividend Safety Rating: Safe

The 56% FCF payout ratio and 50.9% earnings payout ratio provide substantial cushion. Operating cash flow grew 69% over eight years, and the company maintained dividend growth through the pandemic. Management projects deleveraging to target levels by mid-2026, and Stericycle synergies are tracking to the high end of guidance.

The dividend faces minimal near-term risk given the cash flow coverage, but watch for any guidance cuts to the $2.8 billion to $2.9 billion free cash flow target or if debt reduction stalls.

Contact [email protected] for any questions or corrections.