Still No Q2 Information on Oracle’s Investor Relations Page

Live Blog Update #8 Published

← Back to Full Coverage: Live: Oracle (ORCL) Down 13% After Q2 Earnings - Wall Street Reacts

One note: There’s still no financial information on Oracle’s investor relations page for Q2. That’s a fairly poor showing for the company that puts retail investors at a disadvantage. We monitor hundreds of earnings releases per quarter and this is one of the longer delays we’ve seen.

Contact [email protected] for any questions or corrections.

All Updates from Live Coverage

Shares of Oracle traded as low as $186.23 this morning, but have rebounded to $198 in late trading. That’s an improvement, but is still an 11% drop from yesterday’s close.

Overall, Oracle led to a broad sell-off across the semiconductor space. Even rebounding throughout the day, shares of suppliers like NVIDIA (Nasdaq: NVDA) and Broadcom (Nasdaq: AVGO) are down about 1.5%.

At the end of the day, Oracle missing sales last quarter and raising capital expenditure guidance for 2026 both signaled increasing risk for the stock.

How could Oracle reverse recent losses? For better or worse, the company is now largely tied to the fate of OpenAI. If OpenAI releases new models that impress or financials leak from the company that show continued acceleration, that will also serve as a catalyst for Oracle.

Oracle (Nasdaq: ORCL) shares were trading for roughly $207 per share before the company’s earnings call, but selling accelerated during the call, and shares are now trading for about $194.

A few notes:

- Oracle shares are now trading only slightly above where they traded the Friday before the DeepSeek panic sank AI stocks in late January. That’s a dramatic fall for a stock that was once one of the Nasdaq’s top performers.

- The company added $4 billion in revenue to its Fiscal 2027 guidance.

- The big news that caused shares to fall: 2026 CapEx will be $15 billion higher than forecasted in the first quarter.

It’s worth noting that Oracle shares began falling around the time the company announced its updated capital expenditure figures.

Why did Oracle miss revenues last quarter? Research Semi Analysis reports the company’s Stargate data center in Abilene has faced delays that likely contributed to revenue shortfalls last quarter.

We’ll continue updating this live blog thoughout the day with Wall Street’s reactions to Oracle’s quarter.

There won’t be any major shifts to Oracle’s stock price until the company hosts its conference call at 5:00 p.m. ET. Its very likely the stock will be trading down 6 to 7% before the call.

Is there a chance Oracle can bounce back during the call?

As we’ve noted earlier, Oracle has been the subject of deep negativity from Wall Street in recent months. The company’s stock now trades for significantly less than where it traded before its Fiscal Q1 earnings report when it announced a massive RPO expansion.

Oracle clearly understands the ‘bear case’ being levied at the company, in their earnings release they noted that RPO growth this quarter came from “Meta, NVIDIA, and others.” That is to say, Oracle is trying to highlight that they’re not just a one-trick pony with a massive (and risky) partnership with OpenAI.

How effectively management tells that story tonight will decide whether Oracle’s losses are stemmed when the stock opens tomorrow.

We see the initial earnings reaction as somewhat of an overreaction. Oracle’s slight sales miss says little about the company’s future trajectory. We know the company has a massive backlog of sales, the question is whether they’re taking on too much risk with this OpenAI partnership.

If you leave this page open, we will post one more update after Oracle’s earnings call. That will load automatically if you don’t exit this page and come back later.

In addition, if you haven’t checked it out yet, make sure to subscribe to our AI Investor Podcast. We’ll go into more details on Oracle’s earnings in our next episode.

We thank you for joining us during tonight’s live blog. When companies in your portfolio are reporting make sure to come back to 247wallst.com as we host hundreds of live blogs with our analysts each earnings season.

As we’ve been following, Oracle (Nasdaq: ORCL) reported Fiscal Q2 earnings after the bell and shares are down 5.6% as of 4:20 p.m. ET.

Let’s look at some pros and cons from the quarter.

Pros:

- RPO increased once again to $523 billion, 15% sequential growth. Oracle’s RPO remains above much larger cloud rivals like Amazon or Microsoft.

- Cloud infrastructure revenues topped estimates, hitting $4.1 billion. That’s up 68% from last year.

- Non-GAAP EPS of $2.26 topped estimates.

Cons:

- The company missed on revenue, hitting sales of $16.06 which was below Wall Street’s consensus estimate. In addition, its EPS beat was driven by a one-time gain.

- Margins didn’t top expectations, which led to operating income also missing Wall Street estimates.

- This won’t impact the company’s share price, but it’s now 4:23 p.m. ET, and the company still hasn’t put financials for its most recent quarter on their investor relations page. With earnings hitting newswires nearly 20 minutes ago, that’s a big negative for retail investors.

Overall, Wall Street is currently more concerned with the company’s sales miss last quarter than its impressed by continuing RPO growth.

Oracle hosts its conference call at 5:00 p.m. ET, and commentary could change the after-hours negativity.

Oracle shares are trading down between 5% and 6% currently.

It should be noted that the company’s big EPS beat was aided by a $2.7 billion gain from divesting a stake in Ampere.

One positive note : The company attributed RPO growth to ‘Meta, NVIDIA, and others.’

The market is clearly spooked by Oracle’s reliance on OpenAI, so they’re trying to shift the story to a more diversified customer base.

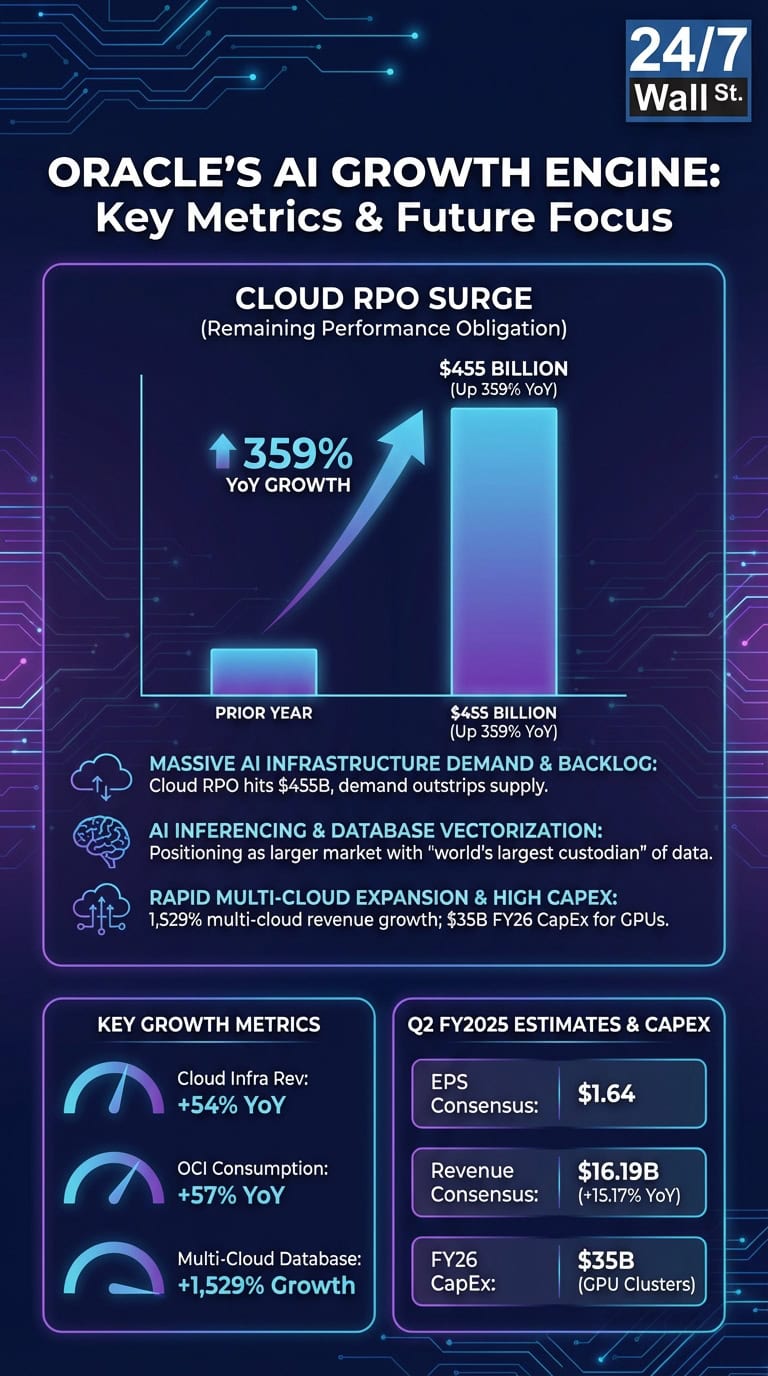

Last quarter Oracle shocked the world with $455 billion in RPO. This quarter that number surged up to $523 billion, well beyond any other hyperscale cloud companies.

And yet, shares remain down as the company slightly missed on revenue last quarter.

Shares are down 5% as of 4:09 p.m. ET.

Revenue slightly missed ($16.06 billion) versus expectations of $16.19 billion.

Adjusted EPS of $2.26 significantly outpaced Wall Street’s expectations of $1.64.

Shares are initially down 5%. We’ll continue posting updates.

We expect Oracle earnings to release at about 4:05 p.m. ET.

Before the earnings release, make sure to subscribe to 24/7 Wall St.’s AI Investor Podcast if you’re an investor in this fast-moving space.

We just released our latest episode detailing 24/7 Wall St. Analyst Eric Bleeker’s trip down to Abilene, Texas to see Oracle’s first Stargate project.

You can listen to an embed in Apple Podcasts below as well:

Oracle (Nasdaq: ORCL) is set to report after the bell. We’ll be updating this live blog with news and analysis the moment their earnings go live.

One note before the company reports, prediction market Polymarket is currently assigning a 90% probability that Oracle will ‘beat’ today’s earnings.

As a reminder, Wall Street consensus for the current quarter stand at:

- EPS: $1.64

- Revenue: $16.19B

- YoY Sales Growth: 15.17%

Looking ahead to the future, Wall Street also expects:

Next Quarter (Feb 2026) Consensus

- EPS: $1.72

- Revenue: $16.86B

FY2026 Consensus

- EPS: $6.82

- Revenue: $66.98B

FY2027 Consensus

- EPS: $8.00

- Revenue: $83.57B

As we noted earlier, we expect most of the reaction after-hours to be less focused on what Oracle reported last quarter and whether management can calm fears around the risk the company is taking on with its massive OpenAI partnership.

Oralce last reported earnings on September 9th. The company closed the day trading for $241.51.

By the end of the next day, shares had skyrocketed to $328.33, about a 36% gain.

Oracle announced a massive swelling of its RPO – or future backlog – thanks to an expanding partnership with OpenAI. Investors initialy cheered the news.

Yet, Oracle has dropped steadily throughout its most recent quarter and now trades below the level it was trading at when it announced massively increased guidance last quarter.

The reason is simple: Wall Street fears two things.

1.) That Oracle won’t have the financing available for this massive buildout. During the quarter, investors fretted that the value of Oracle’s credit default swaps was rising. That is to say, traders are pricing in a higher probability of Oracle defaulting on its future debts.

2.) Fears have risen that OpenAI will be unable to pay for the massive building boom it’s announced. The company has announced more than $1 trillion in spending programs all predicated on massive growth in the years ahead.

With OpenAI facing increased competition from rival models like Google’s Gemini 3, there’s additional doubt OpenAI will be able to pay for all the partnerships its announced.

We doubt there will be a dramatic reaction to whether Oracle tops Wall Street’s expectations for last quarter. Rather, Wall Street will likely react to what Oracle says to calm fears that the company is taking on too much risk in building this level of infrastructure for OpenAI.

Eric Bleeker has been investing for more than 20 years. He began his career working at Microsoft before joining Motley Fool, one of the largest publishers of financial research. In his 15 years at Motley Fool Eric served as the General Manager for Fool.com and led coverage in the Technology & Telecom sector. In addition, he was a featured columnist and has hosted dozens of investing seminars attended by more than a million total investors. Eric has more than 1,000 financial bylines to his name and has been featured in The Wall Street Journal, CNBC, Fox Business, and many other leading publications. He is currently focused on artificial intelligence investing and is a CFA Charterholoder.