If you really want to achieve wealth, taking a page out of personal finance guru Dave Ramsey’s playbook isn’t the worst idea. Ramsey often offers advice that runs the gamut, from addressing your spending to examining your lifestyle. But if you follow his suggestions and use these five key tools, they can — in time — help you reach your financial goals.

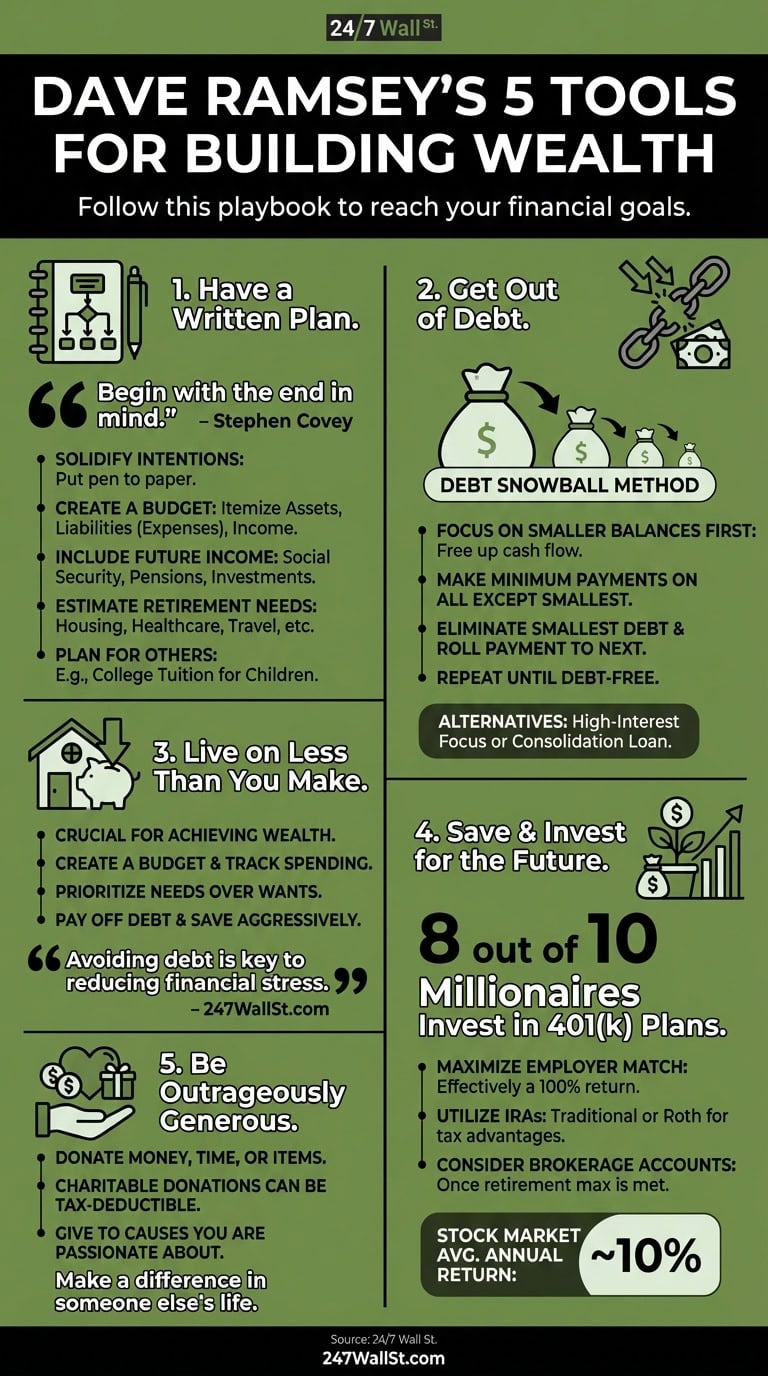

No. 1: Have a written plan.

Ideation is great. But there’s something about putting pen to paper that helps mentally solidify your intentions. And when it comes to growing financially, having a budget is critically important. That includes itemizing your assets, liabilities (e.g., expenses) and income. That income should include your present pay from working, but investments and retirement accounts should be prioritized over a reliance on future Social Security benefits, which Ramsey advises treating as an unpredictable bonus rather than a baseline strategy.

As you near retirement, “begin with the end in mind,” as noted by Stephen Covey, author of The 7 Habits of Highly Effective People. That includes an estimate of how much you’ll need to spend every year on housing, health care, food, travel and other expenses like transportation and even pet expenses.

Maybe you have plans to help your children, and even their children, with things such as college tuition. If so, write it down and work towards it.

No. 2: Get out of debt.

For many of us, getting out of debt is easier said than done. According to Ramsey, by focusing on the smaller balances first, you free up even more cash for the heavier debt loads. Once the smaller debts are repaid, you’ll have new cash flow to make extra payments on higher-interest balances.

Then, as noted by Ramsey Solutions, “Make minimum payments on all debts except the smallest — throwing as much money as you can at that one. Once that debt is gone, take its payment and apply it to the next smallest debt (while continuing to make minimum payments on your other debts).”

Then, repeat that over and over again until you drive down your overall debt.

Or, you could make just minimum payments on all of your debt and put a chunk into the principal of the debt incurring the highest interest. Another approach: You could take out a consolidation loan, wipe out all of the outstanding debt and have one balance in total. Not only could this allow you to manage your debt a bit better, but it may also allow you to put extra funds into an emergency account.

No. 3: Live on less than you make.

Ramsey believes living on less than you make is crucial for achieving wealth. To do so, create a budget, track your spending, put needs before wants, pay off debt and save. Living on less can help with debt reduction and help you take financial control. In the modern economic landscape, this strategy requires deliberate navigation of sticky inflation by deploying digital budgeting applications to actively audit impulse online purchases and one-click transactions.

Additionally, “Ramsey emphasizes the importance of avoiding debt, particularly from credit cards, which can lead to a cycle of overspending and financial strain. Instead, prioritize budgeting and saving so you can develop a more positive relationship with money, viewing it as a tool for achieving goals rather than a source of stress,” says 247WallSt.com contributor Chris MacDonald.

No. 4: Save and invest.

If you’re eligible for a 401(k) plan, take advantage of employer match plans (which is essentially like receiving an automatic 100% return on your contributions up to the matching limit). This year, a record number of Americans became so-called 401(k) millionaires because of the benefits these plans offer. According to Ramsey Solutions, eight out of 10 millionaires invested in their company’s 401(k) plan. To maximize this approach, the standard order of operations dictates investing in a workplace 401(k) precisely up to the company match, completely maxing out a Roth IRA next, and then returning to the 401(k) to capture overflow contributions if the 15% retirement threshold has not yet been achieved.

If you don’t have access to a 401(k) or if you do but still want to save more, consider an individual retirement account (IRA) allows you to save for retirement with tax-free or tax-deferred growth. While it’s best to check with your financial advisor, many times you can deduct contributions on your tax return. Roth IRAs, for example, allow you to invest post-tax dollars so that — at retirement age and beyond — you won’t be taxed on any of the gains or dividend distributions when you tap into those funds.

If you’re able to meet the maximum annual contribution for your IRA, which currently stands at $7,500 for those under age 50 or $8,600 for those age 50 and older, you can allocate remaining funds toward workplace 401(k) options which feature a baseline employee contribution ceiling of $24,500. Beyond these tax-advantaged accounts, a traditional brokerage account can be utilized to build wealth through the stock market, which historically delivers an average annual return of 10%.

No. 5: Be outrageously generous.

If not with your money, then with your time or with donations of food or clothes, suggests Ramsey. As noted by Ramsey Solutions, “Ramsey says that charitable donations can be tax-deductible, which can help lower your tax bill. He also says that giving to a charity you’re passionate about can be fun and that you can make a difference in someone else’s life.”

Editor’s Note: This article has been revised to reflect current IRS regulatory parameters, updating the standard IRA contribution baseline to $7,500, the catch-up allocation to $8,600, and incorporating the $24,500 employee 401(k) ceiling. Textual additions have been integrated to outline modern structural strategies regarding digital spending tracking during persistent inflationary periods, specific asset allocation sequencing between workplace matching programs and Roth vehicles, and current perspectives on long-term dependence on federal entitlement programs.

Contact [email protected] for any questions or corrections.