Large-cap multifactor ETFs combine value, quality, momentum, and size signals into a single portfolio. For retirees weighing whether to add John Hancock Multifactor Large Cap ETF (NYSEARCA:JHML) to their income strategy, the question is whether this fund delivers the stability and income retirement portfolios need.

What Multifactor Exposure Actually Means for Retirees

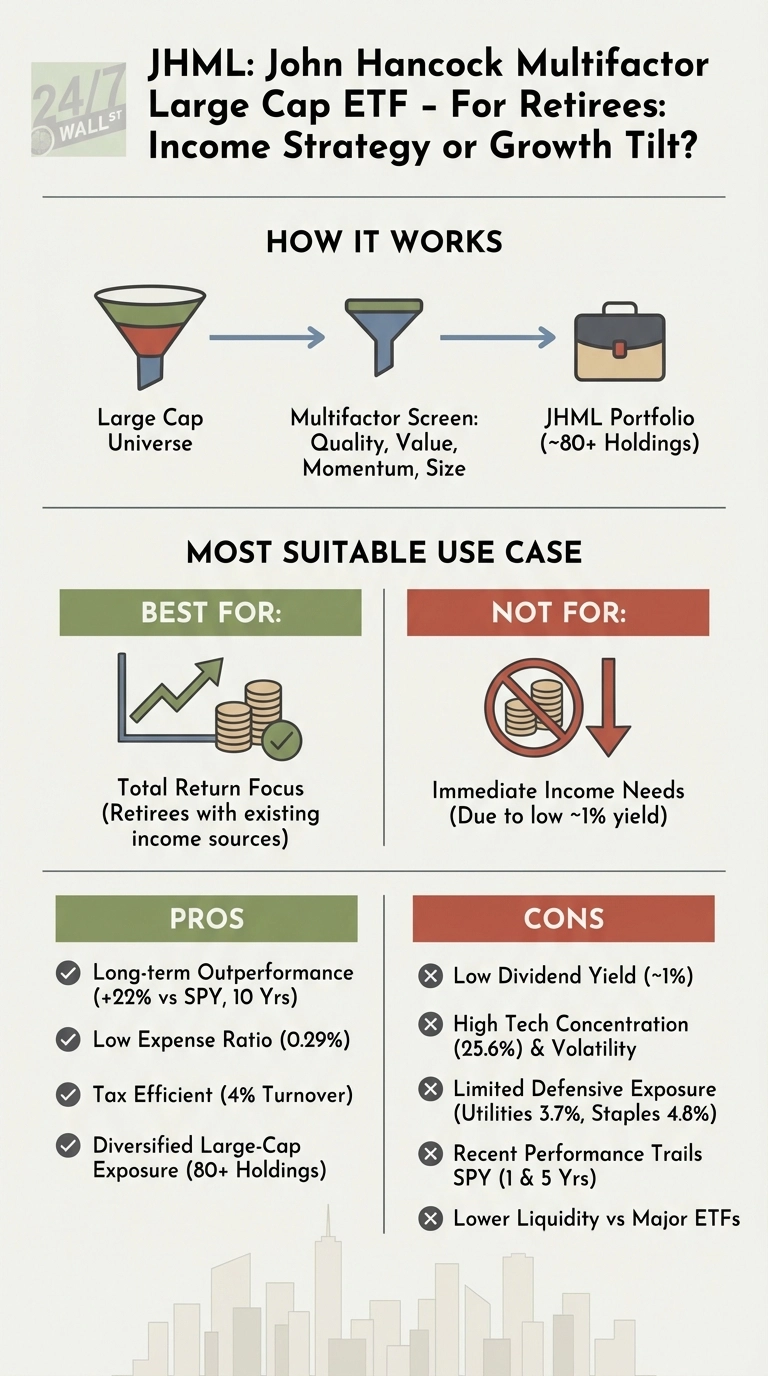

JHML screens the large-cap universe using quality, value, momentum, and size signals to build a portfolio of roughly 600 companies. This multifactor approach costs 0.29% annually—three times the expense of basic index funds—which raises the bar for outperformance. Recent results show the strategy trailing the S&P 500, suggesting the multifactor premium hasn’t materialized consistently for investors.

The Income Problem Retirees Can’t Ignore

The fund’s dividend profile reveals a modest income story. For retirees building portfolios to generate living expenses, the limited yield requires selling shares to meet typical withdrawal strategies.

The portfolio’s sector mix explains the income challenge. Information technology dominates at 26% of assets, with mega-cap growth names like Nvidia (NASDAQ:NVDA | NVDA Price Prediction), Apple (NASDAQ:AAPL), and Microsoft (NASDAQ:MSFT) accounting for nearly 12% combined. This growth orientation drives price appreciation but produces minimal dividends. Traditional income sectors like consumer staples and utilities receive only token allocations, leaving the fund poorly positioned to generate meaningful yield for retirees seeking cash flow.

The fund’s 4% annual turnover rate delivers tax efficiency that typically benefits retirement accounts. But this advantage diminishes when the modest yield forces retirees to regularly sell appreciated shares to meet cash flow needs, potentially triggering the very capital gains taxes the low turnover was designed to avoid.

Trading Stability for Growth Tilt

JHML behaves more like a total return vehicle than an income generator. The heavy technology weighting means volatility comparable to broad market indexes, including a 6.6% drawdown in late 2025. While the multifactor approach may reduce some volatility over full market cycles, it doesn’t eliminate sequence-of-returns risk that threatens retirement portfolios during downturns.

The expense ratio matters more as portfolio size grows. A retiree holding $500,000 in JHML pays roughly $1,000 more per year compared to low-cost index alternatives, creating a performance hurdle that compounds over retirement timelines.

Liquidity presents another concern. With daily volume often below 100,000 shares, retirees managing larger positions may face wider bid-ask spreads when rebalancing or taking distributions.

Who Should Skip This ETF

Retirees who need current income should look elsewhere. The modest yield doesn’t support withdrawal rates in the 3% to 4% range without depleting principal through share sales. Conservative investors uncomfortable with technology concentration should also avoid JHML. The fund’s tilt toward mega-cap tech stocks introduces volatility that conflicts with capital preservation goals common in retirement portfolios.

Consider Dividend Growth Instead

WisdomTree U.S. Quality Dividend Growth Fund (NASDAQ:DGRW) offers a more retirement-appropriate alternative for investors who want both factor exposure and meaningful income, with explicit focus on dividend growth and companies demonstrating earnings quality and consistent payout increases.

DGRW’s holdings selection prioritizes dividend sustainability and growth. That focus becomes increasingly valuable as retirees need income that keeps pace with inflation. DGRW’s 0.28% expense ratio essentially matches JHML’s cost.

JHML works best as a total return holding for retirees who have income covered elsewhere, but the modest yield and tech concentration make it a poor fit for income-focused retirement strategies.

Contact [email protected] for any questions or corrections.