At 58 with $3 million saved, working one additional year ranks among the most financially consequential retirement planning decisions a person can make. For many near-retirees, “one more year syndrome” becomes a recurring trap, as one Reddit user described watching colleagues repeatedly delay retirement despite having sufficient resources. The math behind that single year reveals why this decision deserves serious consideration.

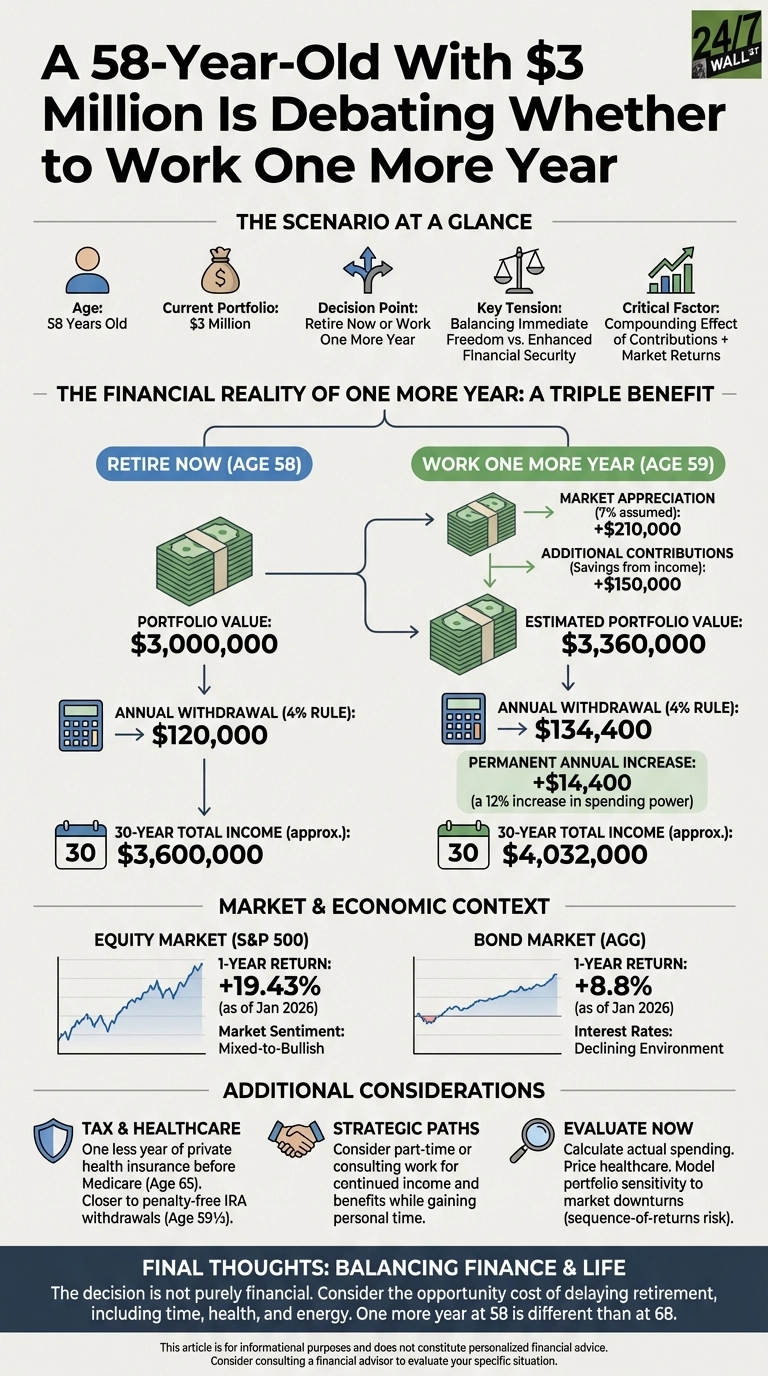

The Scenario at a Glance

- Age: 58 years old

- Current Portfolio: $3 million in retirement savings

- Decision Point: Retire now or work one more year

- Key Tension: Balancing immediate freedom against enhanced financial security

- Critical Factor: Compounding effect of contributions plus market returns

This scenario mirrors similar situations faced by professionals approaching 60 who wonder whether they have reached their financial finish line.

The Financial Reality of One More Year

A single additional working year delivers a triple benefit. First, you avoid withdrawing from your portfolio, preserving capital that would otherwise begin shrinking. Second, your existing $3 million keeps compounding. Assuming a conservative 7% annual return (well below the S&P 500’s trailing 12-month total return of approximately 22% as of early July 2026), that alone equates to $210,000 in market appreciation. Third, you are likely adding substantial new savings on top of that growth.

Maximizing retirement contributions at 58 means taking full advantage of 2026 IRS limits: a $24,500 base 401(k) deferral plus an $8,000 catch-up for savers age 50 and older, for a total of $32,500 in employee contributions. Combined with a 7% return on the existing portfolio, that single extra year could lift your nest egg to roughly $3.36 million. Applying the 4% safe withdrawal rate, your sustainable annual income climbs from $120,000 to $134,400, a 12% permanent increase in spending power that compounds across decades of retirement. One important 2026 wrinkle: under SECURE 2.0, savers whose prior-year FICA wages exceeded $150,000 must now make all age-based 401(k) catch-up contributions as Roth contributions, shifting the tax timing but not the contribution opportunity itself.

Tax and healthcare considerations add further weight to the calculation. Working another year means one fewer year of private insurance premiums before Medicare eligibility at 65. That matters more in 2026 than in any recent year: the enhanced ACA premium tax credits that held marketplace costs in check expired on January 1, 2026, after Congress could not reach an agreement to extend them. The impact has been immediate and severe. According to KFF research, the average subsidized marketplace enrollee is now paying 114% more in annual premiums than in 2025. For a 58-year-old without employer coverage, quality individual market plans can realistically run $15,000 to $25,000 per year at current rates, and a couple in their early 60s earning around $85,000 annually could face roughly $22,600 per year for benchmark silver-plan coverage. Delaying retirement by a year also edges you closer to penalty-free IRA withdrawals at age 59.5, reducing the friction of early portfolio access if it becomes necessary.

Advanced Structural Paths for the Early Bridge

Standard retirement guidance treats age 59.5 as the threshold for penalty-free distributions, but younger corporate professionals have additional tools available. The IRS Rule of 55 lets employees who separate from their employer during or after the calendar year they turn 55 take penalty-free distributions from that employer’s 401(k). Separately, Section 72(t) of the tax code permits Substantially Equal Periodic Payments (SEPP) from a traditional IRA, providing early access to capital without the standard 10% penalty, provided the payment schedule is maintained for five years or until age 59.5, whichever comes later. Each path carries real constraints, so modeling them with a tax professional before any retirement date is essential.

Mitigating Front-End Sequence Risk with a Cash Buffer

Working one extra year does more than grow your portfolio balance. It creates a practical window to guard against sequence-of-returns risk: the threat that a sharp early market decline forces asset sales while prices are depressed, permanently impairing long-term compounding. By directing final-year earnings and maximum catch-up contributions into short-duration fixed income or cash equivalents, a near-retiree can build a liquid runway covering the first two to three years of expenses. That cushion means an equity market correction in year one or two does not require selling broad index funds at a loss. Markets tend to recover; a retiree who avoids forced selling during a downturn preserves the compounding engine that funds the rest of retirement.

Strategic Paths Worth Considering

If your job is tolerable and your health is solid, working one more year delivers measurable, lasting security. The extra $14,400 in annual withdrawal capacity, sustained over 30 years, represents more than $430,000 in additional lifetime spending power before any portfolio growth is considered.

When burnout or health concerns dominate, the calculus shifts. A $3 million portfolio already supports a comfortable retirement with proper asset allocation. Splitting holdings between equity exposure through broad market index funds and investment-grade fixed income can sustain withdrawals while managing volatility. For context, iShares Core U.S. Aggregate Bond ETF (NYSEARCA:AGG) carries a 30-day SEC yield of approximately 4.2%, providing a reliable income stream alongside equity holdings.

A middle path is also worth exploring. Negotiating part-time work or consulting arrangements can preserve income and benefits while returning a substantial portion of personal time, enabling a phased transition rather than a hard stop.

What to Evaluate Now

Start by tracking 12 months of actual spending to establish a real baseline rather than a budget estimate. Price healthcare coverage in your state through ACA marketplaces to quantify what will likely be the single largest retirement expense before Medicare kicks in, keeping in mind that the expiration of enhanced premium tax credits has sharply raised 2026 marketplace costs. Then stress-test your portfolio against a significant market drawdown in the first few years of retirement. Retiring into a sustained decline creates sequence-of-returns risk that one more year of employment would largely sidestep by allowing both additional savings and the construction of a near-term cash buffer.

The most common mistake near-retirees make is treating this as a purely financial question, when it is equally one of life satisfaction and physical capacity. One more year at 58 involves a fundamentally different trade-off than the same decision at 68. The opportunity cost of delay includes time, health, and energy — assets no spreadsheet fully captures.

This article is for informational purposes and does not constitute personalized financial advice. Consider consulting a financial advisor to evaluate your specific situation.

Editor’s note: This update refreshes the S&P 500 trailing 12-month return to approximately 22% as of early July 2026, adds specific 2026 IRS 401(k) contribution figures ($24,500 base plus $8,000 catch-up for age 50-plus, totaling $32,500), and incorporates KFF data showing ACA marketplace enrollees are paying 114% more in premiums following the expiration of enhanced premium tax credits on January 1, 2026, with a couple in their early 60s earning around $85,000 potentially facing $22,600 per year for benchmark coverage.

Contact [email protected] for any questions or corrections.