Notions of “Fairness”

While the concept of fairness in the US is usually the equal application of a charge on anyone regardless of race or religion, income tax sharply divides Republicans and Democrats.

For most financial charges, Americans broadly agree on what fairness looks like: equal application regardless of race, creed, or background. A movie ticket is the classic illustration. Adults, children under 12, and senior citizens over 65 each pay the same price, with no variation for ethnicity or religion. Sales tax operates on the same principle. Whether the purchase is large or small, the same rate applies to everyone at the register.

Income tax is a different matter entirely, and it divides Americans sharply along political lines. Those on the Right argue that taxes are already too high and that people who take financial risks should not be penalized when those risks pay off. Those on the Left contend that great wealth is built on systemic advantages, and that the wealthy should contribute more to the public good by paying their “fair share.” Neither side is entirely wrong, which is precisely what makes the debate so durable.

A tax that escalates with earnings is technically labeled “progressive,” while one applied at the same rate across all income levels is called a “flat” or, pejoratively, a “regressive” tax. In practice, however, those at the very highest wealth tiers often pay a lower effective rate on their total income than those in the upper middle class, thanks to a web of deductions and preferential rates on investment income.

Consumption Taxes vs. Wealth Taxes: The “Fairness” Alternatives

The persistence of this debate has pushed structural alternatives to the forefront of fiscal policy. Proponents of a national consumption tax, often referred to as the FairTax, argue for taxing what people spend rather than what they earn. Supporters say this approach better rewards productivity and saving. To prevent the burden from falling hardest on lower-income households, such proposals rely on a system of “prebates” that offset costs on essential goods. The traditional European model works differently, pairing high Value-Added Taxes (VAT) with progressive income brackets to fund broad social safety nets. Both approaches rest on competing visions of what fairness actually requires.

History of Income Tax

Although the Republican platform advocates reducing taxes and shrinking the Federal government while Democrats want more taxation and more Federal government power, Abraham Lincoln, the first Republican president, was also the first to enact an income tax in 1861 to help fund the Union Army during The Civil War.

The American economic system has historically succeeded in large part because its foundations rest on private property rights and the principle of equal opportunity. Anyone, in theory, can pursue the American dream through their own efforts. That cultural premise has always shaped the public debate over how much government should claim from the fruits of that effort.

Despite being the nation’s first Republican president, Abraham Lincoln created the first federal income tax in 1861 to fund the Union side of the Civil War. It began as a flat levy of 3% on incomes over $800. As the war dragged on, Congress amended it in 1862 to a graduated structure: 3% on incomes between $600 and $10,000, and 5% on everything above. Public pressure led to the tax’s repeal in 1872.

Income tax returned in 1913 under President Woodrow Wilson, following ratification of the 16th Amendment. The most consequential structural shift, however, came in 1943, when Congress passed the Current Tax Payment Act to help finance World War II. Before that law, Americans paid their income taxes in quarterly installments the following year. The 1943 act required employers to withhold taxes directly from paychecks and remit them to the government, converting tax collection from an annual reckoning into a nearly invisible payroll deduction. That change fundamentally altered how Americans perceive their take-home pay, and federal spending has expanded continuously in the decades since.

At the Root of Federal Income Tax Inequality: Progressive Income Tax

The Progressive Income Tax system is the major reason for the discrepancy between why some citizens might pay in the mid 4-figures in tax, while other might pay many times more.

The progressive income tax has come a long way from Lincoln’s two-tier structure. Today, the federal system has seven brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Because the rates are marginal, each tier applies only to the slice of income that falls within it. A taxpayer earning $50,000 pays roughly 10% on the first $12,000, 12% on the next $36,000, and 22% on the remaining $2,000. The result is an effective tax burden that rises as earnings climb, concentrating the load on those theoretically most able to bear it. In practice, the reality is considerably more complicated.

Why The Rich Treat Good Accountants Like Rock Stars

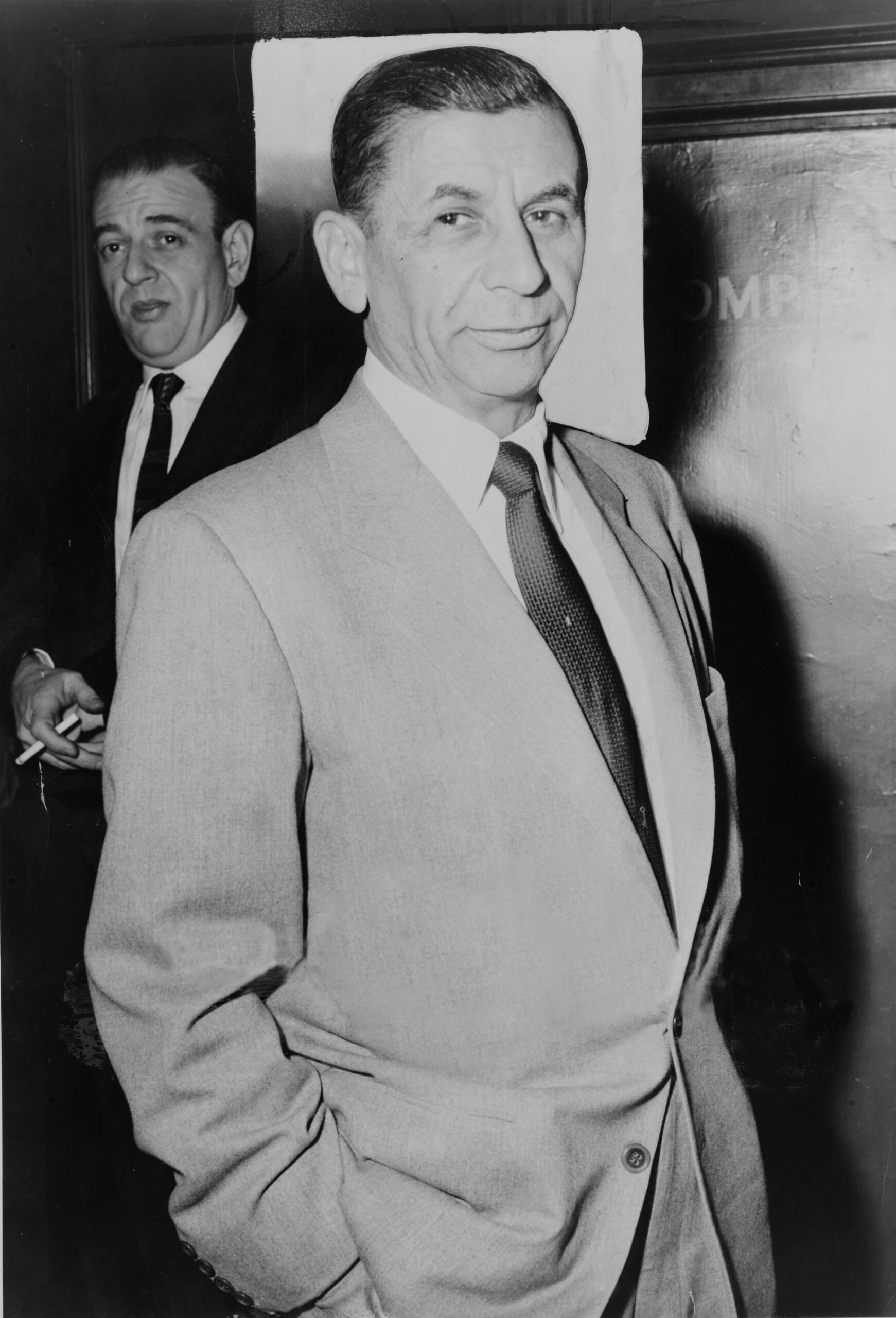

The ultrarich highly value skilled accountants who know how to navigate the voluminous US tax code – even organized crime revered Meyer Lansky for his acumen in laundering and legitimizing the illegal money of mobsters like Bugsy Siegel and Lucky Luciano.

As the tax code grew more complex over decades, politicians layered in provisions that benefit well-connected donors and, often, themselves. Only those who can afford skilled professional accountants have a realistic shot at using them. According to the National Taxpayers Union Foundation, the Internal Revenue Code alone measured approximately 4.1 million words in 2023, and when IRS regulations are factored in, the document runs to nearly 17,500 pages. No individual taxpayer can realistically navigate that volume without professional help.

Deductions, exemptions, specialty credits, and a range of other provisions at both the federal and state levels can reduce taxable income dramatically, even for those earning seven figures or more. Capital gains and passive income face lower rates than ordinary wages. High-net-worth individuals frequently use the “borrow-and-die” strategy, taking low-interest loans against their equity portfolios to fund their lifestyles and sidestepping taxable capital gains events entirely. The accountants who master these techniques are worth every dollar they charge.

The numbers that result from all of this are striking. According to IRS data for tax year 2023, the top 50% of earners (those reporting adjusted gross income above $53,801) paid 97% of all federal individual income taxes. The top 5% paid 59.3% of the total. The top 1%, a group that begins at $675,602 in AGI, paid 38.4% of all federal income taxes while earning 20.6% of the nation’s total income. Their average effective rate was 26.3%, roughly seven times the 3.7% average rate paid by the bottom half. Those below $53,801 in income paid 3.3% of the national total combined. Worth noting: these figures cover individual income taxes only. When payroll taxes are added to the ledger, the top 1%’s share of all federal taxes falls considerably, because Social Security and Medicare taxes hit wage earners at every income level.

Even organized crime has long recognized the value of skilled financial minds. For centuries, Chinese Triads placed the highest non-leadership honor, the White Paper Fan (415) rank, on their designated business advisors and accountants, who managed proceeds from criminal enterprises. In American organized crime, Meyer Lansky was the central figure in legitimizing the gambling and bootlegging proceeds of Bugsy Siegel, Lucky Luciano, and others. For all of Al Capone’s violent crimes, it was ultimately tax evasion that gave federal prosecutors the grounds to arrest and convict him.

The mathematical inequality in who pays federal income taxes is not seriously disputed. What remains bitterly contested is whether that inequality is “fair.” The landscape shifted significantly on July 4, 2025, when President Trump signed the One Big Beautiful Bill Act into law. The legislation permanently extended the individual income tax rates established by the 2017 Tax Cuts and Jobs Act, which had been scheduled to expire at the end of that year, and also made the nearly doubled standard deduction permanent. It added temporary deductions for tip income and overtime pay, running through 2028, along with a temporary $6,000 annual deduction for taxpayers aged 65 and older through the same year. The question of eliminating the federal income tax entirely, which both Trump and Treasury Secretary Bessent had floated, remains off the table for now. Individual income taxes have historically accounted for roughly half of all federal revenues, and whether rising tariff collections could ever offset that gap remains an open and contested question as the broader debate over the structure and fairness of the tax code continues.

Editor’s note: This article was updated to reflect 2023 IRS data (the top 1% income threshold is $675,602, with a 38.4% share of federal income taxes and a 26.3% average effective rate), to note that the top 1%’s share of all federal taxes falls when payroll taxes are included alongside income taxes, to add specifics on the One Big Beautiful Bill Act’s tip and overtime deductions (temporary through 2028) and its permanent standard deduction extension, and to correct the tax code word count to approximately 4.1 million words for the IRC as of 2023 with IRS regulations spanning nearly 17,500 pages.

Contact [email protected] for any questions or corrections.