Social Security is not going bankrupt, but it is heading toward a funding crisis that could reduce monthly checks by roughly a fifth within the next decade. Understanding what that means for your retirement income matters more than ever, especially if you are within 10 years of claiming benefits.

What’s Actually Happening

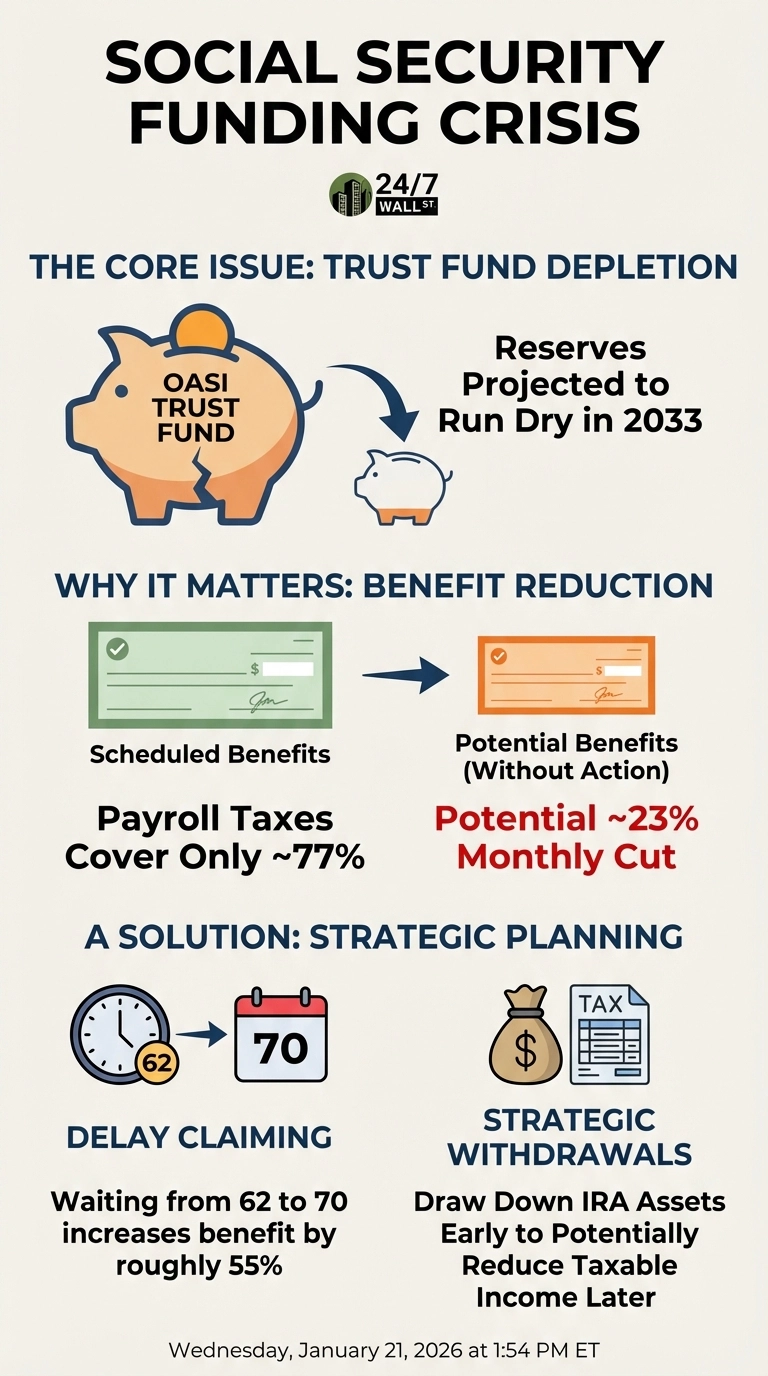

The Old-Age and Survivors Insurance Trust Fund now faces a critical milestone in late 2032, when its reserves are projected to run dry. That deadline moved up by roughly three months from the prior projection, reflecting two pieces of recent legislation that together worsened the program’s finances. The 2026 Trustees Report, released in June 2026, confirmed the accelerated timetable.

The depletion itself does not mean Social Security disappears. Payroll taxes from current workers will continue flowing in, but those taxes alone cannot cover full benefits. The gap between incoming revenue and promised payments is what creates the crisis. The 2026 Trustees Report projects that after the OASI fund is exhausted, payroll tax collections will support only about 78% of scheduled retirement benefits, leaving an average retiree short by hundreds of dollars each month.

Two pieces of legislation accelerated the timeline. The Social Security Fairness Act, signed in January 2025, repealed two provisions that had reduced benefits for certain public-sector workers, adding roughly $200 billion to the program’s 10-year shortfall. Then the One Big Beautiful Bill Act, signed on July 4, 2025, made permanent lower income tax rates and expanded deductions that reduce the revenue Social Security receives from the taxation of benefits, adding another $168.6 billion in costs over the same decade. Together, these laws pushed the projected OASI depletion date forward from early 2033 to late 2032.

For someone receiving the current average monthly retirement benefit of about $2,081, a 22% reduction would trim roughly $458 off each monthly check. Couples face an even sharper squeeze as their combined household income shrinks by hundreds of dollars. Those losses force real tradeoffs between housing, medical bills, and everyday essentials that retirees depend on.

Why This Matters for Your Claiming Decision

The timing of when you start benefits carries lasting consequences, and the closer depletion date makes this decision more urgent. Claiming early locks in a permanently lower monthly amount, and that reduction compounds if Congress later implements cuts on top of it.

Many retirees weigh whether to claim early and secure guaranteed payments now, or delay for higher monthly checks that might face cuts later. There is no universal answer, but the math favors waiting if you have other savings to draw from in your early 60s. Even under the updated projections, delaying from 62 to 70 can increase your monthly benefit by roughly 55% before any statutory cuts are applied, because the Social Security Administration credits 8% per year for each year you wait past full retirement age.

How Other Income Changes the Equation

Social Security does not exist in isolation. It interacts with your other retirement income in ways that directly affect your tax bill. When your combined income crosses certain thresholds, up to 85% of your benefits become taxable. This creates a planning opportunity: drawing down IRA assets strategically before claiming Social Security can reduce your taxable income later, potentially keeping more of your benefits out of the tax net and preserving thousands of dollars over a 20-year retirement.

What to Think Through Now

Focus on what you can control. Review your savings and estimate how long they could sustain you if you delay claiming. Factor in your health and family longevity patterns, because Social Security provides income for life regardless of how long you live. The program’s 75-year actuarial deficit has widened to nearly 4% of taxable payroll, its largest gap since 1977, which underscores how serious the structural imbalance has become.

Any congressional fix will likely combine benefit adjustments, revenue increases, or changes to the retirement age. The goal for individuals is to build a claiming strategy that holds up across multiple scenarios, one that treats Social Security as a critical foundation even if it ultimately becomes a somewhat smaller one.

Editor’s note: This article has been updated to reflect the 2026 Social Security Trustees Report (released June 2026), which moved the projected OASI trust fund depletion date to late 2032 and revised the post-depletion benefit payable rate to approximately 78%. The article also incorporates the effects of the One Big Beautiful Bill Act and the Social Security Fairness Act, both of which worsened the program’s finances, and updates the average monthly retirement benefit to $2,081 based on current SSA data.

Contact [email protected] for any questions or corrections.