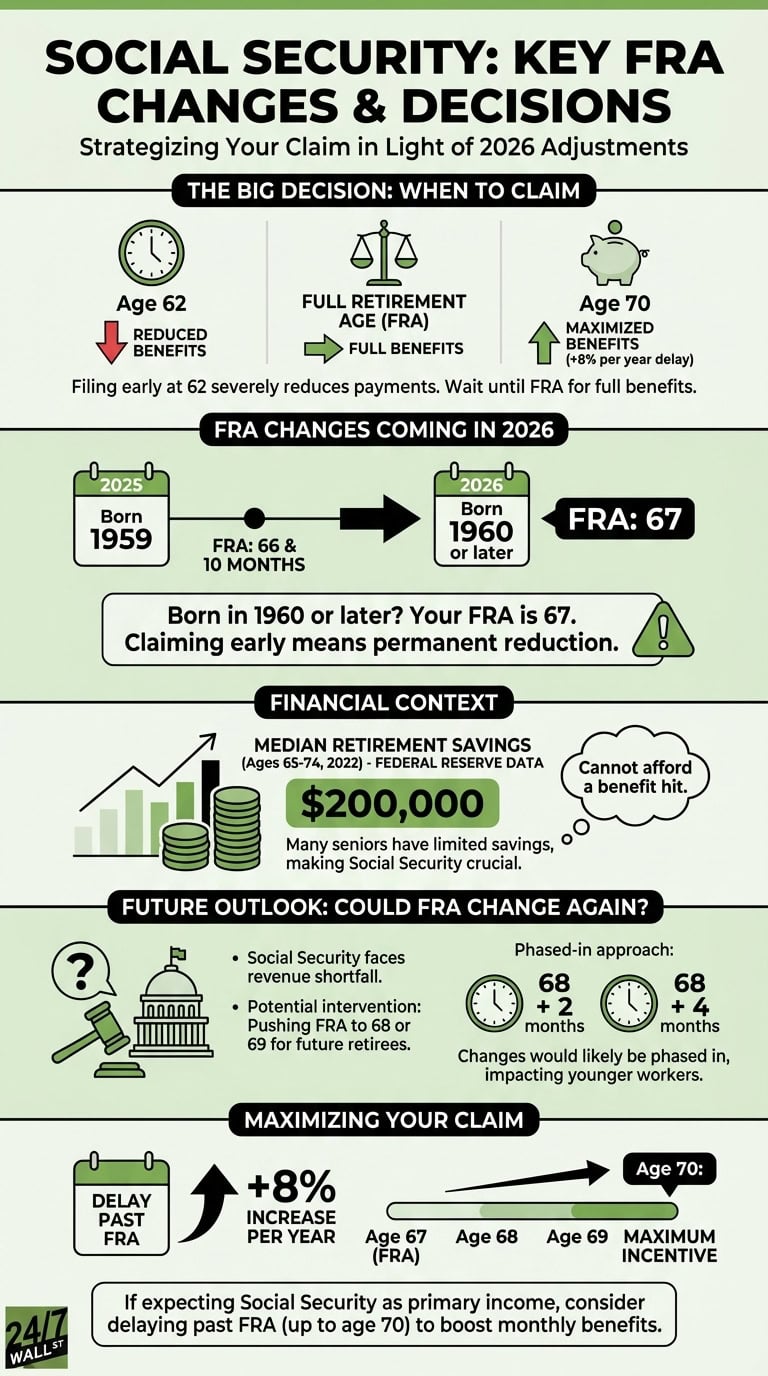

One of the biggest decisions retirees face is figuring out when to claim Social Security. You can sign up for benefits at any point after turning 62, but filing that early carries a steep price: for anyone whose full retirement age (FRA) is 67, claiming at 62 permanently cuts monthly benefits by 30%.

Waiting until FRA is the baseline for receiving your full, unreduced benefit. And in 2026, that milestone has officially shifted in a way that affects millions of Americans approaching retirement.

How FRA is changing in 2026

For decades, Social Security’s FRA stood at 65. That changed in 1983, when Congress passed legislation to gradually raise the FRA in response to longer life expectancies and growing funding pressures. The result was a phased schedule that slowly pushed FRA from 65 to a range of 66 to 67, adding two months per birth year starting with those born in 1955.

In 2026, that gradual phase-in reaches its endpoint. For anyone born in 1959 who reached their FRA in late 2025, the magic number was 66 and 10 months. But for those born in 1960 or later, FRA is now a full 67. That is the highest FRA the program has ever carried, and it applies to every worker born from 1960 onward. Claiming even a single month before that point triggers a permanent benefit reduction.

To put the stakes in dollar terms: in 2026, the maximum monthly Social Security benefit at FRA is $4,207 for workers with maximum taxable earnings across 35 working years. A 30% reduction from claiming at 62 would trim that to roughly $2,945. For most retirees earning far less than the maximum, the gap still represents thousands of dollars each year for the rest of their lives.

Those figures matter especially in light of how little many seniors have saved. According to the Federal Reserve’s 2022 Survey of Consumer Finances, the median retirement savings for households aged 65 to 74 is $200,000. That sounds substantial, but it translates to a modest income stream, making Social Security the financial anchor for a large share of retirees. A permanently reduced benefit can mean the difference between financial stability and a monthly shortfall.

Could Social Security’s FRA change again?

For anyone born in 1960 or later, age 67 is currently the finish line for full, unreduced benefits. Whether that line will move again is an open question, and the answer depends heavily on how Congress addresses Social Security’s funding crisis.

The 2026 Social Security Trustees Report, released in June 2026, projects that the Old-Age and Survivors Insurance (OASI) Trust Fund will be depleted in the fourth quarter of 2032. At that point, incoming payroll tax revenue would cover only 78% of scheduled benefits. If Congress were to allow borrowing between the OASI and Disability Insurance trust funds, the combined depletion date extends to the third quarter of 2034, with 83% of benefits payable. Either way, the clock is ticking. The program’s annual cost has exceeded its non-interest income every year since 2010, and total reserves declined by $160 billion in 2025 alone.

Reform proposals being discussed include increasing the payroll tax rate, adjusting benefit formulas for higher earners, changing the cost-of-living adjustment calculation, and raising the FRA beyond 67. Pushing FRA to 68 or 69 for workers born after a certain year would reduce long-term outlays without a direct benefit cut to existing retirees. Such a change would almost certainly be phased in gradually, adding two months per birth year much as the 1983 law did, so younger workers would bear the adjustment while those near retirement would be mostly unaffected.

None of these changes are imminent, but the 2025 Trustees Report put the long-range actuarial deficit at 3.82% of taxable payroll, the largest since 1977, underscoring that meaningful action is needed well before the trust fund runs dry.

What this means for your claiming decision

If you are approaching retirement, the most important step is knowing your exact FRA and building your plan around it. Claiming Social Security at your FRA locks in your full benefit. Waiting beyond FRA earns delayed retirement credits worth 8% for each additional year, up to age 70. Delaying from 67 to 70 boosts your monthly payment by up to 24% above your FRA benefit, a meaningful gain if you are in good health and expect a longer retirement.

That delayed-claiming incentive also works as a hedge against possible future cuts. A larger starting benefit gives you a higher base if Congress eventually reduces the program’s cost-of-living adjustments or restructures benefits for future retirees. And because the 2026 COLA was 2.8%, a higher starting benefit compounds more in nominal dollar terms each year.

For retirees with modest savings, the case for patience is particularly strong. Locking in a reduced benefit at 62 can leave you permanently dependent on a smaller check at precisely the age when healthcare and other costs tend to rise. When in doubt, running your numbers through the Social Security Administration’s online estimator at SSA.gov is a useful starting point before making a final decision.

Editor’s note: This article was updated to reflect the most current Social Security trust fund data from the 2026 Trustees Report, which projects OASI depletion in Q4 2032 (one year earlier than prior estimates) and combined OASDI depletion in Q3 2034. The specific 30% benefit reduction for claiming at 62, the $4,207 maximum monthly FRA benefit for 2026, the 2.8% 2026 COLA, and the total 24% delayed retirement credit gain from waiting to age 70 were also added.

Contact [email protected] for any questions or corrections.