Retiring at 62 with $1 million sounds comfortable, but the financial landscape has shifted dramatically over the past decade. Inflation, interest rate volatility, and healthcare costs before Medicare have all compounded into a far harder problem than most savers anticipate — one that a well-padded account balance alone cannot solve.

The Scenario at a Glance

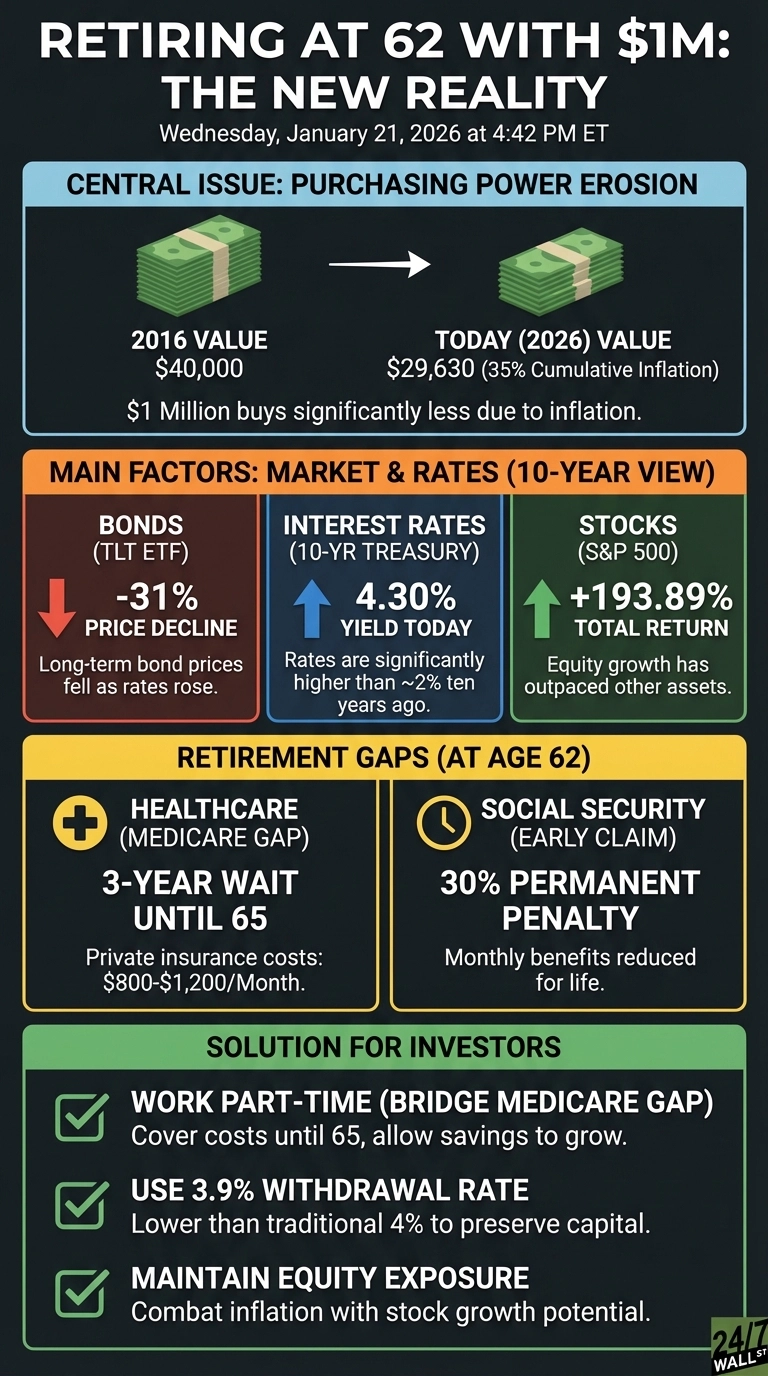

- Age: 62 (earliest Social Security claiming age)

- Portfolio: $1 million in retirement savings

- Gap years: 3 years until Medicare eligibility at 65

- Social Security penalty: 30% permanent reduction for claiming at 62 vs. full retirement age of 67

- Key concern: Making savings last 25 to 30 years amid rising costs

Online retirement planning communities frequently highlight a striking contrast: someone retiring at 42 with $1.26 million faces a very different calculus than someone doing so at 62 with the same portfolio. The 62-year-old must immediately bridge the gap to both Social Security and Medicare while spending down principal, leaving far less margin for error.

The Purchasing Power Problem

Bureau of Labor Statistics data show that $1 in 2016 now requires approximately $1.35 to buy the same goods in 2026, representing roughly 35% cumulative inflation over a decade. For a retiree following the traditional 4% withdrawal rule, a $40,000 annual withdrawal from $1 million today carries the purchasing power of just $29,630 in 2016 dollars. That erosion is not abstract. It shows up in grocery bills, utility costs, and especially healthcare premiums.

Morningstar’s 2026 State of Retirement Income report recommends a 3.9% starting withdrawal rate for retirees using a fixed spending strategy, translating to $39,000 annually from a $1 million portfolio. Retirees who adopt a flexible, market-responsive approach may be able to withdraw as much as 5.7% annually, though that strategy requires accepting some spending variability in down years.

The Interest Rate Reversal

Ten years ago, the 10-year Treasury yielded around 2%. As of mid-July 2026, the 10-year Treasury yield sits near 4.56%, driven by persistent inflation and ongoing fiscal deficit concerns. Higher yields benefit income-focused retirees who are building fresh fixed-income allocations. The rapid rate climb over the past four years, however, severely damaged existing bondholders who locked in at lower rates.

The iShares 20+ Year Treasury Bond ETF dropped significantly over the past decade as rates climbed, while the S&P 500 gained roughly 194% during the same period. That gap illustrates the permanent cost of retreating too far into bonds too early in a shifting rate environment — a lesson still being absorbed by retirees who repositioned aggressively in 2022.

The Sequence of Returns Danger Zone

Retiring at 62 creates acute vulnerability to early market downturns, a dynamic known as sequence of returns risk. Withdrawing fixed amounts from a portfolio during a bear market in the first few years of retirement locks in capital losses and can permanently impair the longevity of a $1 million nest egg. The practical antidote is a dedicated cash or short-duration buffer of one to two years of living expenses, held in Treasury bills or money market funds. That reserve reduces the need to sell equities at depressed prices during corrections, preserving more of the portfolio’s long-term growth engine.

What Actually Matters Now

At 62, a retiree is potentially funding three decades of spending with no Medicare coverage and reduced Social Security benefits. Healthcare is the most immediate financial pressure. The standard Medicare Part B premium is $202.90 monthly in 2026, but private insurance for a 62-year-old can run $800 to $1,200 monthly depending on location and health status. That translates to $9,600 to $14,400 annually before the annual Part B deductible of $283 or any additional out-of-pocket costs.

Claiming Social Security at 62 triggers a permanent 30% benefit reduction relative to the full retirement age of 67. The Social Security Administration sets the maximum monthly benefit at $2,969 for those claiming at 62 in 2026, compared to $4,207 at full retirement age. For someone entitled to $1,000 monthly at full retirement age, early claiming means accepting $700 instead, a shortfall that accumulates to roughly $90,000 in forgone benefits over 25 years.

Strategic Paths Forward

Working part-time until 65 eliminates the healthcare coverage gap and allows Social Security benefits to grow 8% annually for each year of delay past full retirement age, up through age 70. Even modest earnings of $20,000 to $30,000 yearly can substantially reduce portfolio withdrawals during the most critical early-retirement years, when sequence risk is highest and a single bad market run can cause lasting damage to portfolio longevity.

For those stopping work entirely at 62, managing tax brackets and withdrawal ordering becomes vital. Drawing from taxable brokerage accounts first, before tapping tax-deferred retirement accounts, can keep Modified Adjusted Gross Income low enough to qualify for Affordable Care Act premium subsidies before Medicare kicks in at 65. A few hundred dollars of monthly savings on premiums compounds meaningfully across a three-year Medicare gap.

Maintaining meaningful equity exposure is also important despite volatility concerns. A 60/40 stock-to-bond allocation historically supports longer retirement horizons better than conservative portfolios that struggle to outpace inflation. With the Bureau of Labor Statistics reporting 12-month CPI at 3.5% through June 2026, down from a 4.2% spike in May, the inflation trend is moving in the right direction — but remains above the long-run 2% average that most retirement models use as a baseline assumption.

The Options Income Alternative

For retirees whose required spending exceeds the $39,000 baseline from a 3.9% withdrawal rate, conservative options strategies can serve as a supplemental cash flow source. Writing out-of-the-money covered calls on core equity positions, or selling cash-secured puts on index funds, can generate an additional 2% to 4% in annual yield from an existing stock portfolio. This approach reduces the need to liquidate core holdings to meet living expenses, preserving more of the portfolio’s long-term growth capacity rather than steadily eroding it.

What to Do First

Start by calculating your true annual spending need, including healthcare. If it exceeds $39,000 to $40,000 from the portfolio alone, delaying retirement or building additional income sources deserves serious consideration. When running long-term projections, use at least 3% annual inflation as the planning baseline. The BLS June 2026 CPI reading of 3.5% is an improvement, but it still sits well above the historical 2% average, and Middle East energy dynamics keep the near-term outlook uncertain.

A portfolio that cannot grow above inflation at 62 will steadily lose purchasing power across a 30-year retirement. That makes sustained equity exposure a practical necessity, not a preference to be reconsidered every time markets turn volatile.

Editor’s note: This update corrects the 10-year Treasury yield to approximately 4.56% as of mid-July 2026 and refreshes the inflation figure to 3.5% for the 12 months through June 2026 (down from 4.2% in May), based on the Bureau of Labor Statistics release dated July 14, 2026. The Medicare Part B annual deductible of $283 for 2026 has also been added for context.

Contact [email protected] for any questions or corrections.