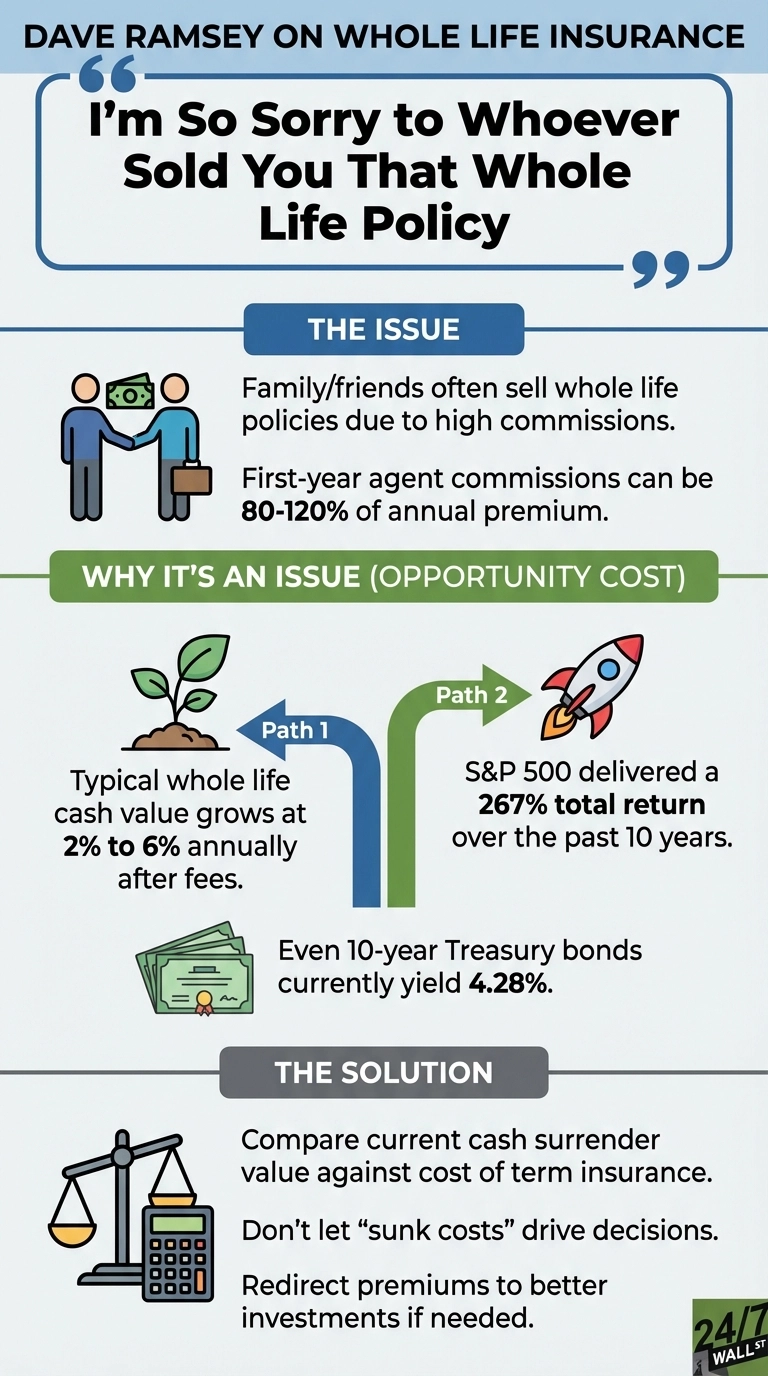

On a recent episode of The Dave Ramsey Show, caller Crystal revealed she had paid into a whole life insurance policy for 10 years after a family friend sold it to her. Ramsey’s response was direct, expressing regret about the sale. When he asked who sold it, Crystal confirmed it was a family friend. Ramsey noted the pattern of family members and friends selling these policies to their personal networks.

His commentary highlighted recruiting tactics common in the insurance industry, where newly licensed agents often target their personal connections.

Where Ramsey Gets It Right

The commission structure explains why newly licensed agents target their personal networks. First-year commissions on whole life policies typically range from 80% to 120% of the annual premium. This creates a powerful incentive to sell to people who trust you, even when the product doesn’t fit their needs.

The opportunity cost becomes staggering when you examine what Crystal gave up. While whole life cash value typically grows at 2% to 6% annually after fees, the S&P 500 delivered a 267% total return over the past 10 years. That difference represents the wealth Crystal sacrificed by choosing whole life over a simple index fund strategy.

Crystal didn’t need to take stock market risk to beat whole life returns. Even conservative investors choosing 10-year Treasury bonds at 4.28% would have built more wealth with zero market volatility, proving that whole life underperforms even the safest alternatives available to her.

The Missing Context

Ramsey’s criticism omits one legitimate use case: high-net-worth individuals facing estate tax liability. For households with estates exceeding the federal exemption threshold, permanent life insurance can provide tax-free death benefits to cover estate taxes. But Crystal’s situation doesn’t suggest this applies.

The advice also assumes Crystal still needs life insurance. If her dependents have aged out or her financial situation changed, she may not need any coverage at all.

What Crystal Should Do

If Crystal still needs death benefit protection, she should compare her current cash surrender value against the cost of term insurance for her remaining coverage needs. The emotional difficulty of walking away from 10 years of payments is real, but sunk costs shouldn’t drive future decisions. The question isn’t what she’s already paid, it’s whether continuing the policy serves her financial goals better than surrendering it and redirecting those premiums elsewhere.

Ramsey’s broader point stands: mixing family relationships with commission-based financial products rarely ends well for the buyer.

Contact [email protected] for any questions or corrections.