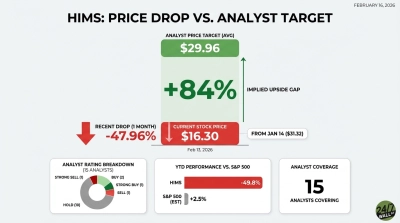

Hims & Hers Health (NYSE: HIMS) delivered a beat on both earnings and profitability in Q4 2025, though a soft 2026 revenue guidance is keeping the stock under pressure after a sharp year-to-date selloff.

The company posted EPS of $0.08, topping the $0.05 consensus estimate by 60%. Q4 revenue came in at $617.8 million, up 28.4% year-over-year and in line with analyst expectations. Adjusted EBITDA reached $66 million at an 11% margin, landing above the high end of the company’s own guidance range of $55 million to $65 million. For the full year, revenue totaled $2.35 billion, up 59% year-over-year.

The EPS beat snaps a streak of four consecutive quarterly misses and marks a clear profitability improvement from Q3’s $0.06 reported EPS. However, the GLP-1 regulatory overhang remains the defining risk: the FDA’s resolution of the semaglutide shortage has restricted Hims’s compounded weight-loss offerings, a key growth driver. Negotiations with Novo Nordisk over distributing branded Wegovy on the platform remain ongoing with no definitive agreement.

For 2026, management’s revenue and adjusted EBITDA guidance came in below analyst expectations, which may explain why the stock is down 78% year-to-date to $14.50 in Tuesday’s premarket despite the earnings beat. Retail sentiment on Reddit shifted sharply bullish post-earnings, with a r/wallstreetbets YOLO post accumulating 308 upvotes and 383 comments. Whether the Novo Nordisk partnership materializes and how the GLP-1 product transition affects subscriber growth through mid-2026 remain key variables for the company’s outlook.

Contact [email protected] for any questions or corrections.