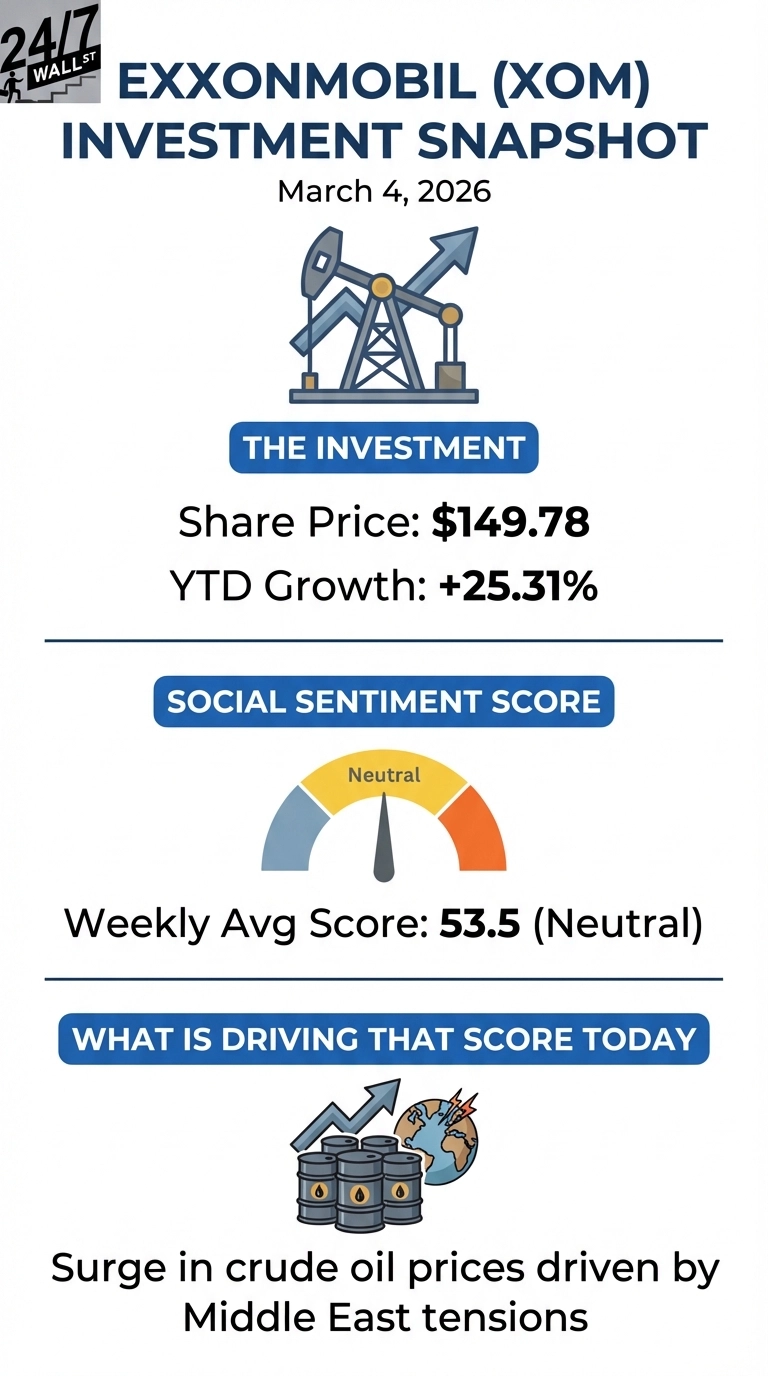

Amidst a growing international crisis heavily involving the price of oil, shares of ExxonMobil (NYSE:XOM) are trading at $149.78 as of Wednesday, up 24% year-to-date and 39% over the past year. Retail sentiment on Reddit has shifted from a monthly average score of 37.875 (bearish) to a weekly score of 53.5 (neutral) over the past week, tracking the surge in crude oil prices driven by Middle East tensions. WTI crude has climbed from $60.46 on January 26 to $71.13 as of March 2.

Polymarket traders are pricing an 80% probability of Iran closing the Strait of Hormuz by March 31, with the full-year market at 84% odds through December 2026. Citigroup raised its XOM price target from $118 to $150 on March 2, and the stock now trades above the current analyst consensus target of $144.25.

Reddit Is Asking the Right Question About XOM

The top-driving post this week, “Why are oil prices up but oil stocks down right now?” on r/stocks, has drawn 109 upvotes and 67 comments and reflects growing skepticism that the oil spike translates into durable equity gains.

Why are oil prices up but oil stocks down right now?

by u/[OP] in stocks

“Oil companies hedge their production and lock in prices months in advance, so a sudden spike doesn’t immediately flow through to earnings. The market is pricing in mean reversion before the next quarterly report even drops.” — u/[OP], r/stocks

Earlier in February, “The real bubble is in Big Oil, NOT in Big Tech” on r/stockmarket peaked at 150 upvotes and 69 comments with sentiment scores in the 22-31 range across nine consecutive data points. What retail discussion has missed entirely: ExxonMobil’s AI infrastructure investments, its supercomputer deployment with NVIDIA and Hewlett Packard Enterprise, or its Mobil Lithium initiative targeting EV battery supply chain entry by 2027.

The real bubble is in Big Oil, NOT in Big Tech

by u/[OP] in stockmarket

“Big Oil is trading on geopolitical fear premiums and legacy dividend chasers. The fundamentals don’t support these valuations when you strip out the noise — capex is ballooning and free cash flow is getting squeezed.” — u/[OP], r/stockmarket

Why retail sentiment stays cautious despite the price rally:

- Full-year 2025 net income fell 14.36% year-over-year to $28.84 billion, and Q4 revenue of $82.31 billion missed the $81.43 billion consensus estimate

- The Chemical Products segment posted a $281 million loss in Q4, weighed down by global capacity additions

- XOM’s trailing P/E of 23x sits above historical norms for an integrated major

The Operational Story Retail Investors Are Missing

ExxonMobil’s Q4 earnings told a different story. The company posted record production of 4.7 million oil-equivalent barrels per day, the highest annual output in over 40 years, while capturing $15.1 billion in cumulative structural cost savings since 2019. The Permian Basin hit a Q4 record of 1.8 million boed, and Guyana’s Yellowtail project started four months ahead of schedule. CEO Darren Woods has described the enterprise-wide AI and data platform transformation: “You will enable us to learn and act faster and better leverage our scale, accelerate the adoption of artificial intelligence, and integrate new solutions. It’s already delivering results, with much more to come.”

Chevron (NYSE:CVX) faces the same macro environment, having completed its Hess acquisition and deepened Guyana exposure. Both majors benefit from the same geopolitical tailwinds, but ExxonMobil’s annualized shareholder return of 29% over five years and 43 consecutive years of dividend growth give it a structural income argument pure-play E&P peers cannot match. The next concrete catalysts: Golden Pass LNG first cargoes expected very early March 2026, and a data center carbon capture announcement expected by year-end 2026.