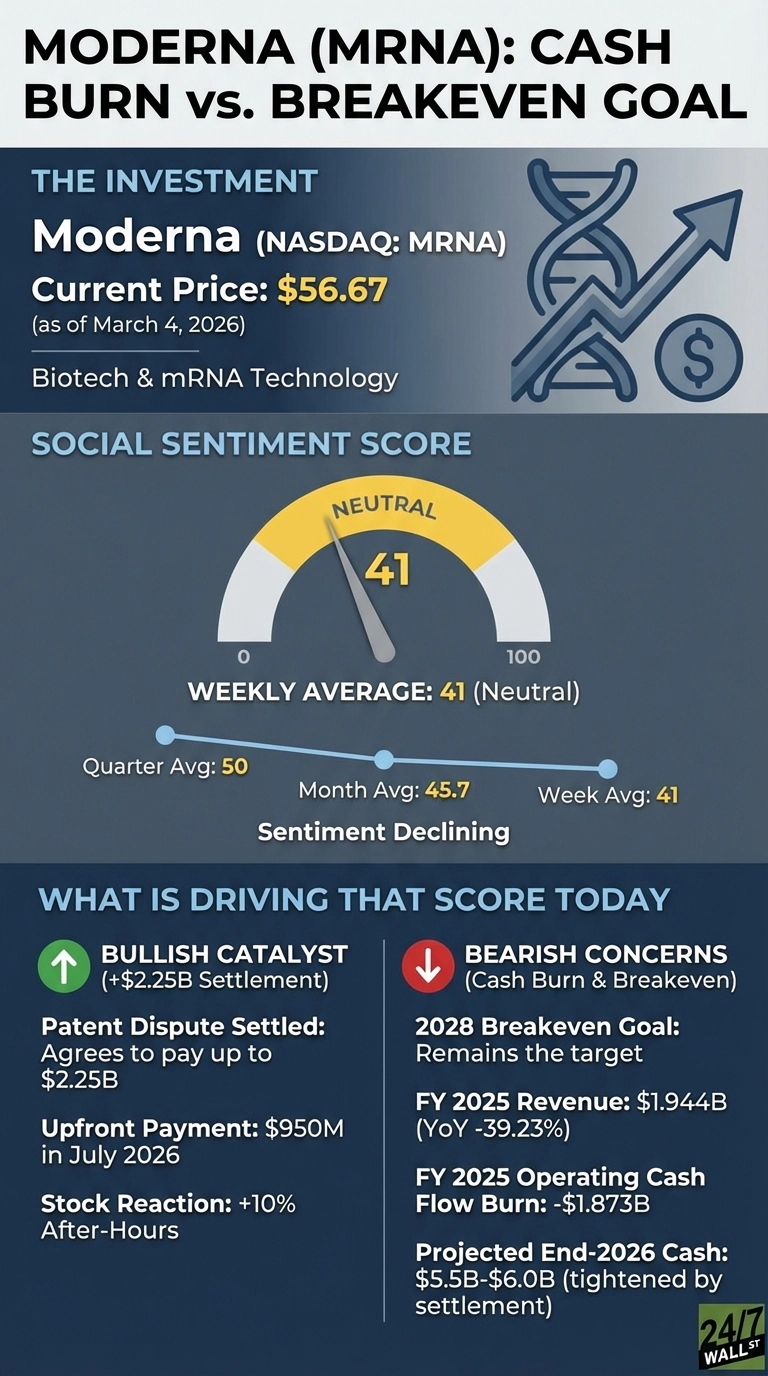

Investors who closely watch the healthcare sector are keeping an eye on Moderna (NASDAQ:MRNA) as its shares are up 12% over the past week and 95% year-to-date, trading near $56.67 as of March 4, 2026. Reddit sentiment has dropped from a quarterly average of 50 to a weekly reading of 41, even as catalyst-driven spikes pushed scores as high as 78 recently. Traders are cheering individual headlines, but anxiety about cash burn and the 2028 breakeven target hasn’t gone anywhere.

The Patent Settlement Tightens the Liquidity Picture

The catalyst lighting up r/wallstreetbets was Moderna’s agreement to pay up to $2.25 billion to settle a long-running legal fight over lipid nanoparticle technology used in its COVID-19 vaccine, including $950 million upfront by July 2026, with up to $1.3 billion more contingent on a Federal Circuit appeal. As a result of this settlement, shares jumped over 10% after-hours.

“Moderna +10% after-hours as Moderna agrees to pay up to $2.25B to settle COVID vaccine patent dispute”

Moderna +10% after-hours as Moderna agrees to pay up to $2.25B to settle COVID vaccine patent dispute

by u/[author] in wallstreetbets

Legal certainty has real value, but the settlement tightens the liquidity picture. Moderna projected ending 2026 with $4.5 billion to $5 billion in cash plus up to $900 million available under its credit facility after absorbing the upfront payment. The company was already guiding for $5.5 to $6 billion in year-end 2026 cash before the settlement, so the $950 million charge meaningfully narrows that cushion.

What the Bears Are Watching

Sentiment spikes tied to specific catalysts keep fading fast. Scores hit 78 on February 18 when the FDA agreed to review the revised flu vaccine application, then collapsed to the low 20s by late February. The r/options community is focused on structural concerns that no single settlement resolves:

- Full-year 2025 revenue fell 40% as COVID vaccine demand normalizes, with 2026 guidance assuming zero contribution from the flu vaccine.

- The oncology pipeline, particularly the personalized cancer vaccine with Merck, carries enormous potential, but Phase 3 adjuvant melanoma interim data is still expected sometime in 2026.

- Operating cash flow burned $1.873 billion in 2025, an improvement from prior-year levels but still substantial given a shrinking cash base.

“MRNA odd option activity observed prior to the crash.”

MRNA odd option activity observed prior to the crash.

by u/[author] in options

2028 Breakeven Depends on Execution

Fortunately, Moderna’s CFO acknowledged the uncertainty directly: “We have ten large shots on goal to increase revenue over the coming years, all with a wide range of potential outcomes.” The analyst consensus price target is $42.25, compared with a current price near $56.67, and 18 of 24 analysts rated it a hold. The patent settlement removes a ceiling, but the floor depends on whether the flu vaccine clears FDA review by August 5 and whether the melanoma Phase 3 interim delivers.