The death of Iranian Supreme Leader Ayatollah Ali Khamenei on February 28, 2026 has fundamentally altered the risk calculus across global energy markets. With the Strait of Hormuz, through which roughly 20% of global oil trade flows, now under acute threat, prediction markets on Polymarket are pricing in an 85.2% probability that Iran closes the strait before the end of 2026. Brent crude has spiked to $77.24 per barrel on March 2, while WTI has surged to just over $80 per barrel today. Here is a look at four publicly traded companies analysts have identified as having direct exposure to the geopolitical shift.

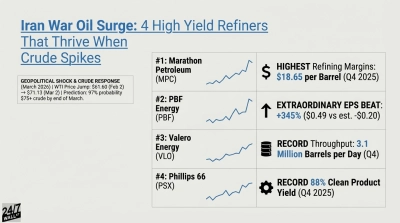

1. Valero Energy (VLO)

Valero Energy (NYSE:VLO) is the most immediate beneficiary of a supply-tightening event. Refiners profit from crack spreads, the margin between crude input costs and refined product prices, and geopolitical disruptions historically compress crude supply while keeping product demand steady, widening those spreads dramatically. Valero entered this environment with record refining throughput of 3.1 million barrels per day in Q4 2025, giving it maximum capacity to capture any margin expansion. VLO shares are up 25.95% over the past month and 13% in just the past week, now trading at $225.60 against a 52-week low of $96.17. Q4 refining segment results already demonstrated what tighter supply does to its income statement: refining segment operating income came in at $1.69 billion versus $437 million a year earlier. With analysts carrying a consensus target of $199.89, the stock has blown past that level on geopolitical momentum, and any sustained Hormuz disruption could reset those targets materially higher.

2. Exxon Mobil (XOM)

Exxon Mobil (NYSE:XOM) benefits on two fronts: higher crude realizations lift upstream earnings directly, and its refining operations capture wider crack spreads simultaneously. The company reported record production of 4.7 million oil-equivalent barrels per day in 2025, its highest output in over 40 years, with the Permian Basin hitting a record 1.8 million boed in Q4. Critically, 59% of production comes from advantaged assets in the Permian, Guyana, and LNG, all outside the conflict zone. The Golden Pass LNG project, with first cargoes expected in Q1 2026, arrives precisely as European and Asian buyers scramble for non-Middle Eastern supply. XOM shares are up 9% over the past month, though they have pulled back 1.32% in Thursday’s early session to $149.82. The analyst consensus target of $144.25 now sits below the current price, suggesting the market is pricing in a geopolitical premium analysts have yet to formally incorporate.

3. Baker Hughes (BKR)

Baker Hughes (NASDAQ:BKR) plays the conflict through LNG infrastructure and oilfield services in non-Iranian producing regions. Its Industrial and Energy Technology segment carries a record backlog of $32.4 billion, built on LNG equipment awards including NextDecade’s Rio Grande LNG and Alaska LNG projects. As Europe and Asia accelerate their search for non-Middle Eastern supply, that backlog becomes more strategically valuable. CEO Lorenzo Simonelli pointed to “continued momentum in LNG, a stronger year of FPSO and gas infrastructure awards” as a core theme heading into 2026. The near-term picture is more nuanced: BKR shares have pulled back 6.09% since March 2, likely reflecting concerns about its $1.39 billion Middle East/Asia OFSE revenue base, which faces direct operational disruption risk. Year-to-date, BKR is still up 34.2%, and the analyst community remains broadly bullish with a consensus target of $61.38.

4. Halliburton (HAL)

Halliburton (NYSE:HAL) stands to gain as drilling and completion activity accelerates in non-Iranian basins, particularly the Permian, offshore Guyana, and Middle Eastern fields outside the direct conflict zone. Its international revenue grew 7% in Q4 2025, demonstrating the breadth of its non-North American footprint. CEO Jeff Miller noted that the “international business is strong” heading into 2026. Halliburton’s forward P/E of 15x represents the lowest forward valuation among the four companies covered here, with an analyst consensus target of $36.50 against a current price of $34.43. Like BKR, HAL has retreated 3.81% since March 2, as the market weighs direct Middle East operational exposure against the broader activity uplift thesis.

What Investors Should Watch

The key variable across all four names is whether the Strait of Hormuz disruption materializes or remains a threat premium. Polymarket’s 82.5% probability of closure by March 31 (a separate near-term market from the 85.2% end-of-2026 contract) has driven the bulk of recent price action, particularly for VLO and XOM. A de-escalation scenario would likely unwind refiner gains fastest, given how sharply crack spreads have repriced. BKR and HAL have longer-duration LNG infrastructure backlogs that analysts have noted may provide earnings support regardless of near-term Hormuz outcomes, according to company guidance. Brent crude at $77.24 remains well below the $80.37 peak seen in June 2025 and far below the 2022 energy crisis highs, suggesting the market is not yet pricing a worst-case scenario into oil itself.