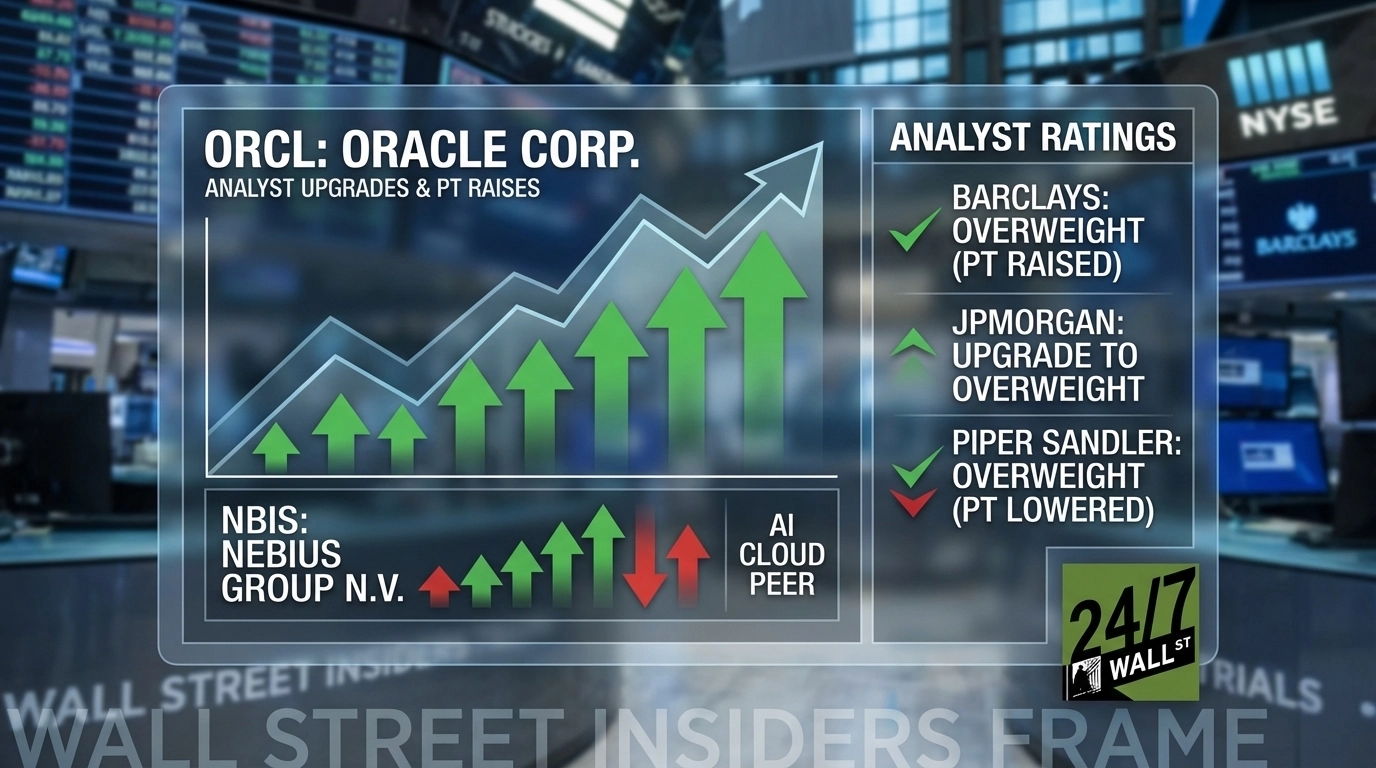

Oracle Corporation (NYSE:ORCL | ORCL Price Prediction) stock is up over 10% in premarket trading on Wednesday after the company delivered a fiscal Q3 2026 earnings report that put to rest several lingering investor concerns, prompting Barclays to raise its price target, JPMorgan to upgrade the stock, and Piper Sandler to reaffirm its bullish stance. The results mark what Oracle calls the first time in over 15 years that organic total revenue and non-GAAP EPS both grew 20%+ in the same period, driven by AI-fueled cloud infrastructure demand that management says continues to exceed supply. Also in focus this week, AI cloud infrastructure peer Nebius Group N.V. (NASDAQ:NBIS) offers a useful lens into the broader AI cloud build-out theme that is reshaping Wall Street’s view of enterprise technology.

| Ticker | Company Name | Firm | Old → New Rating | New Price Target | One-Line Takeaway |

|---|---|---|---|---|---|

| ORCL | Oracle Corporation | Barclays | Overweight → Overweight (PT raised) | $240 | Q3 addressed key investor concerns; shares “starting to work better from here” |

| ORCL | Oracle Corporation | JPMorgan | Neutral → Overweight | $210 | 55% share decline since mid-September creates improved risk/reward |

| ORCL | Oracle Corporation | Piper Sandler | Overweight → Overweight (PT lowered) | $210 | Multiple de-rating acknowledged; demand still outpacing supply in AI cloud |

The Analyst’s Case

Barclays raised its price target on Oracle to $240 from $230 while maintaining its Overweight rating, saying the Q3 print addressed several investor concerns around capital expenditures, the gross margin profile of contracts, and Oracle’s ability to deliver capacity on time. The firm sees other parts of the business, including software-as-a-service and maintenance, performing well, creating what it calls “plenty of upside” from current share levels, and sees the shares “starting to work better from here.”

JPMorgan upgraded Oracle to Overweight from Neutral, citing the 55% decline in shares since mid-September and Oracle’s delivery on its growth acceleration. The firm noted that investor sentiment had shifted from “blind faith to widespread pessimism” over the attainability of Oracle’s fiscal 2030 targets, and sees an improved risk/reward against that backdrop. JPMorgan’s new price target is $210, down from $230, reflecting a more conservative multiple assumption even as the firm turns constructive on the name.

Piper Sandler analyst Billy Fitzsimmons lowered his price target to $210 from $240 to reflect the multiple de-rating across software broadly, while keeping an Overweight rating. Fitzsimmons noted that Oracle provided “breadcrumbs” in Q3 that should help partially ease investor concerns, with demand for AI cloud computing continuing to grow faster than supply. Management expects to “comfortably meet and likely exceed” its growth rate forecast for FY27 and beyond.

Company Snapshot and Recent Performance

Oracle is one of the world’s largest enterprise software and cloud infrastructure companies, with a market cap of approximately $429 billion. Its cloud infrastructure segment has become the primary growth engine, with IaaS revenue reaching $4.89 billion in Q3, up 84% year over year, driven by AI training and inferencing workloads. Total cloud revenue came in at $8.91 billion, up 44% year over year. The company’s Remaining Performance Obligations, a forward-looking indicator of contracted future revenue, surged to $553 billion, up 325% year over year, driven by large-scale AI contracts.

The stock has been under significant pressure heading into this report. Oracle shares are down 23.16% year to date as of March 10, falling from $194.42 at year-end to $149.40. Much of that decline followed Oracle’s Q2 report in December, when the stock dropped roughly 13% on a revenue miss despite a strong EPS beat. Reddit sentiment data tells the same story: sentiment on Oracle was rated “very bearish” as recently as March 9, with posts like “What is wrong with Oracle?” dominating retail investor discussions. That changed sharply on March 10 following the earnings release, with sentiment flipping to “very bullish” with a score of 80 by Tuesday evening.

Nebius Group, a pure-play AI cloud infrastructure company that has emerged as one of the fastest-growing names in the space, provides useful context for the AI cloud build-out theme. Nebius reported Q4 2025 revenue of $227.7 million, up 503.6% year over year, with its AI Cloud segment alone growing 800% year over year. Nebius shares have gained 15.2% year to date, a stark contrast to Oracle’s YTD decline, though the two companies are at very different stages of scale. Analyst consensus on Nebius carries a price target of $147.45, implying roughly 53% upside from current levels.

Why the Move Matters Now

The combination of Oracle’s Q3 results and the multi-firm analyst response reflects a meaningful recalibration of how Wall Street is thinking about the stock after months of deteriorating sentiment. The Q3 print delivered on the metrics that matter most for the AI cloud thesis: IaaS up 84%, multicloud database revenue up 531%, and an RPO figure that signals the pipeline is not slowing. Oracle also raised its FY2027 total revenue guidance to $90 billion, a figure that had been a central point of skepticism for investors.

The analyst consensus price target sits at $253.08 with 32 buy ratings, 10 holds, and just 1 sell among covering analysts. At Oracle’s current price of $149.40, the new targets from JPMorgan and Piper Sandler at $210 and Barclays’ $240 target both sit meaningfully above current levels.

The counterweight to that optimism is real. Oracle is carrying $124.7 billion in non-current debt and generated negative free cash flow of -$24.74 billion in Q3 due to $48.25 billion in capital expenditures. The company has also announced plans to raise up to $50 billion in additional debt and equity financing for further data center expansion. Interest expense grew 32% year over year. These are not small risks, and they help explain why JPMorgan trimmed its price target even as it upgraded the stock.

Key Takeaways

For long-term investors, Oracle’s Q3 report and the subsequent wave of analyst support represent a meaningful shift in the stock’s near-term narrative. The core bull case, that Oracle is building the AI infrastructure backbone that enterprises and hyperscalers need, received tangible validation in the form of an $553 billion RPO balance and accelerating IaaS growth. The composite sentiment index of 68.79 with a 7-day trend change of +22.61 suggests momentum is shifting.

That said, the capital intensity of Oracle’s expansion strategy means free cash flow will remain negative for the foreseeable future, and the debt load warrants ongoing scrutiny. Oracle pays a quarterly dividend of quarterly dividend of $0.50 per share, and its RPO pipeline of $553 billion stands alongside a balance sheet being stretched by significant capital expenditures and a growing debt load. The Q3 print reduces the near-term risk, but the longer-term thesis still depends on Oracle executing on a $90 billion revenue target by FY2027 in a capital-intensive, GPU-supply-constrained environment.

Contact [email protected] for any questions or corrections.