Oracle (NYSE:ORCL | ORCL Price Prediction) just turned in the quarter that finally validates the AI infrastructure thesis. Cloud Infrastructure revenue jumped 93% year over year to $5.79 billion in Q4 FY2026, and the remaining performance obligation backlog now sits at $638 billion.

Shares closed at $201.26 on June 10, up just 3.89% year to date. The disconnect between booked backlog and share price is the entire story. Can ORCL hit $400 by 2027?

Why Oracle Shares Are Stuck Despite Record Backlog

The setup looks great on paper. The tape disagrees. ORCL fell 12.62% in the past week alone and trades 26% below its 52-week high of $343.01. The problem is the bill that pays for the growth.

Oracle burned through $55.66 billion in capex during FY2026 and posted negative $23.69 billion in free cash flow. Management plans to raise approximately $40 billion through debt and equity in FY2027. Pre-earnings news flow flagged capex anxiety, rising debt levels, and valuation concerns as the dominant overhang.

With a beta of 1.655, the stock swings hard when sentiment shifts. Right now sentiment questions whether the buildout pays off before the balance sheet creaks. That’s an honest concern that stops short of breaking the thesis. But it is why the stock is stuck.

Wall Street Sees 27% Upside. I Think That’s Too Conservative

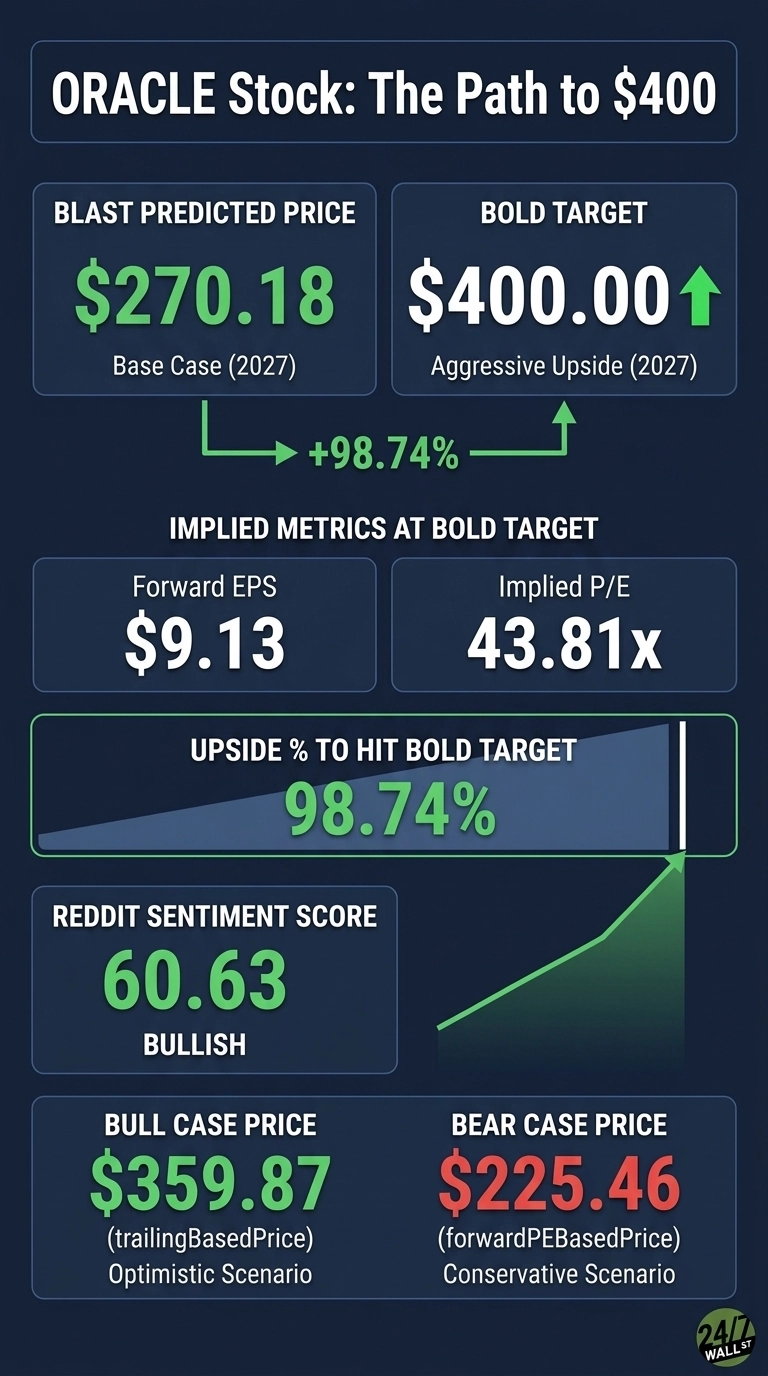

The consensus target sits at $255.18, implying roughly 26.8% upside. The rating split is heavily one-sided: 6 Strong Buy, 30 Buy, 6 Hold, and just 1 Sell. Our internal model puts the base case at $270.18 with 34.24% upside and 90% confidence, with an optimistic scenario reaching $359.87.

Analysts are anchored to trailing multiples and haven’t fully marked up forward EPS to reflect the OCI ramp. Bullish analyst share runs 84%, and earnings growth is tracking 24.5% YoY. When OCI scales from $18 billion in FY2026 to a projected $32 billion in FY2027, those $255 targets get revised. That is how stretch targets become base cases.

Barclays raised the firm’s price target on Oracle to $250 from $240 and keeps an Overweight rating on the shares following the fiscal Q4 report. Further, Bernstein analyst Mark Moerdler raised the firm’s price target on Oracle to $325 from $319 and keeps an Outperform rating on the shares while Citi has a buy rating with a price target of $330.

The Path to $400 Per Share

Reaching $400 from today’s price of $201.26 would require a gain of 98.7%. That’s a doubling. With forward EPS of $9.13, a price of $400 implies a forward P/E of 44x. Our base case of $270.18 already implies 26x, meaning the bold target requires roughly 17x of additional multiple expansion.

That is achievable only if the OCI growth story compounds. Cloud Infrastructure accelerated from 55% growth in Q1 to 93% by Q4, and Multicloud database grew 404% in Q4.

Co-CEO Clay Magouyrk told investors “Oracle is very good at building and running high-performance and cost-efficient cloud datacenters”, citing 211 live and planned regions.

Co-CEO Mike Sicilia added that “All of the top five AI Models are in the Oracle Cloud”. Evercore ISI, TD Cowen, Oppenheimer, and JPMorgan have all raised price targets. The primary risk: if hyperscaler customers slow GPU prepayments, the RPO conversion narrative cracks.

Where Oracle Trades Today vs Its Earnings Power

At $201.26, ORCL trades at roughly 22x forward EPS of $9.13. That is not expensive for a software franchise growing earnings 24.5% YoY. Shares sit well off the 52-week high of $343.01 and well above the low of $134.57.

Over the past decade the stock has returned 503.09%, and the AI cycle is arguably more meaningful than anything that drove that prior run. Today’s multiple does not yet price in $32 billion of FY2027 OCI revenue.

Is $400 Realistic? My Verdict

Reaching $400 by 2027 requires a 98.7% gain. That’s a stretch target well above our base case.

To get there, Oracle needs OCI to keep compounding north of 80%, the $40 billion FY2027 financing has to land without spooking credit markets, and at least one more multi-billion AI contract needs to print. What derails it is a slowdown in hyperscaler GPU commitments. We’ve outlined the blueprint for how Oracle could reach $400 in 2027.

Contact [email protected] for any questions or corrections.