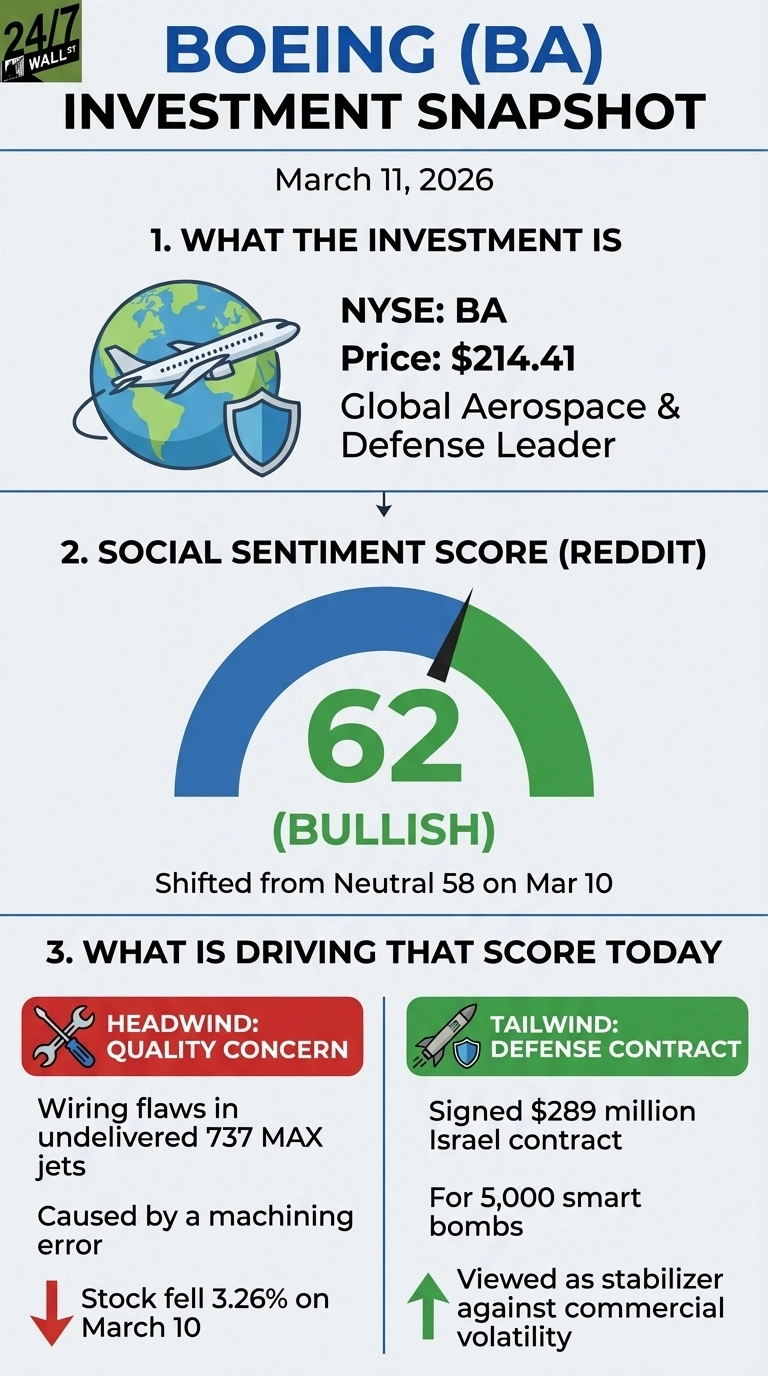

The most prolific name in aeromanufacturing, Boeing (NYSE:BA | BA Price Prediction) shares fell 3.26% on March 10 after the company disclosed wiring flaws in undelivered 737 MAX jets caused by a machining error, and the stock is down 9.3% over the past month. Reddit sentiment shifted from neutral 58 on Tuesday evening to bullish 62 by Wednesday morning, with retail investors looking past the defective headline toward a fresh defense contract announced the same day.

A Wiring Problem at the Wrong Moment

On the plus side for investors, Boeing posted its first annual profit since 2018 last year, with $2.2 billion in net income for 2025. Commercial deliveries accelerated every quarter, hitting 51 jets in February 2026, the highest February total since 2018. CEO Kelly Ortberg told investors on the Q4 call: “We haven’t fully turned the corner, but we’re making real progress in getting back to the Boeing everyone expects of us.”

Boeing says the wiring fix is quick and does not expect the issue to impact its full-year target of 500 737 MAX deliveries in 2026, but the market knows the pattern. The 737 MAX door plug detachment in 2024 reset expectations once already. A new manufacturing defect, however minor, reopens the question of whether quality culture has genuinely changed. The Commercial Airplanes division is still running at a negative 6.05% operating margin despite $11.38 billion in Q4 revenue, up 139% year-over-year, and total debt sits at $54.1 billion.

Reddit Finds a Silver Lining in Defense

Discussion in r/stocks spiked around a post titled “Boeing signs $289 million Israel contract for 5,000 smart bombs, source says”, drawing 669 upvotes and 108 comments with a 95% upvote ratio. Sentiment skewed bullish, with defense revenue seen as a stabilizer against commercial volatility.

As one commenter noted in the thread: “Boeing signs $289 million Israel contract for 5,000 smart bombs, source says” – the post drew 669 upvotes and 108 comments from users viewing the defense deal as a near-term positive amid the wiring headline.

Boeing signs $289 million Israel contract for 5,000 smart bombs, source says

by u/seeking-health in stocks

The broader picture remains split, with both Commercial Airplanes and Defense operating at negative margins despite surging revenue. The 777X program’s first delivery has slipped to 2027, with a potential engine durability issue disclosed on the Q4 call. Free cash flow guidance for 2026 is positive, $1 billion to $3 billion, but the long-term target requires production stability that Boeing has not yet proven it can hold.

The Clearest Near-Term Catalyst

Analyst consensus is a moderate buy, with an average price target of around $246, compared with a current price of $214. Certification of the 737-7 and 737-10 variants, still expected in 2026, would unlock over 1,500 high-margin aircraft in the backlog and is the single clearest near-term catalyst. Until then, every new production defect will keep testing whether the turnaround is structural or just a run of good quarters.

Contact [email protected] for any questions or corrections.