Boeing (NYSE: BA | BA Price Prediction), Honeywell (NASDAQ: HON), and 3M (NYSE: MMM) have all pulled back sharply over the past month. Each just reported Q4 2025 earnings, and each tells a very different story about what “dip” actually means.

Three Dips, Three Very Different Situations

Boeing has taken the hardest hit, falling 12.9% over the past month and was last seen trading around $200 a share. The underlying business remains in recovery mode. Q4 revenue came in at $23.95 billion, up 57% year-over-year, though the headline EPS of $9.92 was almost entirely driven by a $9.67 billion gain from the Digital Aviation Solutions divestiture. Strip that out and both Commercial Airplanes and Defense segments are still running at negative operating margins of −5.6% and −6.8%, respectively. Full-year free cash flow was −$1.877 billion, and consolidated debt sits at $54.1 billion. CEO Kelly Ortberg called it a foundation year: “We made significant progress on our recovery in 2025 and have set the foundation to keep our momentum going in the year ahead.”

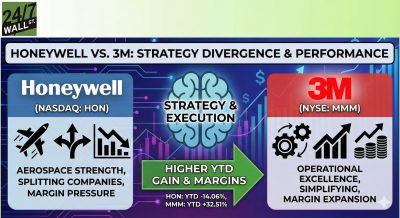

3M’s −11.2% one-month decline, currently trading around $147, reflects a different kind of pressure. The business is executing well. Adjusted operating margin expanded 140 basis points to 21.1% in Q4, and CEO William Brown guided for 2026 adjusted EPS of $8.50 to $8.70 with further margin expansion. The problem is litigation. PFAS-related net pre-tax cash payments totaled $3.5 billion in 2025, and JPMorgan downgraded the stock, citing lingering PFAS valuation risks. The gap between adjusted and GAAP earnings tells the story: Q4 GAAP EPS was $1.07, down 20% year-over-year, versus adjusted EPS of $1.83.

Honeywell’s −7.0% pullback, t0 about $226, is the shallowest of the three and arguably the least compelling entry point. The stock is still up 15.8% year-to-date. Q4 results were solid: Aerospace Technologies posted 21% organic sales growth, and the company exited 2025 with a record backlog above $37 billion. The major catalyst ahead is the planned separation of its aerospace and automation businesses, expected in Q3 2026, but the market has already been pricing it in.

Valuation and Analyst Targets

| Metric | Boeing | 3M | Honeywell |

|---|---|---|---|

| One-Month Decline | −12.9% | −11.2% | −7.0% |

| Current Price | $200 | $147 | $226 |

| Analyst Consensus Target | $272.25 | $178.73 | $251.44 |

| Consensus Rating | BUY | HOLD | HOLD |

| Forward P/E | 137x | 17x | 22x |

The Verdict

Boeing carries the most upside and the most risk. Analyst consensus sits at $272.25 with 20 buy-side ratings, and the base target is $327.47. Reddit sentiment has been consistently bullish at a score of 62 even through the drawdown, driven partly by a $289 million Israel defense contract. But a forward P/E near 137x on a company still burning cash is not a retirement-account staple. This is a turnaround bet, not a stability play.

3M offers the more balanced case. The operational turnaround under Brown is genuine, the dividend yield is 2.2%, and net free cash flow guidance of $4.6 billion to $4.8 billion for 2026 is credible. The company has exited manufactured PFAS products and is making cash payments to resolve liabilities. At a forward P/E of 17x, the valuation is reasonable. The consensus target of $178.73 reflects the litigation discount rather than business quality, undervaluing the operational improvements.

Honeywell has not pulled back enough to be compelling. With the stock still above its year-start price and the analyst target of $251.44, the risk-reward profile appears limited at current levels. The aerospace separation is a legitimate long-term catalyst, but the separation timeline extends into Q3 2026.

For investors evaluating industrial exposure, 3M and Boeing present very different profiles. The 3M dip is real, fundamentals are improving, the dividend is intact, and the litigation trajectory is becoming more predictable. Boeing carries far more upside potential, though the balance sheet risk and cash burn remain significant considerations.

Contact [email protected] for any questions or corrections.