Unilever (NYSE:UL | UL Price Prediction) reported full-year 2025 results on February 12, while Kimberly-Clark (NYSE:KMB) dropped Q4 2025 numbers on January 27. Both are consumer staples giants mid-portfolio reshuffle, and both pay growing dividends. But how do the two compare for income investors?

Portfolio Surgery at Both Companies, Different Scalpels

Unilever completed its Ice Cream demerger in December 2025, generating a $3.37B gain and shedding a low-growth margin drag. What remains is built around Dove, Hellmann’s, Liquid I.V., and premium beauty brands like Hourglass, K18, and Dermalogica. CEO Fernando Fernandez put it plainly: “In 2025 we became a simpler, sharper, and faster Unilever, delivering our commitment to volume growth, positive mix and strong gross margin.”

Underlying operating margin hit 20.0% for the full year, up 60 basis points. Free cash flow came in at $5.921B. North America delivered 5.3% underlying sales growth with 3.8% volume growth, signaling real consumer demand, not just pricing.

Kimberly-Clark’s transformation looks different. The divestiture of its U.S. private label diaper business dragged reported revenue down 17.2% year-over-year in Q4 to $4.08B. Strip that out and organic sales grew 2.1%, with volume-plus-mix up 3.0%. Adjusted operating profit jumped 13.1%. CEO Mike Hsu called the quarter a “springboard” and described the pending Kenvue acquisition as “a powerful next step in our transformation.”

The Dividend Math Tells Two Different Stories

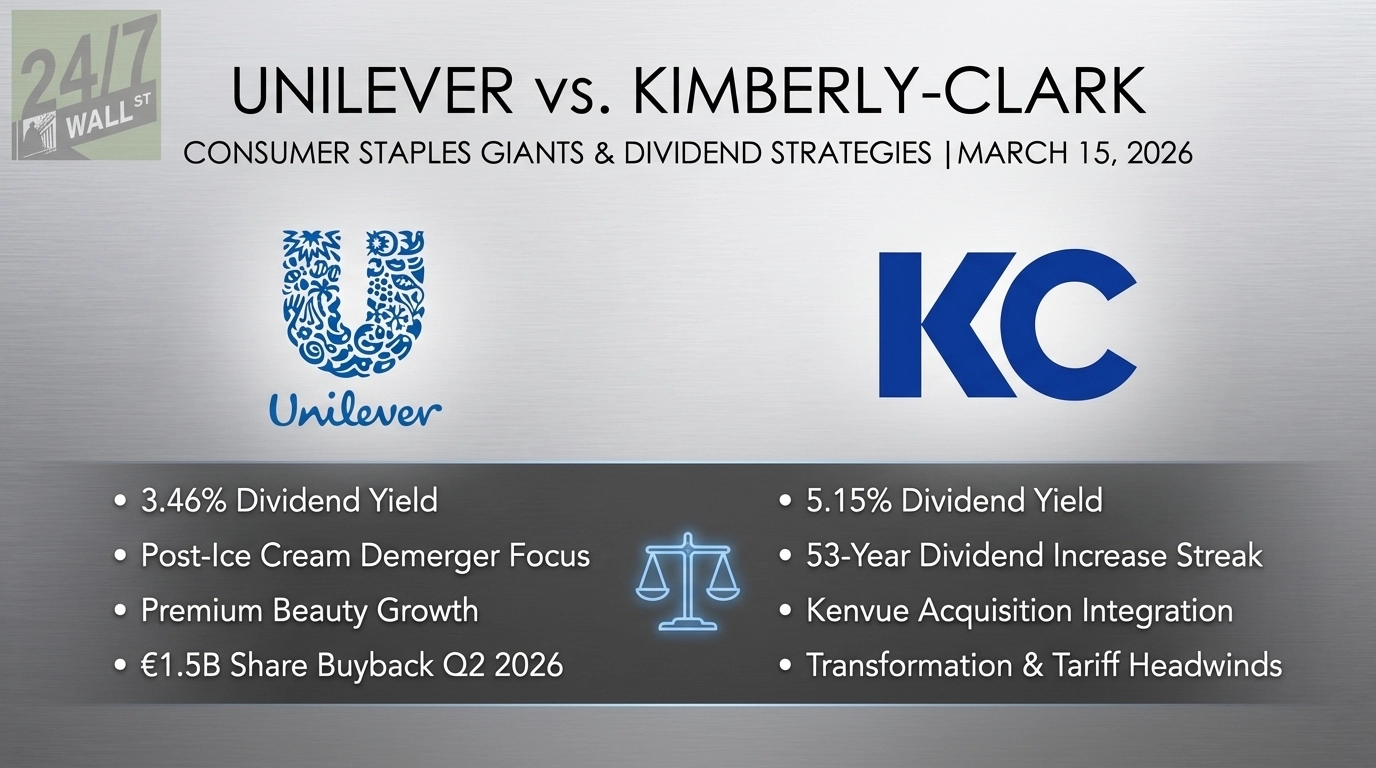

| Metric | Unilever (UL) | Kimberly-Clark (KMB) |

|---|---|---|

| Dividend Yield | 3.46% | 5.15% |

| Annual Dividend | $1.977/ADR | $5.04/share |

| Consecutive Increase Streak | ~3% YoY growth | 53 consecutive years |

| Forward P/E | 17x | 13x |

| Free Cash Flow (FY2025) | $5.921B | $1.639B |

Kimberly-Clark’s 5.15% yield is hard to ignore, backed by a 53-year streak of consecutive increases. The most recent quarterly dividend stepped up to $1.28 in Q1 2026. That streak ranks among the longest in the market and reflects a management culture that treats the dividend as nearly sacred.

Unilever’s yield at 3.46% is lower, but the business looks cleaner post-Ice Cream. A new share buyback of up to €1.5B begins in Q2 2026, adding another return-of-capital layer.

What to Watch Ahead

For Kimberly-Clark, the Kenvue integration is the biggest variable. The company already faces $300M in tariff headwinds flagged for 2026. If Hsu delivers double-digit adjusted EPS growth as guided while absorbing that pressure, the stock at 13x forward earnings trades below its historical average. The 26% one-year price decline has already priced in significant fear.

For Unilever, the question is whether the premium beauty bet keeps gaining traction. Brands like Nutrafol and K18 are growing fast but must scale without losing their premium positioning. Currency remains a drag, with 5.9% currency headwinds hitting reported revenue in 2025.

Two Different Names for Two Different Priorities

Kimberly-Clark carries a 53-year dividend streak at a 5.15% yield and trades at 13x forward earnings, with a transformation roadmap that includes execution risk alongside potential upside if management delivers its guidance. Unilever offers broader global reach across 190 countries, premium brand momentum, expanding margins, and a buyback on deck, with a lower yield as the tradeoff for a cleaner post-restructuring story. These two names serve genuinely different priorities.

Contact [email protected] for any questions or corrections.