Cloudflare (NYSE:NET | NET Price Prediction) stock is up 8% in afternoon trading on Wednesday, with shares changing hands at around $228. The broader market is not participating, though: the S&P 500 is down on the day, making Cloudflare stock’s move stand out even more sharply against the tape.

The catalyst is not a single news item. Instead, it’s the growing investor conviction that as NVIDIA (NASDAQ:NVDA) powered AI workloads scale beyond the data center and push toward the edge, Cloudflare is a network those workloads will need to pass through. That thesis is gaining traction fast.

NVIDIA’s AI Boom Creates a New Kind of Infrastructure Winner

NVDA stock is essentially flat today, but the company’s recent earnings report continues to reshape how investors think about the AI infrastructure stack. NVIDIA reported $68.13 billion in quarterly revenue, up 73.2% year over year, with data center revenue alone hitting $62.31 billion, up 75%

This story relates directly to Cloudflare. AI agents need to reach users, query APIs, execute tasks, and return results in real time. Every one of those interactions has to travel across a network. Cloudflare sits in front of more than 20% of all websites, making it one of the most logical beneficiaries of that traffic explosion.

Cloudflare’s Own Numbers Back the Story

Cloudflare’s Q4 FY2025 results, reported on February 10, were genuinely strong across every dimension that matters for a company at this stage of growth. Revenue came in at $614.51 million, up 33.6% year over year, beating the consensus estimate of $591.24 million by 3.94%. Non-GAAP EPS was $0.28, beating the $0.27 estimate. Furthermore, Cloudflare’s free cash flow hit $99.44 million, a 16% margin that more than doubled year over year.

The enterprise pipeline is what really caught Wall Street’s attention, though. Cloudflare closed its largest annual contract value deal ever, averaging $42.5 million per year. Also, Cloudflare’s total new annual contract value (ACV) grew nearly 50% year over year, the fastest pace since 2021.

Additionally, Cloudflare’s remaining performance obligations grew 48% year over year. These aren’t just vanity metrics, and 48% growth means the backlog is building fast.

CEO Matthew Prince framed Cloudflare’s AI positioning directly, asserting, “If agents are the new users of the web, Cloudflare is the platform they run on and the network they pass through.”

Prince went even further, describing an AI flywheel where “more agents drive more code to Cloudflare Workers, which fuels demand for our performance, security, and networking services.” That’s a compounding growth loop, not a one-time tailwind.

Analyst Sentiment and the Valuation Reality

The analyst community is mostly constructive on NET stock. RBC and Stifel have remained bullish on Cloudflare, while UBS adjusted its share-price target to $210 but maintained a Neutral rating.

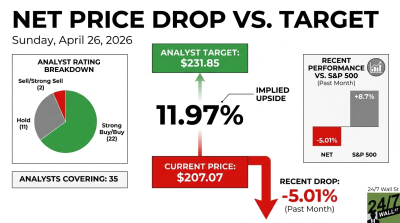

The consensus analyst target for Cloudflare stock sits at $232.43, with 17 analysts rating it a Buy and 5 rating it a Strong Buy against just 3 Sell-side ratings combined. At today’s price, NET is trading fairly close to the consensus analyst target of $232.43.

Meanwhile, Cloudflare’s valuation isn’t cheap by any traditional measure. The forward P/E sits around 175x, and the price-to-sales ratio is 34x trailing revenue.

With NET stock, you’re paying for a future where agentic AI traffic becomes a massive, monetizable flow across Cloudflare’s network. If that future arrives on schedule, the current multiple may be sustainable. On the other hand, if the AI agent buildout stalls or hyperscalers decide to internalize more edge delivery, Cloudflare stock could face valuation pressure.

For context on where retail sentiment has been, we recently noted that Reddit was firmly bullish on NET stock even as the valuation math looked stretched. That dynamic has not resolved.

Reddit sentiment scores for Cloudflare stock ranged from 68 to 78 throughout early March, with peak engagement hitting 1,538 upvotes and 140 comments in a single overnight window on March 10. Retail conviction is high. Whether fundamentals catch up to that conviction is the real question.

What to Watch

NET shares are up 98% over the past year, and the stock has cleared its 50-day moving average of $186.17 with room to spare. The 52-week high of $260 is the next meaningful technical reference point.

Cloudflare also raised $2 billion in 2030 convertible senior notes to fund its growth buildout, giving it a long runway to invest in AI edge infrastructure without needing to tap equity markets.

The $225 level and the 52-week high represent the next meaningful technical reference points worth watching for NET stock. The company’s Q1 FY2026 guidance of $620 million to $621 million in revenue gives investors a clear near-term benchmark, and any update to that outlook or enterprise deal flow commentary will be a potential catalyst to track.

To sum it up, Cloudflare’s AI edge story is real. Going forward, the question will be whether today’s share price already reflects the positive assumptions.

Contact [email protected] for any questions or corrections.