When we think about cloud infrastructure powering the internet, AWS typically dominates. But Cloudflare (NASDAQ:NET | NET Price Prediction) is building something fundamentally different – and arguably more relevant for what comes next.

The Business Model Inversion

AWS built its empire centralizing compute in massive data centers. Cloudflare inverts this entirely, operating a distributed network spanning 330+ cities globally, positioning compute and security at the edge – closer to end users and AI workloads.

CEO Matthew Prince framed the opportunity on the Q1 2025 earnings call:

We have the scale, the technology, and the team to capture the massive opportunity ahead of us – as evidenced by the size and the length of the deals we’re closing and the caliber of customers betting on Cloudflare.

The company landed its largest contract in history during Q1 – over $100 million – driven primarily by the Workers developer platform. This is Cloudflare’s answer to AWS Lambda, architected for edge computing from day one.

Growth Acceleration While AWS Decelerates

Cloudflare’s revenue growth has accelerated for two consecutive quarters: 27% in Q2, then 31% in Q3 2025.

Q3 2025 delivered $562 million in revenue against estimates of $545 million, with non-GAAP EPS of $0.27 versus $0.23 expected. Operating margins expanded to 15.3% from 10.6% two quarters prior. The company generated $75 million in free cash flow – 13% of revenue – while narrowing GAAP net losses to just $1.3 million from $15.3 million a year ago.

Prince captured the momentum:

Our excellent third quarter results clearly demonstrate our increasing momentum, with revenue growth accelerating for the second consecutive quarter to 31% year-over-year.

The AI Infrastructure Play

Cloudflare’s edge architecture positions it uniquely for AI inference workloads. Training models requires centralized compute, but running AI applications at scale demands low-latency, distributed infrastructure – Cloudflare’s core competency.

The company is shipping products. The Workers AI platform lets developers deploy machine learning models globally without managing infrastructure. The recent Replicate acquisition adds more sophisticated AI deployment capabilities.

Valuation Reality Check

Trading at 34x sales with a forward P/E of 159x, Cloudflare isn’t cheap. CEO Prince sold $31.8 million in stock during early December, while President Michelle Zatlyn offloaded $15.8 million. Both transactions occurred through pre-arranged 10b5-1 plans at prices above $200, suggesting routine diversification rather than panic.

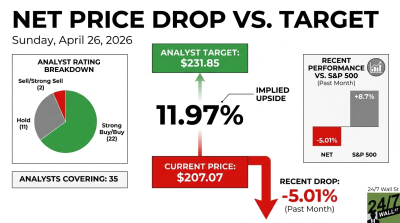

Barclays initiated coverage in December with a Buy rating and $235 price target, implying roughly 10% upside from current levels. The bull case hinges on whether Cloudflare can maintain 30%+ growth while expanding margins toward AWS-like profitability.

The company crossed $2 billion in annualized revenue in Q2 2025. AWS generates meaningfully over $100 billion annually. The question isn’t whether Cloudflare replaces AWS. Both are winners and will continue to be, in my opinion. It’s whether the edge computing model captures enough of the next wave of internet infrastructure spending to justify today’s valuation. Based on the growth trajectory and contract wins, that thesis looks increasingly credible.

Contact [email protected] for any questions or corrections.