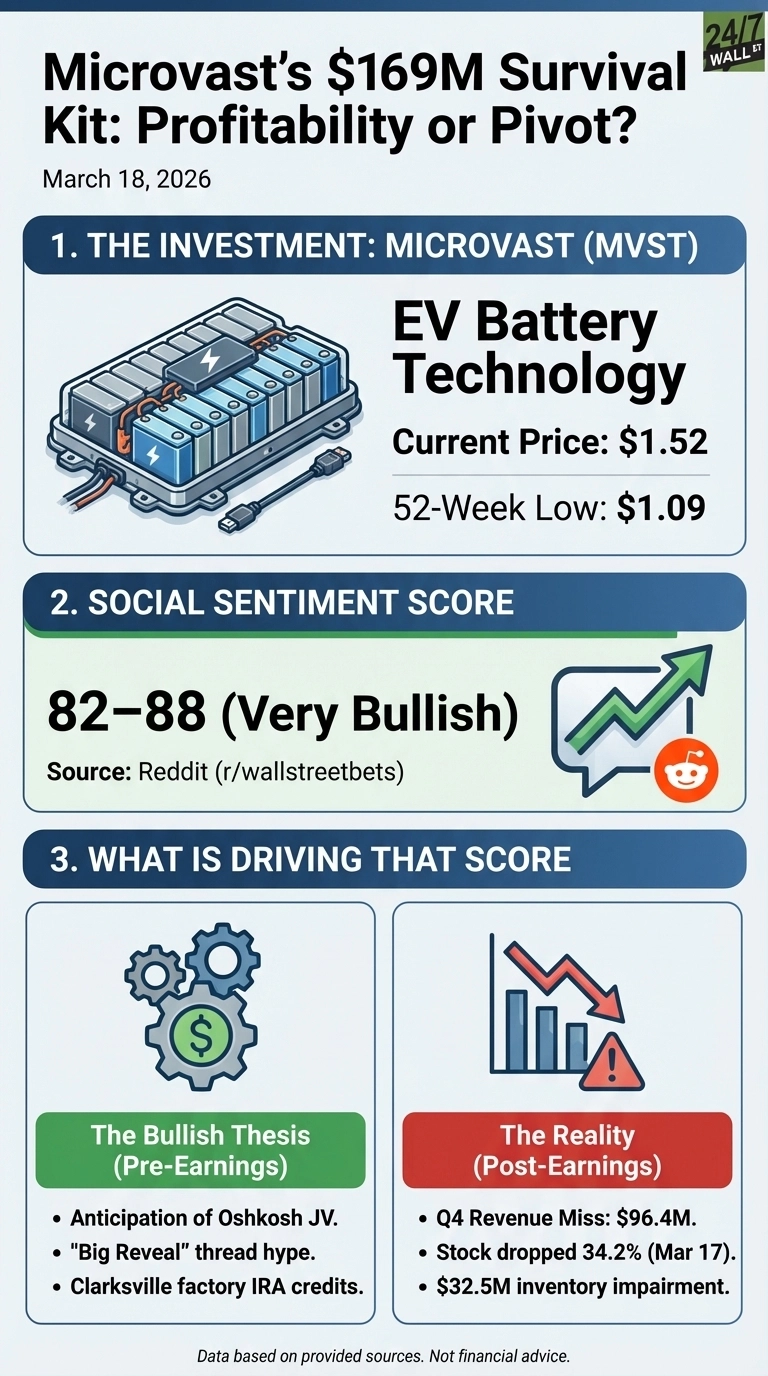

Microvast (NASDAQ:MVST) shares dropped 34.2% on March 17 after the battery maker reported Q4 2025 results that raised hard questions about whether its profitability story is real or manufactured. The stock sits at $1.52, down 46% year-to-date and near its 52-week low of $1.09. The Q4 miss was severe: revenue came in at $96.4 million against a consensus estimate of $133.75 million, a 26.6% shortfall. A $32.5 million inventory impairment charge crushed gross margin by 7.6 percentage points.

The full-year numbers tell a different story than Q4 alone. Annual 2025 revenue reached $427.5 million, a 12.6% year-over-year increase, and adjusted EBITDA swung from negative $44.8 million in 2024 to positive $44.7 million in 2025. Microvast also closed a $169 million capital raise that gives it runway for its U.S. manufacturing push. The question is whether those improvements reflect a genuine operational turn or accounting flexibility masking an uneven business.

While the $169 million cash pile is a buffer, the company’s recent 10-K filing explicitly mentioned ‘substantial doubt’ about its ability to continue as a going concern due to heavy near-term debt maturities, putting even more pressure on the U.S. manufacturing push to deliver results by year-end.

The r/wallstreetbets Thesis That Didn’t Survive Monday

Before earnings, Reddit sentiment was decidedly bullish. A due diligence post titled “DD on $MVST and $OSK: The Big Reveal is Monday” by user Atreides— accumulated 192 upvotes and 196 comments by Monday evening, with sentiment scores peaking at 89 out of 100.

DD on $MVST and $OSK: The Big Reveal is Monday

by u/Atreides— in wallstreetbets

In the post, Atreides— wrote:

“The Clarksville factory activated through the Oshkosh JV structure qualifies for IRA 45X tax credits, creating a structural cost advantage over imported alternatives — this is the big reveal Monday.”

The post argued Microvast had engineered a turnaround through a structured joint venture with Oshkosh Corporation (NYSE:OSK | OSK Price Prediction) Oshkosh Corporation to activate its Clarksville, TN factory, pointing to equipment imports, M&A-focused hiring, and tax credit mechanics. The author held 90,000 shares with a $17 price target. The earnings miss erased that optimism fast. The bullish case rested on three pillars:

- US revenue grew 173% year-over-year, though the CFO attributed this largely to customers accelerating deliveries ahead of tariff uncertainty, not organic demand growth

- A $169 million financing raise and insider ownership around 29.7% signaling management’s commitment to the long-term build

- The Clarksville factory, activated through a JV structure, would qualify for IRA 45X credits of $10 per kWh for domestic battery pack assembly, creating a structural cost advantage over imported alternatives

Why the Q4 Miss Matters More Than the Full-Year EBITDA Swing

Microvast reported a full-year GAAP net loss of $29.2 million despite the adjusted EBITDA swing. A shareholder investigation announced by Holzer & Holzer on March 17 over the inventory impairment charge adds legal overhang. CEO Yang Wu stated the 2026 strategy focuses on “accelerating path to profitability by optimizing R&D to production cycles and scaling with margin integrity.”

Analysts carry a consensus price target of $7 against a current price of $1.52, but closing that gap runs directly through whether Clarksville’s initial 2 GWh pack capacity produces real revenue in 2026 or stays a promise on a slide deck. With a newly issued ‘going concern’ warning in the latest 10-K, the timeline for Tennessee is no longer just a growth milestone, it is a survival necessity.

Data Sources

- Microvast Q4 2025 Earnings Call Highlights: Used for full-year revenue, EBITDA swing, US revenue growth attribution, inventory impairment margin impact, and CEO 2026 strategy quote

- Microvast Holdings (MVST) Is Up 10.0% After Posting Q4 Profit: Used for Q4 net income, full-year net loss, finance leadership overhaul context, and analyst revenue forecasts

- Fuse API Reddit Sentiment Data: Used for sentiment scores, upvote/comment trajectory, and primary Reddit thread details, including author position and JV thesis

- Alpha Vantage News Sentiment: Used for Q4 revenue miss vs. estimates, inventory impairment charge, legal investigation announcement, and insider ownership figures

Contact [email protected] for any questions or corrections.