Oil prices have soared by over 50% in the past month, with WTI crude trading sideways in the $90 to $100 band. Stocks like Exxon Mobil (NYSE:XOM), Occidental Petroleum (NYSE:OXY), and Marathon Petroleum (NYSE:MPC) have rallied by just 10% or less due to the broader market believing the Strait of Hormuz will be open quickly. The opening of the Strait remains tentative, and it could take weeks for oil prices to normalize.

J.P. Morgan’s base case before the conflict was Brent averaging roughly $60/barrel for the full-year 2026. OPEC+ was planning to increase its production to 206,000 barrels per day in April. The market has not forgotten any of that and still believes oil prices will retreat quickly after the conflict winds down.

That said, the market’s assumption of a quick reopening is shaky. The sporadic attacks over the Strait have slowed traffic down to a trickle. Iran has refused to engage in a ceasefire. Trump’s latest message about a 5-day postponement expires on Friday, which could lead to a worse flare-up.

Even if things do calm down, oil stocks are now well-positioned to keep rising as further investments are set to pour in to decentralize energy production away from the Gulf.

Exxon Mobil (XOM)

ExxonMobil gets most of its oil from the Permian Basin in the U.S., Guyana, and the Gulf of America/Mexico. It has operations in other countries in the Western Hemisphere and Oceania, and it’s well-insulated from volatility in the Gulf.

Being insulated does not seclude it from the benefits of higher oil prices. Most of the oil flowing out of the Strait of Hormuz goes to Asian countries, and those markets are now turning elsewhere for their energy. Hence, oil prices across the board are going up, and ExxonMobil is a clear beneficiary.

CEO Darren Woods opened by saying Exxon has built “a higher return, lower cost, technology-led company… in a league of our own,” and the numbers underneath that claim are hard to argue with. Those margins have gotten even fatter now.

Exxon Mobil is sending a team to Venezuela to assess investments there. It’s an earshot distance from Guyana, so there’s significant growth potential.

I expect XOM stock to keep surging if the Strait isn’t open by May and more demand shifts West.

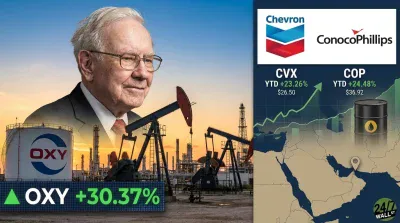

Occidental Petroleum (OXY)

Occidental Petroleum is Warren Buffett’s favorite oil stock. He religiously added more to his OXY holdings before stepping down as CEO, and these holdings are now paying off in spades. It is up almost 16% in the past month alone and is among the strongest-performing oil companies now, because the Permian Basin is the absolute bedrock of the company.

Occidental recently exited the chemicals business, meaning it is more production-focused than companies like ExxonMobil. That makes it an even more “pure-play” bet on oil in this environment. Of course, this is a double-edged sword, since a post-ceasefire environment will be worse for OXY if oil prices tumble.

Still, OXY stock was doing well before February and is a cash cow. Debt was over $40 billion back in 2019 and tumbled to $23.35 billion in 2025. The rapid debt payoff, plus the oil focus, can cause it to surge above the 2024 peak and beyond.

The stock trades at just 0.71 times projected free cash flow. The median oil stock trades at 0.8 times, and a company this lean should trade much higher. The FCF margin here is 19%, with the EBITDA margin at 54%; both are better than 80% of oil and gas companies.

Marathon Petroleum (MPC)

Marathon Petroleum is less about extracting oil and more about refining that oil. This company spans the full downstream stretch of the energy chain, with crude oil arriving at its refineries and then being sold at the station.

The higher oil prices are already translating into pain at the pump for many Americans. But for Marathon, it’s a boon, as higher prices allow it to widen its margins.

MPC stock is already up 56% over the past year and is up nearly 500% since February 2020. This surge is not just because investors are bullish on oil refining, but also because the company has embarked on an extremely aggressive buyback program. Outstanding shares have halved from 651 million shares to just 294 million shares in the past five years due to buybacks. That’s a remarkable decline and better than 99.1% of the whole oil industry. 13.4% of shares have been bought back annually in the past three years on average, and that’s on top of a 1.66% dividend yield.

The widened margins as a result of higher oil prices will allow even more buybacks in the future, and I expect MPC stock to keep rallying.