A publicly traded business development company, Monroe Capital Corporation (NASDAQ:MRCC), just declared a $0.75 special pre-merger distribution, and on the surface, that looks generous. However, the data tells a more complicated story about what shareholders are actually receiving and what comes next.

How MRCC Generated Its Income

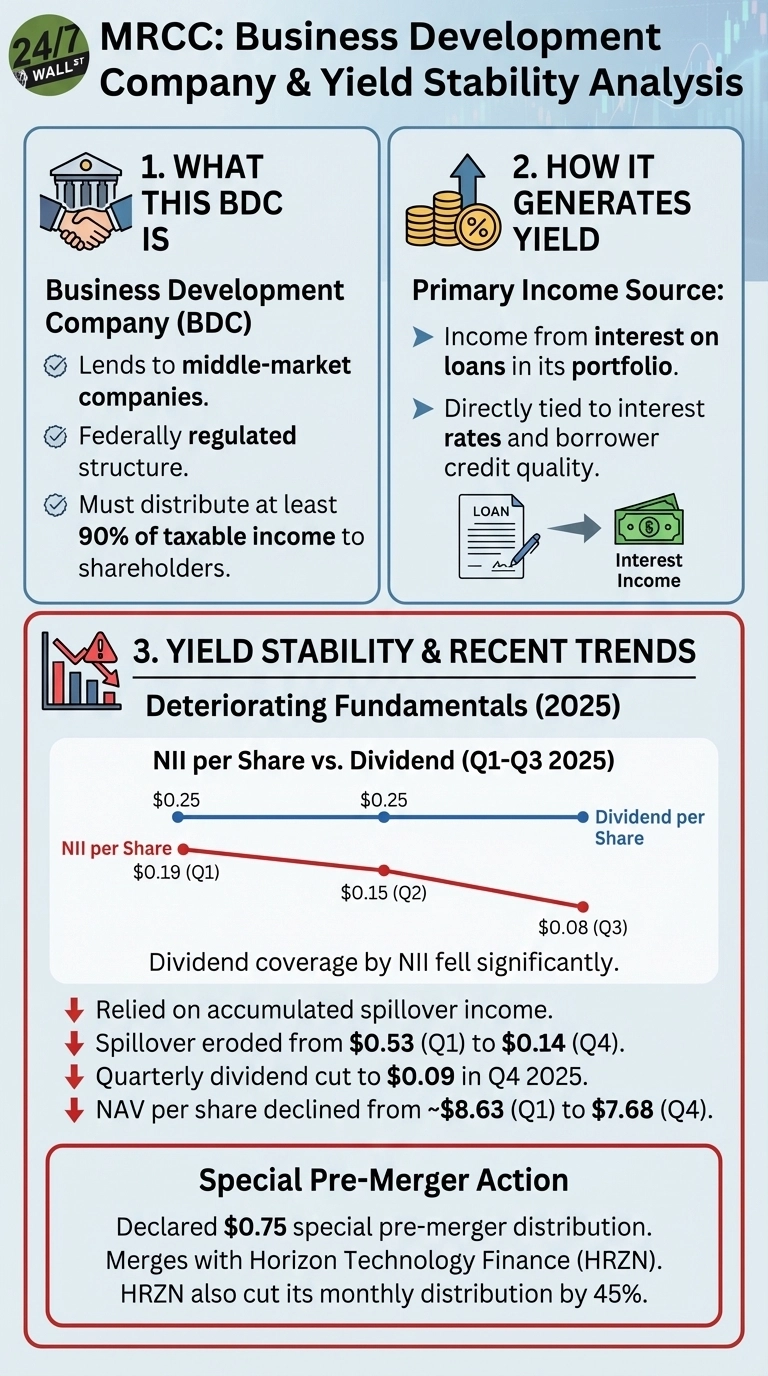

MRCC is a federally regulated structure that lends to middle-market companies and must distribute at least 90% of its taxable income to shareholders. Income comes from interest on loans in its portfolio. The challenge is that this income is directly tied to interest rates and borrower credit quality. When rates fall or loans go bad, net investment income shrinks, and the dividend becomes harder to sustain.

That is exactly what happened through 2025 as the company announced that net investment income per share fell from $0.19 in Q1 2025 to just $0.08 in Q3 2025, while the quarterly dividend stayed at $0.25. The good news is that management plugged the gap with accumulated spillover income, a reserve of previously undistributed earnings, while the reserve itself eroded from $0.53 per share in Q1 2025 to $0.14 per share by Q4 2025.

The Dividend Was Already on Life Support

By Q4 2025, management acknowledged the math. The quarterly dividend was cut to $0.09 per share, down from $0.25, with CEO Theodore Koenig citing “the decrease in base rates” as a key driver. The Fed cut rates in late 2025, bringing the federal funds rate to 3.75%, compressing the spread between what MRCC earns on its loans and what it pays to borrow.

Portfolio quality was also deteriorating. Non-accruals, loans where borrowers have stopped making payments, rose from 3.4% in Q1 2025 to 4.0% by Q4 2025. The average portfolio mark fell to 89.7% of amortized cost, meaning the portfolio is worth less than what was originally lent out.

The $0.75 in Context

The special distribution is real cash, funded by $0.14 per share of remaining spillover income and merger-related asset liquidation proceeds. But framing it as a value unlock requires scrutiny. MRCC shares are down 26% year-to-date, and the stock currently trades at around $4.71 per share, versus a book value of $7.68. The $0.75 distribution helps narrow that gap but does not close it.

What Shareholders Are Converting Into

The NAV-for-NAV merger with Horizon Technology Finance (NASDAQ:HRZN) means MRCC shareholders receive HRZN shares at equivalent NAV. The problem is that HRZN has its own headwinds. Its NAV dropped from $8.43 at year-end 2024 to $6.98 by Q4 2025, and the company just cut its monthly distribution by 45%, from $0.11 to $0.06. HRZN shares have reflected this deterioration, falling 33% year-to-date as investors price in the weaker income outlook.

HRZN CEO Mike Balkin said the reduced distribution “aligns our distribution level with our anticipated NII and operating results for 2026, taking into account the expected impact of the anticipated merger with MRCC.” That is, management acknowledges that the combined entity cannot sustain the prior income level in the near term.

Value Gift or Fire Sale?

The $0.75 distribution is a genuine return of capital, but it is the last act of a BDC that spent most of 2025 paying dividends it could not fully earn, watching its NAV erode, and managing rising credit stress. Shareholders collecting that check are simultaneously converting into HRZN at a moment when HRZN itself is cutting income and absorbing its own portfolio pressures.

For income investors, the post-merger dividend picture is materially weaker than what MRCC offered even a year ago. The combined entity has cited scale and capital base as strategic rationale for the merger, though near-term income will be lower. HRZN’s ability to deploy capital at yields that support distribution recovery is the central question for income investors evaluating the combined entity following the merger’s close.