Wall Street has gotten far more selective on AI stocks, but these AI stocks are still receiving the lion’s share of invested capital. Dividend Aristocrat stocks like PepsiCo (NASDAQ:PEP | PEP Price Prediction), Hormel Foods (NYSE:HRL), and Beckton Dickinson (NYSE:BDX) are neglected, and that’s exactly why it’s worth chasing them right now.

A portion of investors have already started rotating their capital into these dividend stocks. If you think the AI rally could start fading more on the heels of a global slowdown, these dividend stocks will end up being your best friend. They provide a healthy dividend yield you can reinvest to snowball your portfolio. Plus, you get healthy upside potential on top.

Some of these Dividend Aristocrats are beaten down to the point where their upside potential now rivals these AI stocks when you factor in the prospect of recovery.

Let’s take a look.

PepsiCo (PEP)

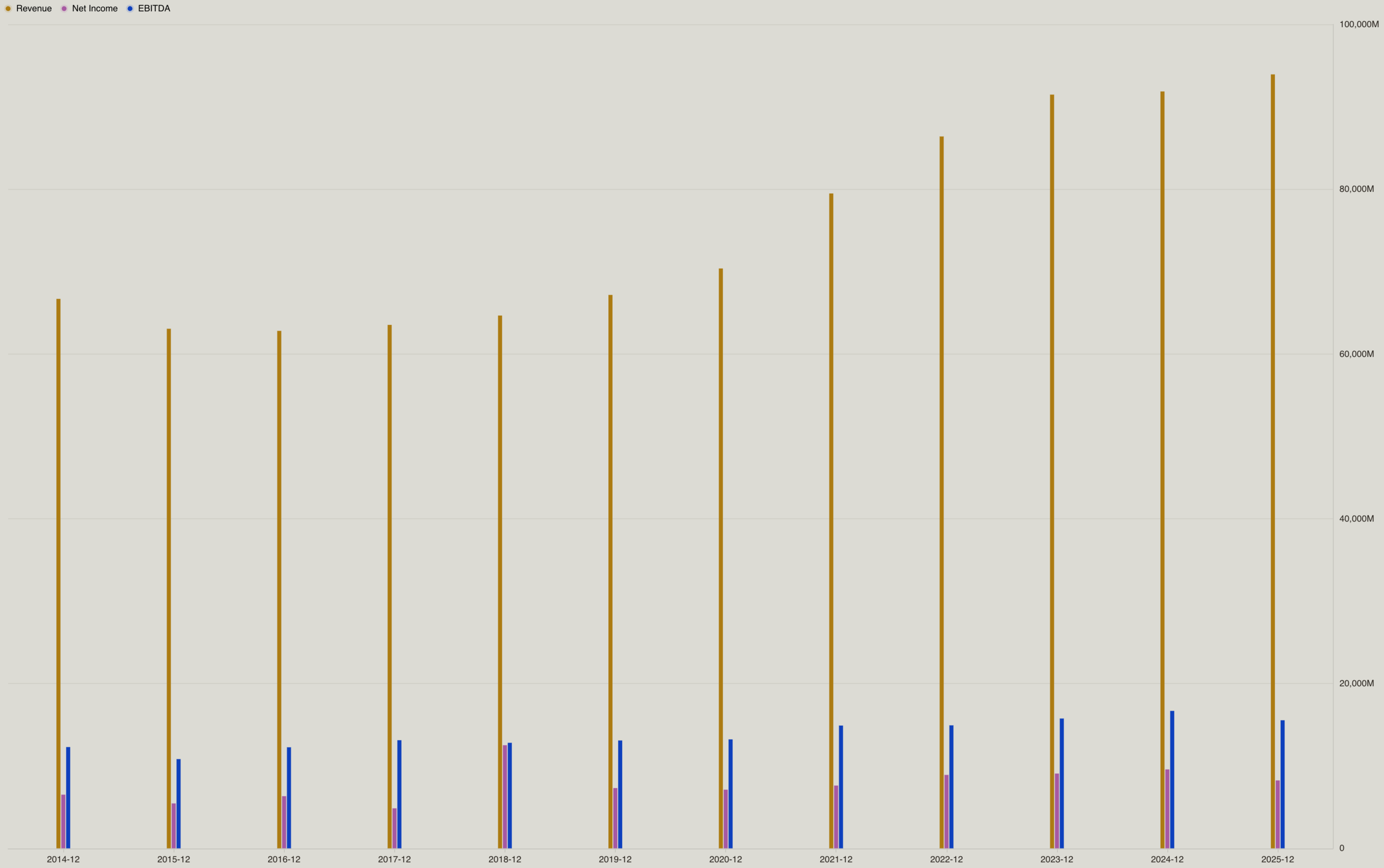

PepsiCo has taken a beating since mid-2023 for various reasons, with the most prominent one being GLP-1 drugs. That said, I do not think these weight loss drugs were enough to throw off its entire customer base. This company dominates snack aisles, and the pullback in the stock market was a product of a revenue growth slowdown, not a decline like many on Wall Street would make you believe.

The market simply believed that the growth trajectory from 2020 to 2022 would stick. When that didn’t appear to be the case, the Street quickly discounted the stock, and in doing so, took things too far.

PEP stock now sits at just 17 times forward earnings, which is very low for a dependable Dividend Aristocrat stock. In the 2010s, PepsiCo had far lower growth rates and was struggling to grow its sales, but the stock still kept rising. I expect the current slump to be temporary, with PEP stock making a full recovery within the next 24 months.

The biggest catalyst that could re-rate PEP stock upward would be lower Treasury yields. PEP stock has a dividend yield at 3.75%, which is just shy of T-Notes and T-Bonds. Treasuries don’t come with the upside potential or the inflation hedge either. Hence, I see massive inflows into PEP stock even if T-note yields come down to 3%.

PepsiCo is a Dividend King with 53 years of consecutive dividend growth.

Hormel Foods (HRL)

HRL stock is down by over 52% in the past five years and has brutally underperformed the market. This is one of the most recognizable branded food companies, but it was hit with the same issues PepsiCo has been dealing with. The difference is that it’s worse with Hormel Foods.

The inflation surge caused higher input costs for the business, and customers weren’t eager to buy at elevated prices. This caused net income to plunge from $1 billion in 2022 to $478 million in 2025, even though revenue has remained stable at $12 billion.

Management also made a significant blunder by acquiring the Planters snack nut portfolio for $3.35 billion in 2021. This one acquisition ruined the balance sheet. In 2020, cash was at $1.73 billion, with $1.3 billion of debt, and post-acquisition, cash was just $635 million, with $3.3 billion of debt. Oh, and the Federal Reserve embarked on record interest rate hikes just a few months later.

This saga is still costing the company dearly, with net interest losses at $54 mllion last fiscal year.

I do see a silver lining in all this. The bad has already been priced into the stock, and a recovery is yet to be priced in. Hormel’s turnaround hinges on pricing finally catching up to input costs, commodity relief in the back half of 2026, and portfolio pruning that sheds low-margin businesses like whole-bird turkey.

I believe HRL stock has likely bottomed out, with a floor price at $22. You get a 5.22% dividend yield with significant long-term upside at just 15 times forward earnings. HRL stock is too cheap to ignore.

Becton Dickinson (BDX)

Beckton Dickinson traded sideways from 2018 to 2025 before plunging by 20%, and it has yet to recover. BDX lost ground not because of any single crisis, but because China, research funding, tariffs, and a leadership shake-up arrived in near-sequential waves that gave bulls little time to regroup.

Tariff chaos and budget cuts are now behind us, and analysts expect both EPS and revenue to start recovering from FY2027 onwards. The recovery is likely to be drawn out, but it’s worth buying into due to how cheap the stock is. You’re paying just 12 times forward earnings for a Dividend King with 53 consecutive years of dividend growth. The payout ratio is just 30%, so the 2.69% dividend yield has plenty of room to keep growing before it hits the ceiling.

When you factor out non-recurring expenses, you’re paying just 11 times earnings. Historically, BDX has traded at 21 times earnings minus non-recurring items. That leaves tremendous room for upside when things finally normalize.