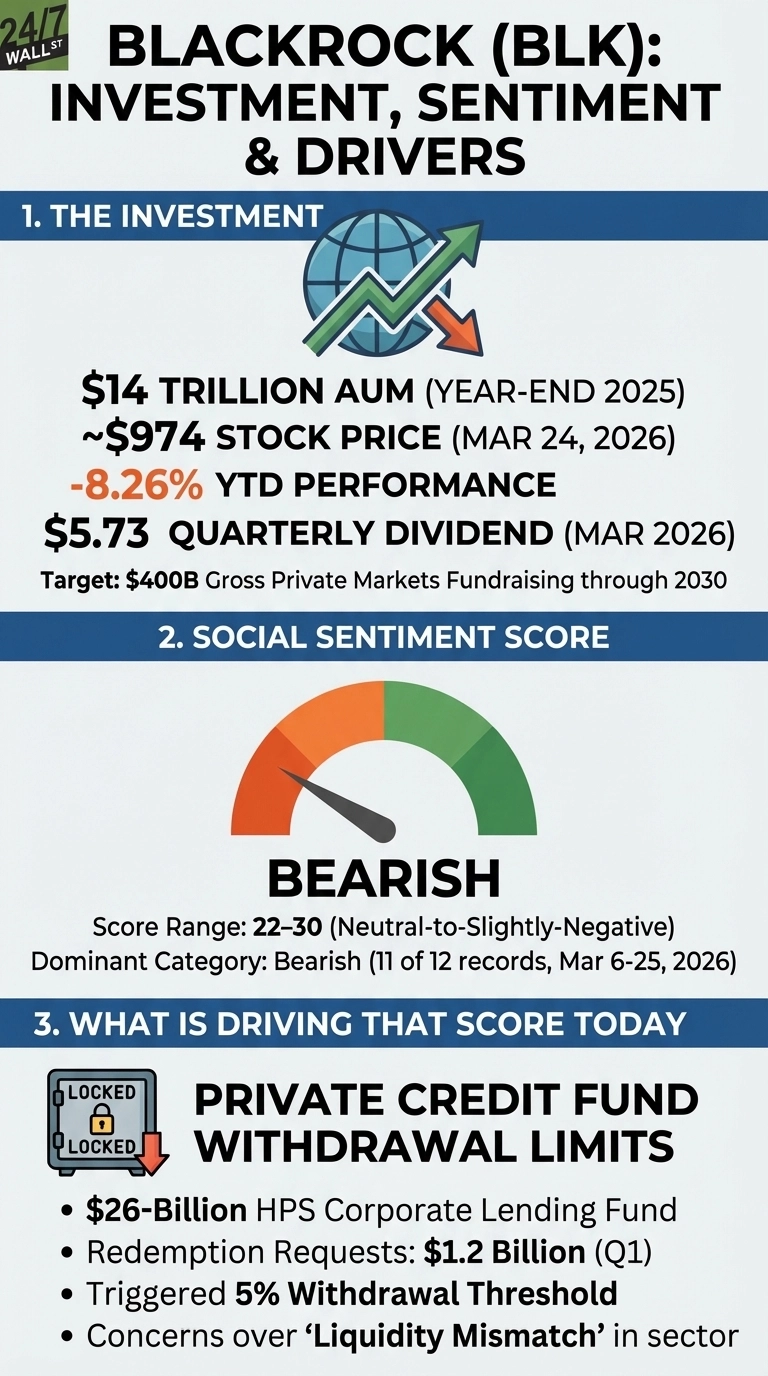

The world’s largest asset manager, BlackRock (NYSE:BLK) crossed $14 trillion in AUM at year-end 2025, raised its quarterly dividend to $5.73 per share, and is targeting $400 billion in gross private markets fundraising through 2030. By almost every operational measure, BlackRock is executing, but it’s not all positive as shares are down about 8.9% year-to-date, trading near $974, and Reddit’s investor communities have turned bearish. The gap between business performance and social sentiment tells a specific story.

A Private Credit Stumble Drives the Bearish Turn

The sentiment shift traces to one event, which took place on March 6, 2026, when BlackRock disclosed it had placed withdrawal limits on its flagship private credit fund after receiving redemption requests totaling $1.2 billion in the first quarter, roughly 9.3% of the fund’s net asset value. The firm paid out $620 million, hitting the 5% redemption threshold that triggers restrictions on further withdrawals.

The post by u/BusyHands_ on r/stocks captured the reaction immediately, accumulating 1,497 upvotes and 200 comments at peak:

BlackRock limits withdrawals from private credit fund after surge in redemption requests

by u/BusyHands_ in r/stocks

The post noted that “redemption requests faced by some of the biggest players in the market reflect the liquidity mismatch in the sector, where investor money is often tied up in assets that cannot be sold immediately.” That framing landed hard with retail investors already anxious about private credit exposure.

Three Concerns Driving the Skepticism

Sentiment has held at 22 to 30 on a 0-to-100 scale across 11 of 12 recorded sessions since early March, concentrated in r/stocks and r/investing. Three concrete concerns dominate the discussion:

- BlackRock’s $26-billion HPS Corporate Lending Fund hit its redemption cap, raising questions about liquidity risk in the private credit strategy that cost $12 billion to acquire.

- Peers face the same pressure: Blackstone lifted its redemption limit from 5% to 7% and injected $400 million to cover requests, while Blue Owl replaced redemptions with promised payouts.

- BlackRock trades at a forward P/E of 18x versus the investment management industry average of 10x, leaving little room for missteps on the private markets buildout.

The Underlying Business Still Delivered

The bearish tone sits in tension with what BlackRock actually produced in 2025: full-year revenue reached $24 billion, up 19% year-over-year, and EPS was $48.09, up 10%. Organic base fee growth accelerated from 1% at the start of 2024 to 12% in Q4 2025, and the iShares ETF platform pulled in $527 billion in net inflows for the year. CEO Larry Fink addressed the turbulence directly: “Uncertainty and anxiety about the future of markets and the economy are dominating client conversations. We’ve seen periods like this before… and some of BlackRock’s biggest leaps in growth followed.” Analysts have a consensus price target of around $1,320, compared with the current price of $974. The private credit redemption story is real, and it reflects a sector-wide liquidity issue that has hit Blackstone and Blue Owl as well.

Data Sources

- BlackRock Q4 2025 earnings call transcript via Alpha Vantage: AUM milestone, organic base fee growth trajectory, private markets fundraising targets, and CEO commentary.

- BlackRock Q1 2025 earnings data via Fuse API: Revenue, EPS, iShares inflows, and technology services growth.

- Reddit sentiment data via Fuse API: Sentiment scores, activity levels, subreddit breakdown, and post engagement for March 2026.

- The Globe and Mail: HPS Corporate Lending Fund withdrawal restrictions, redemption figures, and competitive context.