Palo Alto Networks (NASDAQ:PANW | PANW Price Prediction | PANW Price Prediction) CEO Nikesh Arora published an op-ed on March 30, 2026, titled “Weaponized Intelligence” that cuts to the heart of where cybersecurity is heading. His core argument: “AI must fight AI.” Arora contends that AI-powered tools are making sophisticated cyberattacks accessible to many, eroding the defender’s advantage, and that the industry’s only viable response is to integrate AI models into defensive solutions while consolidating fragmented security tools.

The op-ed arrived three days after Arora made that argument tangible in the most direct way possible: an open-market stock purchase, his first since November 2019.

$10 Million at the Low

On March 27, 2026, Arora filed a Form 4 disclosing the purchase of 68,085 shares at prices ranging from $146.874 to $147.48 per share, totaling approximately $9,999,977. The transaction increased his direct holdings by 24.73% to 343,394 shares, bringing his total Palo Alto stake to approximately $162 million at the time of purchase.

The timing was deliberate. The purchase came immediately after a sectorwide sell-off triggered by a leaked draft post about Anthropic’s new AI model “Claude Mythos,” which raised competitive concerns about AI replacing traditional cybersecurity firms. Palo Alto Networks shares fell 6% on those fears. At the time of purchase, the stock was down roughly 20% year-to-date and near its 52-week low of $139.57.

Bernstein analyst Peter Weed pushed back on the panic, stating “Anthropic is not entering the cybersecurity software market and Mythos is designed to make AI models harder for hackers to exploit, not replace cybersecurity firms.” JPMorgan’s Brian Essex struck a similar tone, calling Arora’s purchase a “substantial vote of confidence” and arguing that the stock’s sell-off had moved beyond reason. Arora’s op-ed made the same case from the inside. It was not the first time he acted this way either: in February 2024, Arora bought $10.6 million of Palo Alto stock after a guidance cut sent shares plummeting 28%, underscoring a consistent pattern of putting personal capital behind his public conviction.

The Financials Behind the Conviction

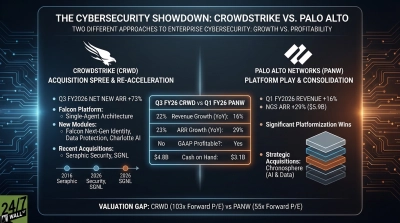

Arora’s purchase aligns with a business that had been executing consistently. In Q2 FY2026, Palo Alto Networks posted $2.594 billion in revenue, up 14.9% year over year, beating estimates. Non-GAAP EPS came in at $1.03, topping the $0.9389 consensus by 9.7%. Non-GAAP operating margin held at 30.3%, the third consecutive quarter above 30%.

Next-Generation Security annual recurring revenue (ARR) reached $6.30 billion, up 33% year over year. That metric sits at the center of Arora’s platformization and AI security thesis. At the time of the op-ed, full-year guidance called for revenue of $11.28 billion to $11.31 billion and NGS ARR of $8.52 to $8.62 billion, representing 53% to 54% growth.

Arora framed the AI tailwind directly on the Q2 call: “We saw continued strength in platformizations, a trend that is accelerating due to AI. Customers are keen to both modernize and normalize their cybersecurity stack, aligning them to our approach.”

Market Response and Subsequent Validation

The stock surged over 8% on March 30, the same day the op-ed published. The months that followed confirmed the business case Arora had staked his own money on. In Q3 FY2026, reported on June 2, 2026, Palo Alto Networks delivered revenue of $3.0 billion, up 31% year over year, including $388 million from the recently completed CyberArk and Chronosphere acquisitions. NGS ARR hit $8.13 billion, a 60% year-over-year surge that blew past the upper end of guidance. Non-GAAP EPS came in at $0.85, beating the $0.80 consensus. The company simultaneously raised its full-year revenue outlook to $11.42 billion to $11.43 billion.

The analyst community responded in kind. The consensus price target, which stood near $207 at the time Arora made his purchase, climbed to approximately $306 across more than 50 analysts polled by S&P Global following the Q3 print, carrying a Buy rating. Arora’s $147 entry price now sits well below both the revised targets and where shares had recovered to by early June 2026.

Editor’s note: This article has been updated to include Palo Alto Networks’ Q3 FY2026 results (revenue of $3.0 billion, NGS ARR of $8.13 billion, and raised full-year guidance), the JPMorgan analyst commentary on Arora’s purchase, the historical precedent of Arora’s February 2024 insider buy, and the current analyst consensus price target of approximately $306, up significantly from the $207 figure that prevailed when the original article was published.

Contact [email protected] for any questions or corrections.