Oppenheimer analyst Ittai Kidron raised his price target on Palo Alto Networks (NASDAQ:PANW | PANW Price Prediction) to $275 from $245 on May 15, reiterating an Outperform rating. The price target raise followed Oppenheimer’s attendance at CyberArk’s Impact 2026 customer conference, where Palo Alto unveiled the rebrand of CyberArk to “Idira.” For investors, the call crystallizes a clearer identity security thesis baked into Palo Alto Networks stock.

The rebrand signals more than a name change. By folding CyberArk into a unified identity security platform, Palo Alto is staking its claim on agentic identity — the fast-emerging category where AI agents require fine-grained access controls that legacy perimeter tools weren’t built to handle. Oppenheimer’s checks with customers at the event suggest demand is real and pipelines are building.

That backdrop frames why the Street-high $275 target carries weight, and why investors are reassessing how identity fits into the broader platform consolidation thesis underpinning PANW shares.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| PANW | Palo Alto Networks | Oppenheimer | Price Target Raise | Outperform | Outperform | $245 | $275 |

The Analyst’s Case

Kidron’s thesis centers on the Idira launch. The rebranded CyberArk platform will integrate with Strata, Cortex, and Prisma AIRS, delivering first-party identity detection and dynamic fine-grained privilege controls to humans, machines, and AI Agents.

Oppenheimer’s customer survey at the event showed uninterrupted renewal activity and strong spending expectations, with all respondents positive or indifferent on the Palo acquisition and no churn signals. That’s a clean read-through for Palo Alto Networks stock.

Company Snapshot

Palo Alto Networks is the platform consolidator of choice in cybersecurity, with brands spanning Unit 42, Cortex XSIAM, AgentiX, and now Idira. Q2 FY2026 revenue rose 15% year over year (YoY) to $2.59 billion, with Next-Generation Security ARR up 33% to $6.3 billion.

CEO Nikesh Arora noted that “customers are keen to both modernize and normalize their cybersecurity stack.” Updated FY2026 guidance now calls for revenue of $11.28 billion to $11.31 billion, reflecting acquisition-driven acceleration.

Why the Move Matters Now

PANW stock trades at $239, up 30% year to date (YTD) and 46% over the past month. The forward P/E ratio of 52x isn’t cheap, and the consensus analyst target sits at $207.56, making Oppenheimer’s $275 a Street-high call.

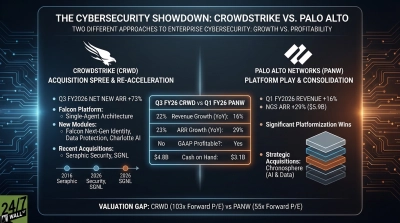

The competitive backdrop matters. CrowdStrike (NASDAQ:CRWD) shares have climbed 43% over the past month on the same platform consolidation tailwind, while Okta (NASDAQ:OKTA) stock remains down 6% YTD as identity incumbents face new pressure.

The Idira move plants Palo Alto’s flag in agentic identity, where AI agents need fine-grained access controls that traditional perimeters don’t address.

What It Means for Your Portfolio

For prudent investors, the Oppenheimer analyst upgrade reinforces a clear platform consolidation narrative. The bull case rests on identity security demand plus expanding NGS ARR; the bear case includes premium valuation, CyberArk integration risk, and competitive pressure from CrowdStrike.

Palo Alto Networks stock could continue rerating if Idira’s cross-platform integration converts existing CyberArk customers into broader platform buyers. Position sizing should respect the multiple, and watch for whether the Q3 FY2026 results confirm the 28% to 29% revenue growth guidance.

Contact [email protected] for any questions or corrections.