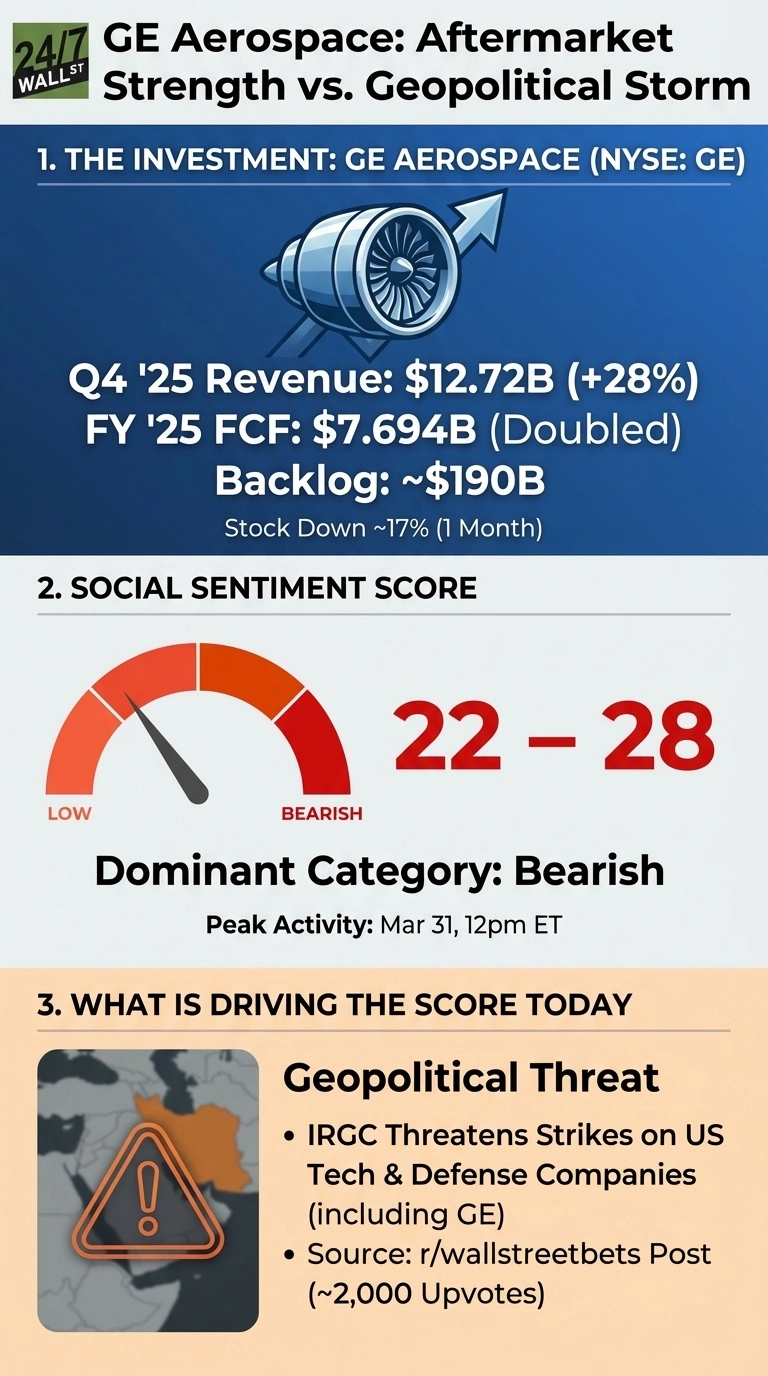

Still a giant in its field, GE Aerospace (NYSE:GE | GE Price Prediction) shares are down nearly 14% over the past month and nearly 5% year to date, even as the business posts some of its strongest results in years. Reddit sentiment on GE sits at 22 to 28, firmly bearish, driven not by earnings disappointment but by a geopolitical threat that landed GE on an unwelcome list. The stock recovered about 4% on April 1, trading near $295, but the one-month drawdown reflects how quickly macro risk can overshadow fundamental strength.

The business itself tells a different story as Q4 2025 revenue came in at $12.72 billion, well ahead of estimates, while full-year free cash flow doubled to $7.694 billion. GE Aerospace’s $190 billion backlog and 2026 EPS guidance of $7.10 to $7.40 suggest the aftermarket engine is still running hot.

IRGC Threat Pulls GE Into a Geopolitical Storm

The catalyst for the bearish Reddit spike was a post by u/Playwithuh in r/wallstreetbets that accumulated nearly 2,000 upvotes and 323 comments:

IRGC threatens strikes on US tech giants across the Middle East

by u/Playwithuh in r/wallstreetbets

“The Islamic Revolutionary Guard Corps (IRGC) has threatened to strike 18 US technology and defense-related companies operating in the Middle East… The IRGC named companies including Cisco, HP, Intel, Oracle, Microsoft, Apple, Google, Meta, IBM, Dell, Nvidia, Tesla, GE, JPMorgan, and Boeing, among others, as potential targets.” The same post appeared in r/stocks, generating 673 upvotes and 166 comments. Peak activity hit on Tuesday, March 31 at noon ET, with 1,549 upvotes and 422 comments across subreddits in a single hour.

Aftermarket Strength Meets a Skeptical Reddit

The dominant sentiment category is bearish, with scores clustering between 22 and 28 across r/wallstreetbets, r/stocks, and r/investing. The geopolitical noise is crowding out an otherwise constructive fundamental picture. Three reasons the skepticism has traction:

- CES margins compressed 420 basis points in Q4 from a lower spare engine ratio and higher install deliveries, raising questions about whether services’ profitability can hold as equipment mix shifts.

- GE Aerospace trades at a forward P/E of 44x, a steep premium that leaves little room for execution misses or macro shocks.

- Supply chain constraints remain an active risk, even as priority supplier material input rose more than 40% in 2025.

Capital Returns Signal Confidence

GE Aerospace raised its quarterly dividend to $0.47 in Q1 2026, up from $0.36 throughout 2025 and well above the $0.01 paid during the 2019 to 2020 distressed period. The $24 billion capital return program running through 2026, along with a target to return at least 70% of free cash flow beyond 2026, reflects management’s confidence in cash generation. With 17 of 19 analysts rating GE a buy or strong buy and a consensus target near $362, the Wall Street view diverges sharply from Reddit’s current mood. The geopolitical threat represents a near-term risk. The aftermarket services cycle remains the longer-term driver of the investment case.