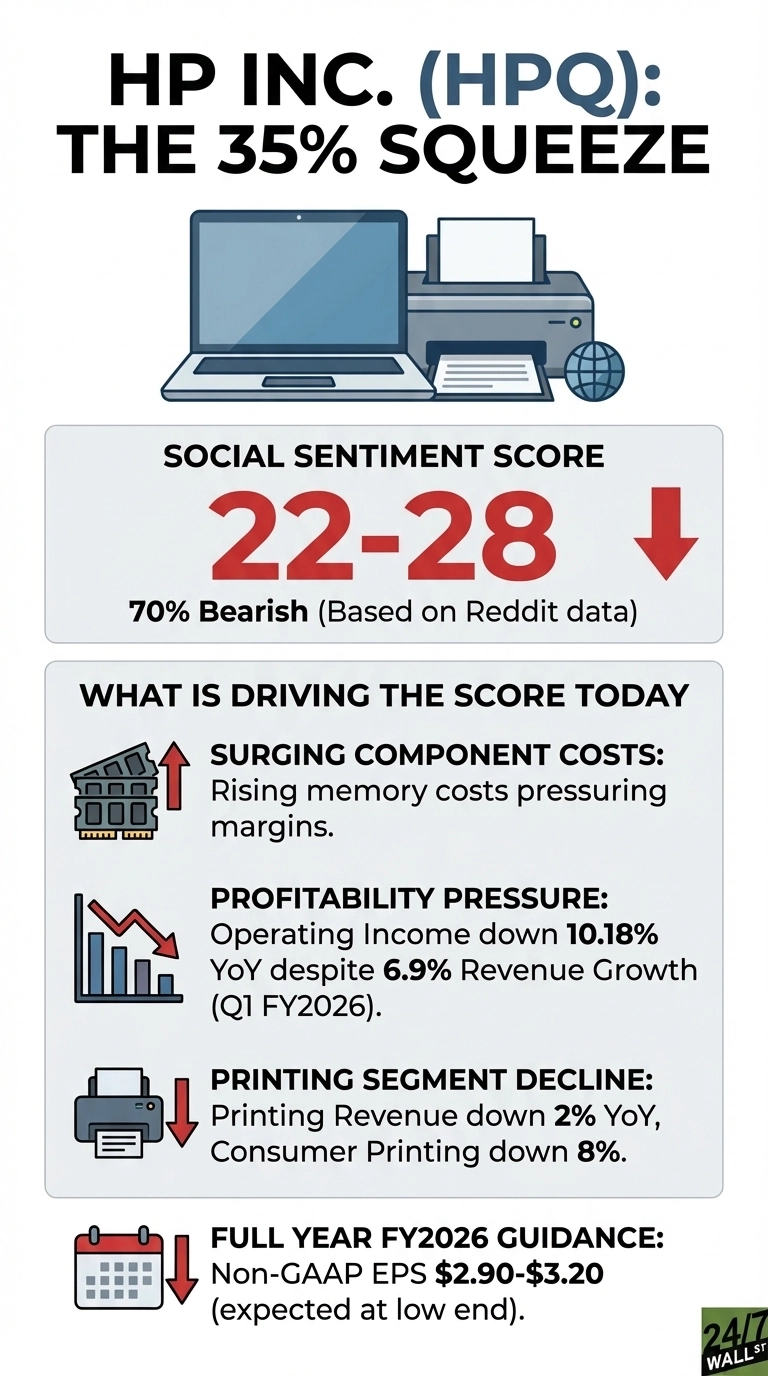

HP Inc (NYSE:HPQ | HPQ Price Prediction) beat Q1 FY2026 estimates on both the top and bottom lines, yet shares have lost 31% over the past year and trade near their 52-week low of $17.56. Meanwhile, Reddit sentiment scores have settled in the 22-28 range, with 70% of records classified as bearish. AI PC momentum is real, but memory costs are absorbing the gains.

HP posted Q1 revenue of $14.44 billion, up 6.9% year over year, and non-GAAP EPS of $0.81 against a $0.77 estimate. Personal Systems revenue rose 11% to $10.25 billion, with AI PCs now accounting for more than 35% of total PC shipments. Gross profit was essentially flat, down 0.18% year over year, and operating income fell 10.18% despite that revenue growth. Management guided full-year non-GAAP EPS to the low end of $2.90 to $3.20 and flagged a double-digit decline in PC unit shipments for 2026.

Reddit’s Read on HP’s Memory Cost Problem

Discussion across r/wallstreetbets, r/investing, and r/stocks picked up sharply around the earnings release, with the peak engagement window logging 1,539 upvotes and 418 comments. Users are not dismissing the AI PC story but are focused on whether HP can translate unit growth into margin recovery while memory prices stay elevated. A thread in r/technology captured the concern, with one commenter noting: “It means your RAM is less stringently quality tested, which is bad. They also reduced shipping costs, which is good. I call it frogurt.”

RAM now represents 35 percent of bill of materials for HP…

by u/Gioware in r/technology

The bearish case centers on three issues:

- HP’s finance chief warned that memory cost volatility is expected to persist even into next year, with no near-term relief for a cost that now dominates the bill of materials.

- Printing revenue fell 2% year over year in Q1, with consumer printing down 8%, removing a historically stable margin contributor.

- Management guided PC unit shipments to a double-digit percentage decline for 2026, meaning AI PC mix gains must offset both volume pressure and cost inflation simultaneously.

HP at $19: What the Numbers Actually Say

As it stands today, HP trades at a trailing P/E of 7x and yields roughly 6.3%, with insider activity trending toward net buying across 14 recent transactions. Analysts are split: 3 buys, 8 holds, and 3 underperforms, with a consensus target near $19.43. Dell (NYSE:DELL) faces the same memory cost headwinds and AI PC transition dynamics, framing the margin pressure as an industry-wide constraint. Q2 FY2026 results will be the next test, with HP guiding non-GAAP EPS of $0.70 to $0.76, a sequential step down from Q1.

Contact [email protected] for any questions or corrections.