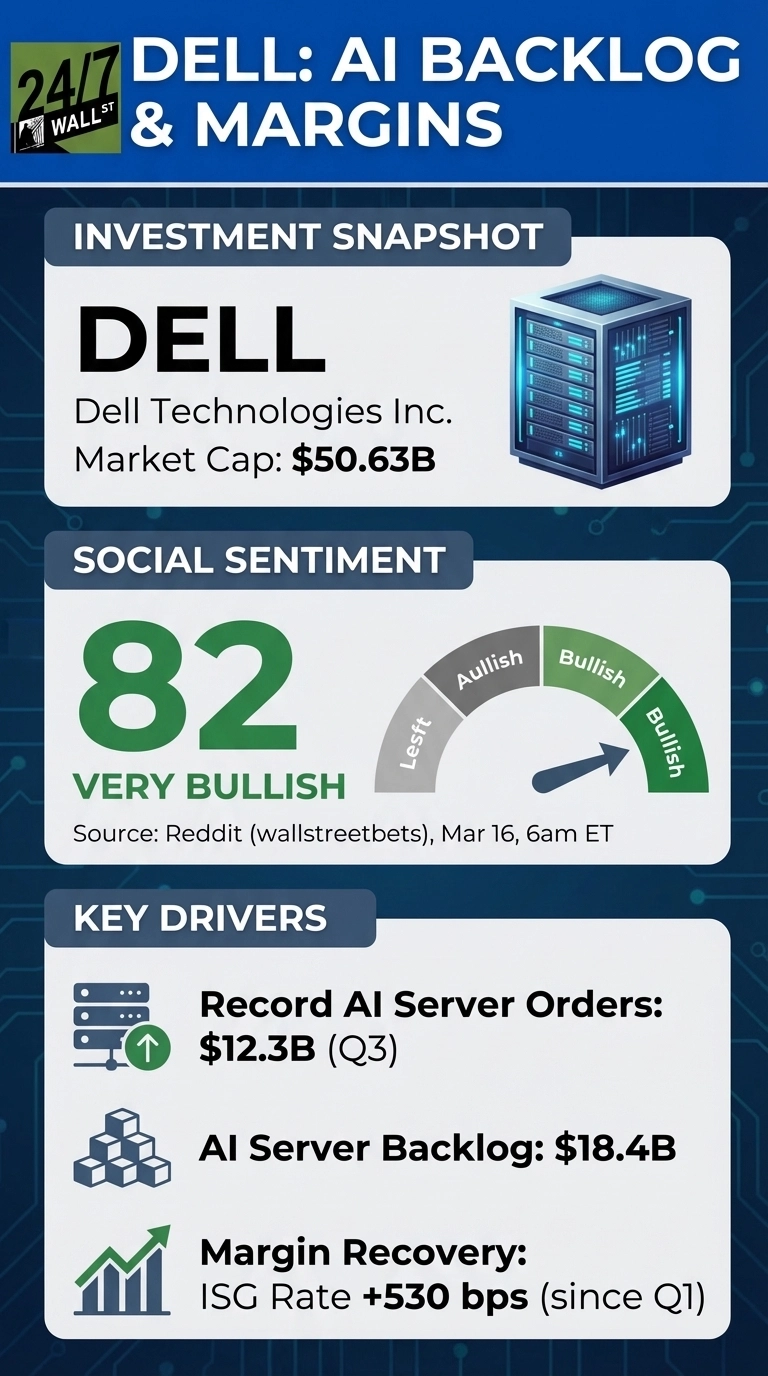

It might not be the computing giant it once was, but Dell Technologies (NYSE:DELL | DELL Price Prediction) had a Q4 earnings beat that settled a debate retail investors had been running for weeks: whether a record AI server backlog would translate into real profit.

When it comes to detailed performance numbers, Dell’s Q4 FY2026 results, reported February 26, delivered a clean beat: it saw Q4 revenue of $33.4 billion, well ahead of the roughly $31.6 billion consensus, with non-GAAP EPS of $3.89 against an estimate of around $3.51. Full-year FY2026 revenue came in at $113.5 billion. FY2027 guidance projects $140 billion in revenue at the midpoint, with AI-optimized server revenue expected to roughly double to ~$50 billion. Dell also raised its quarterly dividend 20% to $2.52 per share and expanded its share repurchase authorization by $10 billion.

Before earnings, r/stocks hosted an analytical thread: “Dell reports tomorrow with an $18.4B AI server backlog and a margin story that finally started recovering.”

Dell reports tomorrow with an $18.4B AI server backlog and a margin story that finally started recovering

by u/corenellius in stocks

“My read is the recovery is real but fragile. If margins hold at 12%+ while shipping $9.4B in AI servers, the bull case gets a lot stronger.” After the print, r/wallstreetbets responded with “Why no one posted DELL gains?”. One commenter wrote: “Finally, DELL doing what it was supposed to do.”

Why no one posted DELL gains?

by u/Agmikai in wallstreetbets

Three reasons retail investors are bullish:

- Dell entered FY2027 with a record $43 billion AI server backlog, providing strong near-term revenue visibility

- ISG operating income improved 530 basis points since Q1 through the fiscal year, showing margins moving in the right direction despite AI server mix pressure

- The 20% dividend hike to $2.52/year and $10 billion buyback expansion signal management confidence in cash generation

Of course, the skepticism is real, too, as Morgan Stanley raised its price target to $110 while keeping an Underweight rating, citing difficulty projecting simultaneous gains in pricing, demand, and margins during a significant memory cycle. The concern: AI-optimized server revenue carries dilutive gross margin rates even as margin dollars grow.

Dell CEO Jeff Clarke has acknowledged the dilutive rate for multiple consecutive quarters while arguing that it is improving. HPE also flagged that memory shortages are expected to persist through 2027, a component that Dell relies on heavily in high-density AI server configurations.

Something investors should watch for is ISG’s operating margin in Q1 FY2027. If Dell sustains rates above 13% while shipping into a $43 billion backlog, the margin recovery story becomes structural. However, if memory costs compress it back toward single digits, the WSB celebration may prove premature.

Contact [email protected] for any questions or corrections.