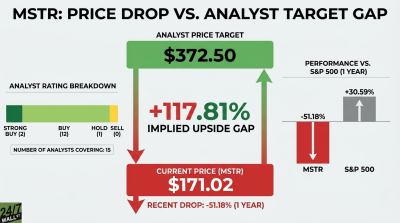

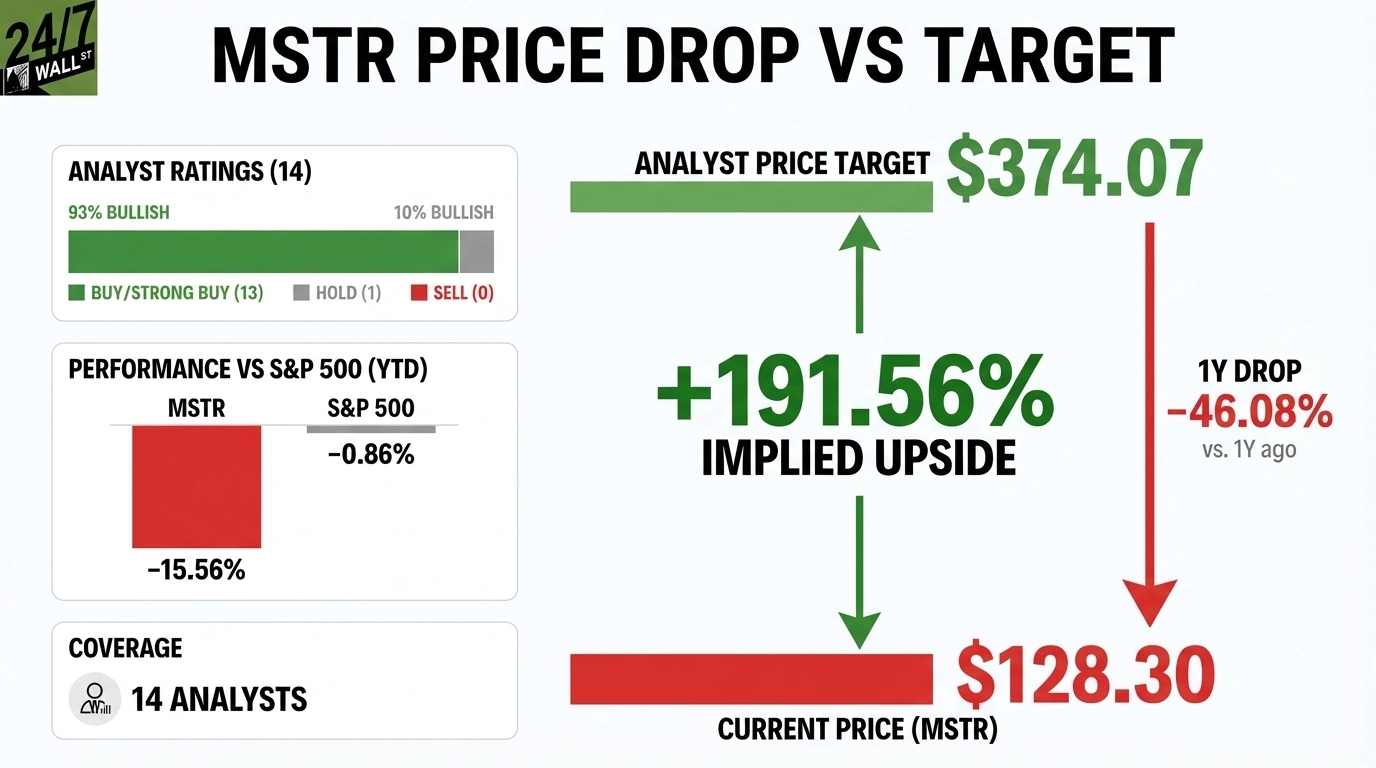

Strategy (NASDAQ:MSTR | MSTR Price Prediction), formerly known as MicroStrategy, currently trades at $128.30, while the Wall Street consensus price target sits at $374.07, implying upside of 191.56% from current levels. That gap reflects a fundamental disagreement about what this company is worth.

Strategy is a leveraged bitcoin treasury vehicle that runs a legacy analytics business on the side. The company holds 713,502 BTC with a cost basis of approximately $54.26 billion, and every quarterly result is essentially a function of where bitcoin traded during those 90 days. That makes the analyst-versus-market disconnect unusually sharp, because the two sides are disagreeing on the trajectory of bitcoin itself.

MSTR Stock Has Fallen 46% in One Year While Bitcoin Barely Moved

Bitcoin fell, and Strategy is leveraged to bitcoin. Bitcoin is down 17.83% year-to-date and 5.71% over the past year, but MSTR has amplified those losses significantly due to its leveraged structure. The stock is down 46.08% over the past year and down 15.56% year-to-date.

The Q4 2025 earnings report intensified the selloff. Strategy posted a net loss of $12.44 billion, or $42.93 per diluted share, against an analyst estimate of negative $15.66 per share. That is a -174.14% earnings surprise, driven almost entirely by a $17.44 billion unrealized loss on digital assets under the new ASU 2023-08 fair value accounting standard. The operating loss for the quarter reached $17.45 billion. These are largely non-cash accounting entries tied to bitcoin’s price at quarter-end.

Retail sentiment around earnings was brutal. A post on r/wallstreetbets framing MSTR as a “generational wealth opportunity” short generated high engagement. More recently, sentiment has stabilized in bearish territory, hovering around 28 to 30. The prediction market composite sentiment index currently sits at 39.1, rated bearish.

Why 13 Analysts Still Have Buy Ratings

To understand why a meaningful group of analysts remains bullish, you have to look at how the model actually works. The core mechanism for Strategy is Bitcoin Per Share, or BPS. Strategy’s capital markets machine raised $25.3 billion in FY2025, making it the largest U.S. equity issuer for a second consecutive year, and used those proceeds to buy more bitcoin. The company achieved a 22.8% BTC Yield in FY2025, meaning the amount of bitcoin backing each share grew by that amount even after accounting for dilution from share issuance. Bulls argue that as long as BPS is growing and bitcoin is rising, the dilution from ATM programs is accretive rather than destructive.

Remaining capital capacity is another key piece of the story. As of early 2026, Strategy still had over $37 billion of capacity across its ATM programs, including $8.1 billion in common stock and more than $29 billion in preferred issuance. Prediction markets reflect that expectation, assigning a 96.6% probability that the company will hold at least 800,000 BTC by the end of 2026 and a 98.2% probability of a bitcoin purchase announcement in the current week alone.

At the same time, Strategy’s preferred stock platform, led by STRC with a $3.4 billion aggregate stated amount and an 11.25% variable dividend rate, gives the company a flexible and increasingly differentiated financing structure. Prediction markets assign just a 9% probability of a margin call in 2026, reinforcing the view that the balance sheet can support the bitcoin accumulation strategy.

A 191% Gap Between Price and Target

MSTR trades at $128.30 against a consensus analyst target of $374.07, implying upside of 191.56%. The stock’s 52-week high is $457.22 and its 52-week low is $104.17, so the current price sits near the bottom of its annual range.

The analyst community remains largely bullish. 13 analysts rate MSTR a Buy or Strong Buy, 1 rates it a Hold, and none rate it a Sell. That 93% bullish consensus is remarkable for a stock that has lost nearly half its value over the past year. The bull thesis rests on the premise that if bitcoin is going significantly higher, Strategy’s leveraged accumulation strategy will compound those gains for common shareholders.

The Case for Buying Here Is Real, But So Is the Case for Staying Away

The bull case comes down to bitcoin. If bitcoin is early in a sustained move toward $100,000 or higher, the setup starts to work quickly in shareholders’ favor. The BPS growth engine compounds, the preferred stock platform provides ongoing access to capital, and the path back toward analyst targets looks reasonable.

The bear case shows up if bitcoin stalls or moves lower. The company has $10.60 billion in total liabilities, ongoing preferred dividend obligations, and continued dilution from ATM programs. Its bitcoin value sits around $54 billion, and with bitcoin near $71,529, the position is roughly equivalent to the company’s current enterprise value.

The upside looks compelling on paper, with 191% implied upside to analyst targets. But this is still a directional bet on bitcoin, not a business driven by stable cash flows. Until bitcoin shows a clear move higher, the gap between the stock and analysts’ price targets is likely to remain wide.