Wall Street’s conviction around Alphabet‘s (NASDAQ:GOOGL | GOOGL Price Prediction) long-term story keeps building. William O’Neil has reinstated coverage of Alphabet stock with a Buy rating, a signal that the firm sees the search giant’s expanding portfolio, spanning AI-powered search to autonomous vehicles, as a compelling opportunity at current levels. No price target was provided alongside the reinstatement.

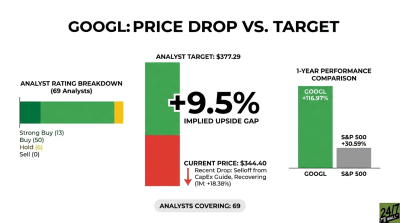

The timing is notable. Alphabet shares are flat year-to-date and currently trade near $312, well below the analyst consensus target of $376.29. With 61 Buy or Strong Buy ratings and zero Sell ratings across Wall Street, William O’Neil’s reinstatement lands in a firmly bullish crowd.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| GOOGL | Alphabet | William O’Neil | Reinstatement | N/A | Buy | N/A | N/A |

The Analyst’s Case

William O’Neil’s reinstatement centers on Alphabet’s multi-engine growth story. The thesis highlights Google Search, YouTube, Google Cloud, AI integration across products, and Waymo’s autonomous vehicle expansion as the key pillars. Each of these segments delivered in the most recent quarter, giving the firm a concrete fundamental foundation for the call.

Google Cloud is the standout. Cloud revenue reached $17.66 billion in Q4 2025, up 48% year-over-year, with operating income more than doubling. The segment now runs at an annual run rate exceeding $70 billion, backed by a $155 billion backlog as of Q3 2025.

Company Snapshot

Alphabet crossed a historic threshold in fiscal 2025, generating $402.8 billion in full-year revenue , the first time the company has exceeded $400 billion annually. Full-year net income reached $132.17 billion, up 32% year-over-year. Google Search revenue alone hit $63.07 billion in Q4, while YouTube’s combined ads and subscriptions revenue surpassed $60 billion annually.

Waymo, Alphabet’s autonomous driving subsidiary, received a $16 billion investment round announced in February 2026, majority funded by Alphabet. That’s a serious capital commitment to what could become a transformative revenue stream, though it remains in the early innings.

Why the Move Matters Now

Alphabet trades at a forward P/E ratio of 26x, a discount to its trailing multiple, suggesting the market is pricing in continued earnings growth. CEO Sundar Pichai noted on the Q4 earnings call that “the Gemini App has grown to over 750 million monthly active users” and that “Search saw more usage than ever before, with AI continuing to drive an expansionary moment.” With Q1 2026 earnings scheduled for April 29, the reinstatement arrives at a moment when investors are actively reassessing the stock’s near-term trajectory.

What It Means for Your Portfolio

William O’Neil’s Buy reinstatement adds institutional weight to a thesis that’s already well-supported by fundamentals. If you believe Alphabet’s AI investments in Gemini and Waymo will translate into durable revenue streams, and that Google Cloud’s 48% growth rate reflects a structural shift rather than a cyclical bump, the stock’s current price relative to analyst targets offers a case worth examining.

That said, Alphabet’s planned 2026 capital expenditures of $175 billion to $185 billion represent a massive bet on AI infrastructure, and execution risk is real. Antitrust scrutiny over Search dominance remains an overhang. Cautious GOOGL stock investors will want to watch for whether Q1 2026 earnings confirm that Cloud momentum and AI monetization are accelerating before adding materially to any position.