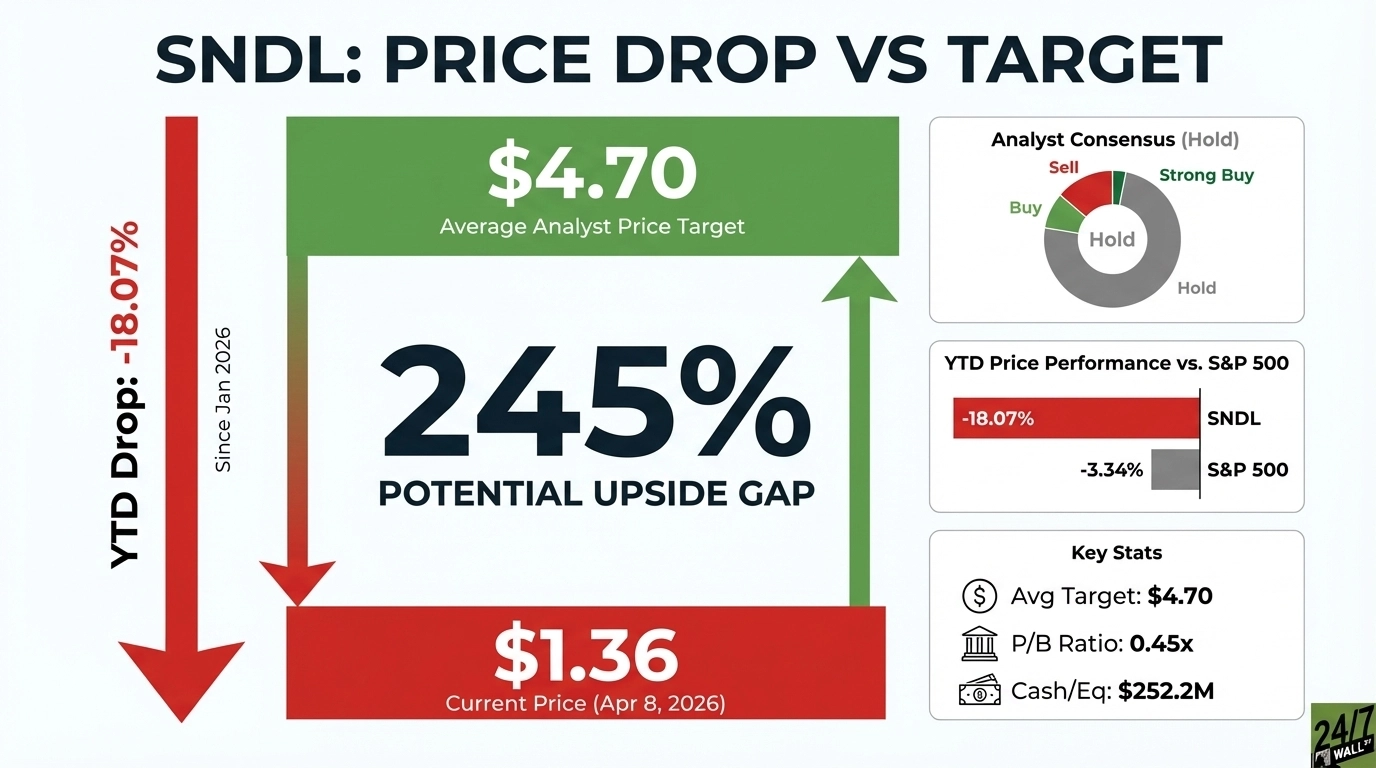

SNDL Inc. (NASDAQ:SNDL) currently trades at $1.36, while the average analyst price target sits at $4.70, implying an upside of roughly 245% from current levels.

SNDL is Canada’s largest private-sector liquor and cannabis retailer, operating 167 liquor stores under banners including Ace Liquor, Liquor Depot, and Wine and Beyond, as well as 192 cannabis retail locations under Value Buds, Spiritleaf, and Cost Cannabis. The company also runs a cannabis cultivation and manufacturing segment and holds strategic cannabis investments through SunStream Bancorp. A 245% gap between the stock’s price and analysts’ price target warrants a closer look at the stock.

Declining Since October, Accelerated by Earnings

SNDL’s slide traces back to a peak of $2.50 in September 2025, followed by a sharp drop to $1.67 by November 2025. The stock briefly recovered to $2.15 in December before resuming its descent. Q4 2025 earnings accelerated the move, with the stock gaining +1.3% on the day of the announcement, falling -3.21% the following day, and dropping -10.9% over the following week. SNDL has averaged a -7.45% one-day post-earnings decline and -9.47% over the following week across its last three quarterly reports.

Q4 2025 revenue came in at $252.50M against a $257.97M estimate, a miss of 2.12%. Liquor retail posted revenue of $148.84M, down 3.4% year over year. Cannabis retail same-store sales fell 0.7% in Q4 but gained 3.9% for the full year.

Broader market weakness adds some context, with the S&P 500 down roughly 3.34% year to date. SNDL has fallen 18.07% year to date, making its underperformance severe and largely self-inflicted by segment-level softness.

What Analysts Still See in a Stock the Market Has Nearly Given Up On

The analyst consensus is officially “Hold” with a target of $4.698. This 245% implied upside reflects that the underlying bull case has concrete pillars.

The first pillar is the balance sheet. SNDL carries $252.24M in cash and equivalents vs $170 million in capital lease obligations at year-end. That cash pile lowers the company’s enterprise value significantly to roughly $292 million, while the market cap is $352 million.

The second pillar is the catalyst stack. A corporate restructuring targeting more than C$20M in annualized savings is expected to complete in Q2 2026. There are 27 pending Ontario store approvals from the 1CM acquisition that could expand the retail footprint meaningfully. International cannabis sales tripled from C$3.6M to C$12.6M, an early-stage growth vector. U.S. cannabis rescheduling from Schedule I to Schedule III, if it proceeds, could eliminate Section 280E tax treatment and benefit SNDL’s SunStream investment portfolio.

A Stock Trading at 47 Cents on the Dollar of Book Value

SNDL currently trades at $1.36 against an analyst consensus target of $4.698. The stock trades at a price-to-book ratio of 0.447, meaning investors are paying less than 50 cents for every dollar of book value. The 52-week range runs from $1.15 to $2.89, putting the current price closer to the floor than the ceiling. The stock is down 18.07% year to date, while the S&P 500 has declined approximately 3.34%.

The stock’s beta sits at 0.813, suggesting SNDL is less volatile than the broader market, making year-to-date underperformance more notable. The EV/EBITDA multiple of 8.46x is reasonable for a company with operational recovery underway.

The Gap Is Real, But So Is the Risk

The path to the analyst target requires execution across multiple fronts.

Restructuring savings need to materialize on schedule, Ontario store approvals must unlock meaningful revenue, and international cannabis sales have to sustain triple-digit growth. With a price-to-book ratio below 0.5 and over $60 million in net cash, the balance sheet provides a downside floor that many businesses simply do not have.

That said, risks remain. Liquor retail demand could continue to soften, SunStream restructurings may drag on longer than expected, and Canadian cannabis retail might struggle to reaccelerate after the Q4 slowdown. Free cash flow also declined 59.1% for the full year, signaling that capital efficiency is moving in the wrong direction even as profitability metrics improve.

The balance sheet gives SNDL a level of survivability that most small-cap cannabis companies lack. The restructuring and store expansion catalysts are real and time-bound. Still, a 245% gap to the target alongside a Hold consensus suggests that any upside will likely take years, not quarters.